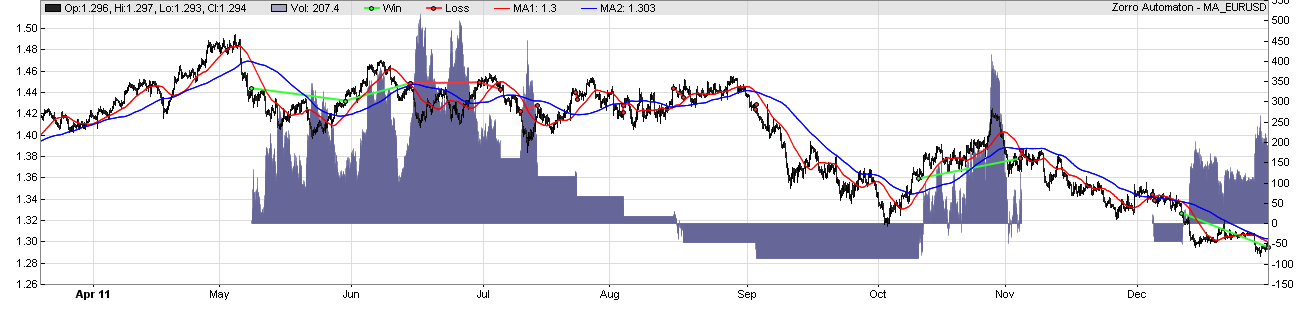

Here is something I did over a year ago in R. It is a simple 30 minute cross on the SPX intraday, i.e., if the 30 minute SMA crosses the price, then enter or exit. PL curve attached.

lastmin = 388

simday = function(datestr,plotflag=FALSE) {

day = as.Date(datestr)

spxidx = spx$Date==day

flipvec = vector()

#print(spx$Date[spxidx])

totpl = 0.0

maxpl = 0.0

maxtime = 0

firstpos = 0.0

firsttime = 0

ncross = 0

if (sum(spxidx)==390) {

#print(as.Date(day,origin="1970-01-01"))

#flush.console()

open = spx$Open[spxidx]

high = spx$High[spxidx]

low = spx$Low[spxidx]

close = spx$Close[spxidx]

sma30 = spx$SMA30[spxidx]

status = "cash"

price = 0.0

for (imin in seq(sum(spxidx))) {

if (imin >= 40 && imin < lastmin) {

if (status!="short" && close[imin]<sma30[imin]) {

status = "short"

ncross = ncross+1

pl = 0.0

if (price>0.0) {

pl = (low[imin]-price)

totpl = totpl+pl

if (totpl>maxpl) {

maxpl = totpl

maxtime = imin

}

if (firsttime==0 && totpl>0) {

firsttime = imin

firstpos = totpl

}

}

price = low[imin]

print(paste("short",as.Date(day,origin="1970-01-01"),imin,price,pl,totpl))

flipvec = c(flipvec,imin)

}

if (status!="long" && close[imin]>sma30[imin]) {

status = "long"

ncross = ncross+1

pl = 0.0

if (price>0.0) {

pl = (price-high[imin])

totpl = totpl+pl

if (totpl>maxpl) {

maxpl = totpl

maxtime = imin

}

if (firsttime==0 && totpl>0) {

firsttime = imin

firstpos = totpl

}

}

price = high[imin]

print(paste("long",as.Date(day,origin="1970-01-01"),imin,price,pl,totpl))

flipvec = c(flipvec,imin)

}

}

}

# close positions at end of day

imin = lastmin

if (status=="long") {

pl = 0.0

if (price>0.0) {

pl = (low[imin]-price)

totpl = totpl+pl

}

if (totpl>maxpl) {

maxpl = totpl

maxtime = imin

}

if (firsttime==0 && totpl>0) {

firsttime = imin

firstpos = totpl

}

price = low[imin]

print(paste("eod close long",as.Date(day,origin="1970-01-01"),imin,price,pl,totpl))

flipvec = c(flipvec,imin)

}

else if (status=="short") {

pl = 0.0

if (price>0.0) {

pl = (price-high[imin])

totpl = totpl+pl

}

if (totpl>maxpl) {

maxpl = totpl

maxtime = imin

}

if (firsttime==0 && totpl>0) {

firsttime = imin

firstpos = totpl

}

price = high[imin]

print(paste("eod close short",as.Date(day,origin="1970-01-01"),imin,price,pl,totpl))

flipvec = c(flipvec,imin)

}

print(paste(as.Date(day,origin="1970-01-01"),ncross,totpl))

flush.console()

if (plotflag) {

plot(close,type="l",col="blue",main=datestr)

plot.xy(xy.coords(seq(length(close)),sma30),type="l",col="red")

abline(v=flipvec,col="green")

grid()

}

}

c(totpl,ncross,maxpl,maxtime,firstpos,firsttime)

}

spx = read.table("spx.csv",sep=",",stringsAsFactors=FALSE,header=TRUE)

spx$Date = as.Date(spx$Date,format="%m/%d/%Y")

datevec = unique(spx$Date)

ndays = length(datevec)

plvec = vector()

simdates = vector()

ncrossvec = vector()

maxplvec = vector()

maxtvec = vector()

firstplvec = vector()

firsttvec = vector()

for (day in datevec[1:ndays]) {

retvec = simday(as.character(as.Date(day,origin="1970-01-01")))

totpl = retvec[1]

ncross = retvec[2]

maxpl = retvec[3]

maxtime = retvec[4]

firstpl = retvec[5]

firstt = retvec[6]

if (totpl!=0.0) {

plvec = c(plvec,totpl)

simdates = c(simdates,as.Date(day,origin="1970-01-01"))

ncrossvec = c(ncrossvec,ncross)

maxplvec = c(maxplvec,maxpl)

maxtvec = c(maxtvec,maxtime)

firstplvec = c(firstplvec,firstpl)

firsttvec = c(firsttvec,firstt)

}

}

pldat = data.frame(date=as.Date(simdates,origin="1970-01-01"),pl=plvec,ncross=ncrossvec,maxpl=maxplvec,maxt=maxtvec,firstpl=firstplvec,firstt=firsttvec)