Of course, none of this needs to be restated for the ETers, who are all master traders, never have a losing day, never trade anything but ES on 5 minute charts, and have a perfect system and complete discipline that "pulls out" $500/day from the market, like clockwork. Or they're just a few bad trades away from world domination.

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

shooting the moon

- Thread starter billyjoerob

- Start date

More insane top shorting.

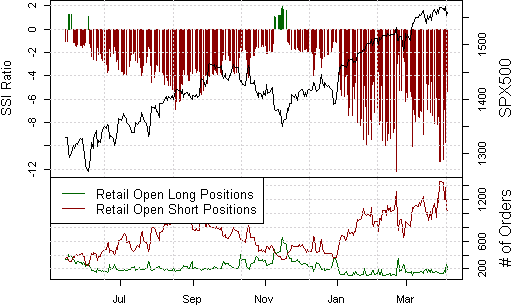

SPX500 âRetail CFD speculators remain aggressively net-short the SPX500 contract as it trades near record-highs, and we see little choice but to maintain our bullish contrarian trading forecast.

http://www.dailyfx.com/technical_analysis/sentiment?technicalSentiment=SPX500

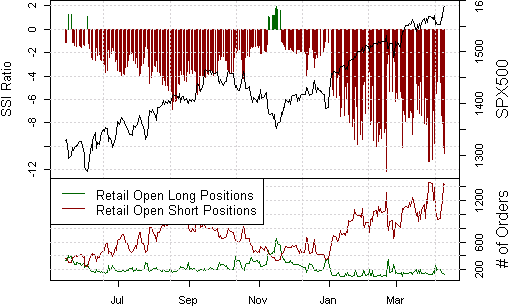

SPX500 âRetail CFD speculators remain aggressively net-short the SPX500 contract as it trades near record-highs, and we see little choice but to maintain our bullish contrarian trading forecast.

http://www.dailyfx.com/technical_analysis/sentiment?technicalSentiment=SPX500

There may be another $10 in IDT. $8 of cash, business is probably worth $10, and then $7-$10 for Zedge, a profitable mobile app for trading ringtones/screensavers.

http://stockcharts.com/h-sc/ui?s=IDT&p=D&yr=0&mn=6&dy=0&id=p51300415546

Good example of this strategy, from Dan Loeb:

âIn the 1990s, we recognized that the growth of the Internet would have a huge impact, but instead of focusing just on new internet companies, we bought a bunch of old-line companies that had internet companies embedded within them and we did quite well without taking the risk attendant in purchasing shares of high-flying overpriced internet companies."

http://stockcharts.com/h-sc/ui?s=IDT&p=D&yr=0&mn=6&dy=0&id=p51300415546

Good example of this strategy, from Dan Loeb:

âIn the 1990s, we recognized that the growth of the Internet would have a huge impact, but instead of focusing just on new internet companies, we bought a bunch of old-line companies that had internet companies embedded within them and we did quite well without taking the risk attendant in purchasing shares of high-flying overpriced internet companies."

Our retail sentiment data shows that the number of orders short SPX500 outnumber those long by an almost-unbelievable 10.6 to 1.

. . .

As it stands we would equate getting short at these levels as roughly equivalent of jumping in front of a freight train.

http://www.dailyfx.com/technical_analysis/sentiment?technicalSentiment=SPX500

. . .

As it stands we would equate getting short at these levels as roughly equivalent of jumping in front of a freight train.

http://www.dailyfx.com/technical_analysis/sentiment?technicalSentiment=SPX500

J. Gundlach: "Gourmet Burito is an oxymoron"

http://stockcharts.com/h-sc/ui?s=CMG:JACK&p=W&b=5&g=0&id=p99844405027

I think he's probably right. The Qdoba breakfast burrito is quite tasty, 600 calories for $3.

http://stockcharts.com/h-sc/ui?s=CMG:JACK&p=W&b=5&g=0&id=p99844405027

I think he's probably right. The Qdoba breakfast burrito is quite tasty, 600 calories for $3.

A smart economist and blogger says something which probably reflects the approach of most ordinary investors:

http://www.arnoldkling.com/blog/ (permalink is broken)

"Speaking of stocks, I know of a newsletter writer who recommends specific stocks and always adds what he calls a âprotective stop.â So he might say, âbut X at 20, but put in a stop-less order to sell if it goes down to 18.â This struck me as a strange strategy, but today I was pondering it and I think I have it figured out.

Suppose that the stocks that he recommends are really no better or worse than buying an index fund. So, without the stop-loss orders, if you followed his buy recommendations you would get the exact same return as the market. With the stop-loss orders, itâs as if you are buying the market portfolio along with a portfolio of out-of-the-money put options. In this case, though, you only pay the option premium if the market bounces around, so you buy a stock at 20, sell it at 18, then buy it back (or buy some other stock recommended by the newsletter) when it goes back up to 20.

I think that this approach minimizes the chances that you will regret taking the writerâs advice. If the market rallies, you will be happy with your gains. If it falls, you will be happy that your losses are limited. And if it bounces up and down you are unlikely to notice that the advice is giving you a tendency to buy at the highs and sell at the lows. So I think this strategy would appeal to regret-averse investors. But itâs not a strategy that appeals to me."

Kling seems to think that losses are temporary, so any attempt to limit losses is irrational. He speaks of "regret-averse" instead of risk-averse because he doesn't really see a reason to limit losses, other than an irrational fear of regret.

If the auditor of HLF said to you, next quarter's earnings will be good, that would be a good bet to make. You might even leverage up. The problem is that even if you knew the destination, you wouldn't know the path. So there is an optimal strategy that isn't simply betting 1000% of your networth on HLF and waiting for the profits. Even if you knew the destination, it would make sense to use a stop loss.

Let's say you knew HLF would trade for $100 in 12 months. You are given these options,

a) buy now, but no opportunity to sell in the interim, and no leverage.

b) you can buy when you like, but no selling, and no leverage.

c) buy when you like, sell only once, and no leverage.

d) buy when you like, sell only once, and leverage.

e) no buying or selling restrictions, and no leverage.

f) no restrictions, leverage

Obviously, f is the best option. The value of f) simply illustrates the enormous option value of cash. But Kling prefers a), it seems. Or he thinks the selling options are limited to c) or d). But there is the possibility that the stock declines, post sale. Then the option of unlimited buys and sells is very valuable, versus a) thru d). Of course, if you don't know the price of HLF in 12 months, but you do have a high conviction about the price of the market in 20 years, then your best option might be a).

http://www.arnoldkling.com/blog/ (permalink is broken)

"Speaking of stocks, I know of a newsletter writer who recommends specific stocks and always adds what he calls a âprotective stop.â So he might say, âbut X at 20, but put in a stop-less order to sell if it goes down to 18.â This struck me as a strange strategy, but today I was pondering it and I think I have it figured out.

Suppose that the stocks that he recommends are really no better or worse than buying an index fund. So, without the stop-loss orders, if you followed his buy recommendations you would get the exact same return as the market. With the stop-loss orders, itâs as if you are buying the market portfolio along with a portfolio of out-of-the-money put options. In this case, though, you only pay the option premium if the market bounces around, so you buy a stock at 20, sell it at 18, then buy it back (or buy some other stock recommended by the newsletter) when it goes back up to 20.

I think that this approach minimizes the chances that you will regret taking the writerâs advice. If the market rallies, you will be happy with your gains. If it falls, you will be happy that your losses are limited. And if it bounces up and down you are unlikely to notice that the advice is giving you a tendency to buy at the highs and sell at the lows. So I think this strategy would appeal to regret-averse investors. But itâs not a strategy that appeals to me."

Kling seems to think that losses are temporary, so any attempt to limit losses is irrational. He speaks of "regret-averse" instead of risk-averse because he doesn't really see a reason to limit losses, other than an irrational fear of regret.

If the auditor of HLF said to you, next quarter's earnings will be good, that would be a good bet to make. You might even leverage up. The problem is that even if you knew the destination, you wouldn't know the path. So there is an optimal strategy that isn't simply betting 1000% of your networth on HLF and waiting for the profits. Even if you knew the destination, it would make sense to use a stop loss.

Let's say you knew HLF would trade for $100 in 12 months. You are given these options,

a) buy now, but no opportunity to sell in the interim, and no leverage.

b) you can buy when you like, but no selling, and no leverage.

c) buy when you like, sell only once, and no leverage.

d) buy when you like, sell only once, and leverage.

e) no buying or selling restrictions, and no leverage.

f) no restrictions, leverage

Obviously, f is the best option. The value of f) simply illustrates the enormous option value of cash. But Kling prefers a), it seems. Or he thinks the selling options are limited to c) or d). But there is the possibility that the stock declines, post sale. Then the option of unlimited buys and sells is very valuable, versus a) thru d). Of course, if you don't know the price of HLF in 12 months, but you do have a high conviction about the price of the market in 20 years, then your best option might be a).

There has to be a mathematical way to put this, maybe for somebody smarter than me.

stock a moves from 1 to 5, lets call it 4u

stock b moves up 2 and back 1, so from 1 to 5 it moves 8u (from 1 - 3 - 2 - 4 - 3 - 5)

So same destinations, different paths. Stock b travels twice as far (8u vs. 4u). b is in a sense the better trading stock, and if you were long only, you missed out. If you only know the destination (as with bonds), that is useful, but if you know the path, you also know the destination, and you can lever up.

But let's say you know the destination but not the path. You choose to invest 50%. Your odds may improve, they may get worse. You don't know. In that case, you are never going to be fully invested. Your odds can always improve.

stock a moves from 1 to 5, lets call it 4u

stock b moves up 2 and back 1, so from 1 to 5 it moves 8u (from 1 - 3 - 2 - 4 - 3 - 5)

So same destinations, different paths. Stock b travels twice as far (8u vs. 4u). b is in a sense the better trading stock, and if you were long only, you missed out. If you only know the destination (as with bonds), that is useful, but if you know the path, you also know the destination, and you can lever up.

But let's say you know the destination but not the path. You choose to invest 50%. Your odds may improve, they may get worse. You don't know. In that case, you are never going to be fully invested. Your odds can always improve.

"Since November 13, 1987, Monday and Tuesdays combined are up 595.68% for the Dow, while Wednesday, Thursday and Friday combined are up 9.72%. For more a quarter of a century, nearly the Dowâs entire gain has come during the first 40% of the week."

http://www.crossingwallstreet.com/archives/2013/04/stats-for-the-dow.html

But it's not just on a weekly basis. I bet you could find the same thing on a daily or monthly or yearly basis. Most of the gain is at the beginning or the end - January thru March and then November thru December are where most of the stock gains are concentrated. Likewise first few and last few days of the month. And same for daily trading, most of the gains are before 10:30.

I consider myself a weekly trader, I find weekly charts more informative than daily. A bearish daily chart can often look very different viewed weekly.

http://www.crossingwallstreet.com/archives/2013/04/stats-for-the-dow.html

But it's not just on a weekly basis. I bet you could find the same thing on a daily or monthly or yearly basis. Most of the gain is at the beginning or the end - January thru March and then November thru December are where most of the stock gains are concentrated. Likewise first few and last few days of the month. And same for daily trading, most of the gains are before 10:30.

I consider myself a weekly trader, I find weekly charts more informative than daily. A bearish daily chart can often look very different viewed weekly.

If this market is a megaphone top, ie lower lows and higher highs, then I could see the SPY go to 2000 like a rocket and then collapse just as hard back to the 1600 base. That would certainly inflict maximum pain, which is why markets were invented.