Hi TheBigShort

Thanks for being a subscriber.

I'll expand on the how we calculate the earnings effect defined as the amount of extra implied volatility in each expiration due to the expected move after an earnings announcement.

To remove the implied earnings effect in the IV, ORATS follows these steps.

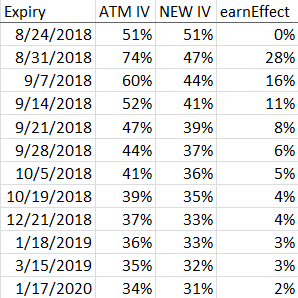

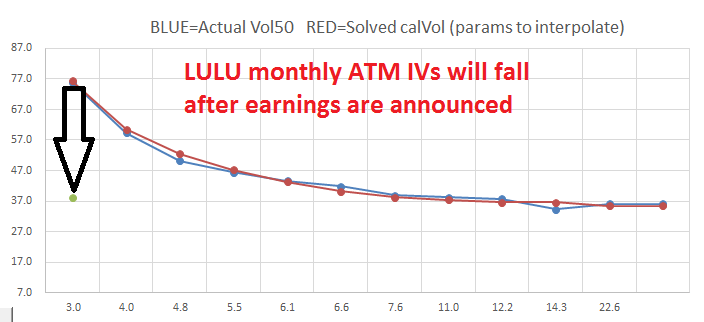

For example, consider LULU that announced earnings 8/30/2018 after the close. Presented below is the method for extracting earnings from IV. See the at-the-money IVs for each expiration, post removal of earnings effect IV, and that portion of the IV that is applicable to the earnings announcement move:

- Apply accurate earnings announcement dates to determine how many earnings apply to each expiration;

- Solve for an earnings move that makes the most rational resultant ex-earnings effect monthly implied volatility relationships;

- Present monthly and constant maturity readings historically.

The 8/25/2018 expiry does not have an earnings effect. 8/31/2018 has the largest earnings effect (since the earnings effect will have a greater percentage of days relative to the number of days to expiration). Notice how the method solves for a remaining NEW IV skew that is still down sloping (backwardation).

I hope this helps.

Matt

You don't use decimals???

...and a suggestion. Excel --> format data series --> line style --> smooth