Suppose you backtest and don't like what you see. You're probably going to drop the rule, or modify it

You shouldn't really take any action at all, since you have forward information at this point.

But if you're going to backtest and ignore the results, then what's the point of doing it?

To be honest I find the dichotomy artificial, and it's not a distinction I'd seen before, so some of the argument might be that I am not understanding the nomenclature. I don't really understand what you mean by 'forwardtesting'....?

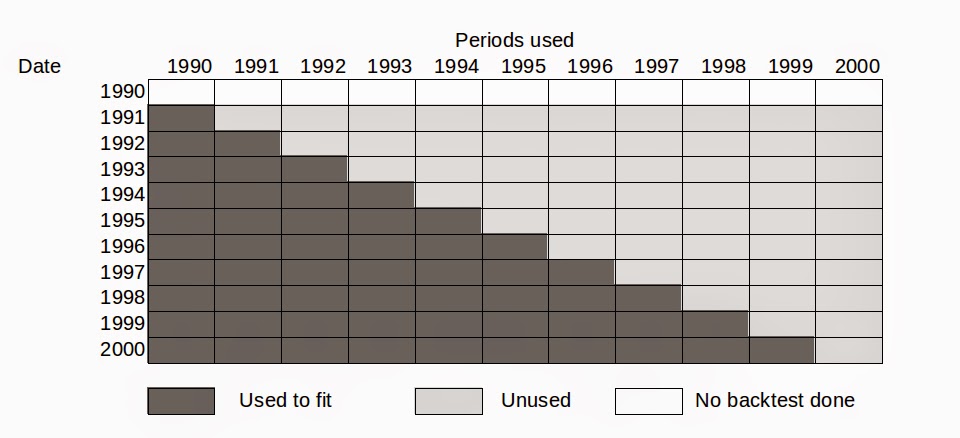

To me WFA is a form of backtesting*, and in my opinion the only valid one.

* other time domains are fully in sample, half out of sample (fit on first period A, test on second period B), half and half (fit on A test on B, fit on B test on A), knock one out (fit on all years except 2002, test on 2002; fit on all years except 2003, test on 2003...)

I think they mean "paper trading" or some other sort of demo trading with optimized strategy with live data (unlike past data in WFA) when they say "forward testing". But you are absolutely right that WFA is the only valid backtesting method.

") ). So bottomline is, you call it out-of-sample testing, I call it WFA. Nice to know that some traders out there don't do backtesting with the whole historical data and curvefitting as a consequence.

). So bottomline is, you call it out-of-sample testing, I call it WFA. Nice to know that some traders out there don't do backtesting with the whole historical data and curvefitting as a consequence.