Lots of perma option sellers are lured into the strategy because of its 'positive expectation', they will read studies on why options are consistently 'overpriced' and hence think that its a great deal to sell them. I did a little monte carlo simulation on a normal trading system vs a typical option selling type system. I then compared how one stacked up against the other.

System 1

50% chance of a -1 return

50% chance of a +2 return

1 trade per time period

System 2

97.6% chance of a +1 return

2.3% chance of a -20 return

1 trade per time period

The systems both have the same expected value (roughly), so in theory they are the same but in practice they are completely different. The risk adjusted returns of System 1 just blows System 2 out of the water.

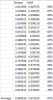

I did several simulations of 2000 trades each. These are the results for System 1. MAR is CAGR/MAX DrawDown. Bet size is 2% of the account (a typical rule of thumb used by traders)

System 2 using 2% bet size

Risk adjusted returns are a lot better on System 1.

I guess this explains why options are 'overpriced'.

Option sellers extract expected returns at the cost of ruining their risk adjusted returns (and maybe their health).

There is no free lunch in selling options, most of the financial world runs on risk adjusted returns (like hedge funds), most people can't tolerate certain drawdowns without going crazy/killing themselves, lots of traders would be fired if they used something similar to system 2.

The cost of going against convexity is worse risk adjusted metrics, so that leads one to believe that the benefit of adding convexity is an improvement in risk adjusted metrics. Effectively, buying options can be a way of juicing one's performance metrics. This shows that folly of 99% of ET traders looking to sell options (like Sweet Bobby), they are trying to come up with a system that already has something bad going against it. Why choose from a system pool so severely disvantaged? System 1 type system pool has several things going for it, its a lot better pool to choose from

conclusion: Dont add anti-convexity bets into a portfolio unless you really know what you are doing. Expectation has nothing to do with it, its about the payoff distribution over a long enough period of time