GOOD READ

Investors should adjust to trading in the Twilight Zone as Wall Street narratives change quicker than a TikTok video, BofA Securities says in its weekly Flow Show note Friday.

Investors "are in the trickiest partof the investment cycle: tightening ending but easing far from beginning, inflation over but recession not yet begun, China reopen vs US recession," strategist Michael Hartnett wrote in a note.

Investor conviction is still in a huge bear market and tail risks to the consensus are high, Hartnett added.

In the current scenario, he posed three "heretical thoughts":

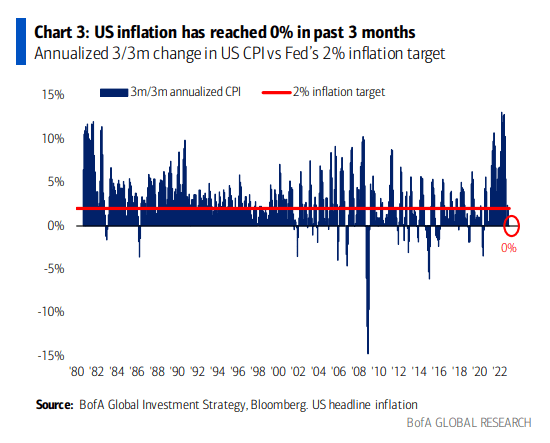

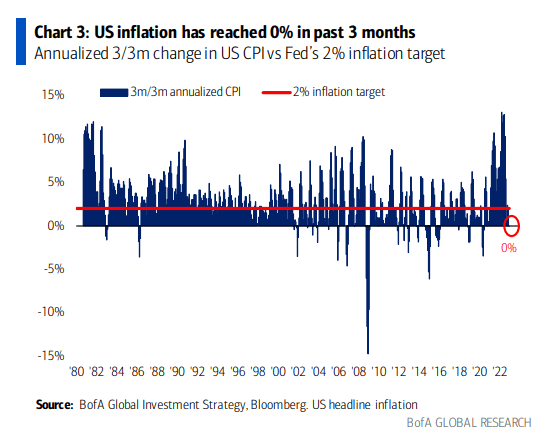

- CPI troughs in Q1. Annualized three-month change in CPI is 0% (see chart at bottom) while markets are bullishly trading two more quarter-point Fed hikes and 200 bps of cuts over 18 months. A "super-tight labor market (<200k on initial claims) + renewed rise (in) commodity prices (China reopen + MAD geopolitics in Russia/Ukraine)" could lead to a couple of higher-than-expected CPI prints that reverse outsized expectations of 200bps of cuts.

- "Mission Accomplished" central banks unwittingly confirm a new era of inflation. The expected end of tightening would occur before policy rates hit restrictive levels in real terms and "hikes ending with all economies at full employment/inflation well above target." Central banks are "quietly accepting higher structural inflation, wittingly or unwittingly (maybe they think low rates help to service government debt, higher inflation helps to debase nominal level of debt, inflation cures wealth inequality)."

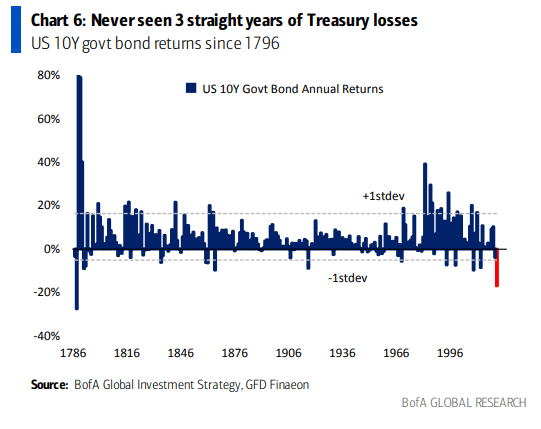

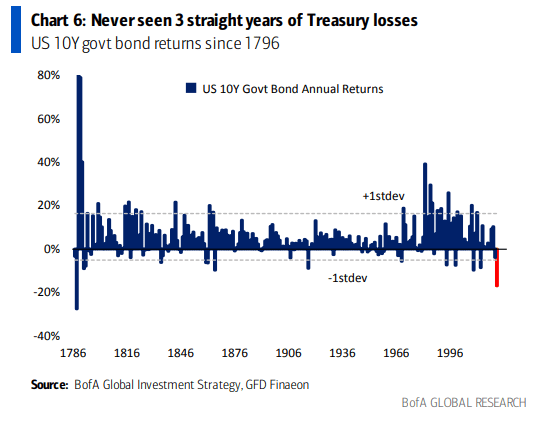

- Q2 recession marks a low in bond yields.Last year's 17% loss in U.S. Treasuries (TBT) (TLT) (SHY) was the worst since 1788 and there has never been three-straight years of U.S. government bond losses. "250 years of history say US Treasury returns up in 2023 ... but recession coming and likely a biggie." Higher U.S. unemployment coinciding with a 2% personal savings rate, a 15% growth in credit card debt, 19% record APR credit card rates at a 50-year high and consumer finance companies increasing provision is "no bueno."

From a cyclical viewpoint, Hartnett still predicts positive Treasury returns this year and a tough year for stocks (NYSEARCA:

SPY) (

QQQ) (

DIA) (

IWM), with a hard landing and credit events risks underpriced. For the S&P 500 (

SP500)

he says nibble at 3,600, bite at 3,300 and gorge at 3,000.

Looking at secular leadership there will be a shift from deflation assets to inflation assets being a conviction trade, like Japan in 1990, the dot-com bust in 2000, U.S. and EU banks in 2007 and BRICs and resources in 2011, he added.

Tech (

XLK) and FAANG (

META) (

AAPL) (

AMZN) (

NFLX) (

GOOG) (

GOOGL) will underperform in the coming years and the new leadership will be inflation assets like commodities, non-U.S. stocks, small-cap over large-cap and value (

IWD) over growth (

IWF), Harnett said.