You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

FXCM Discussion

- Thread starter Jason Rogers

- Start date

Jason Rogers

ET Sponsor

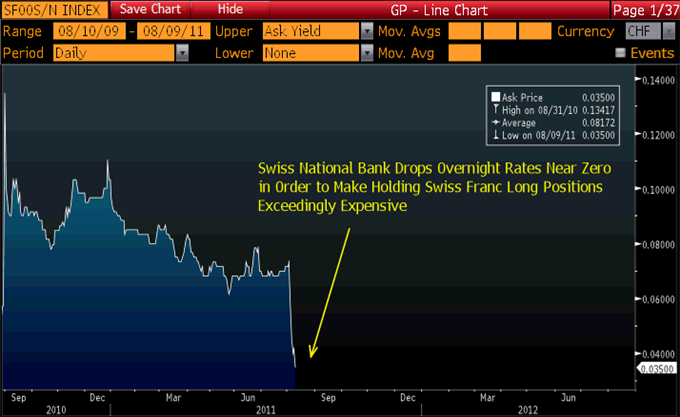

If you're long the CHF, beware of rollover charges increasing (especially on EUR/CHF) as a result of the Swiss National Banks cut to short term interest rates last week. Overnight rates for the CHF have fallen to record lows which is part of the SNB's attempt to make it less attractive to buy the CHF. The result being that it is more expensive to hold long positions in the Swiss Franc.

Below is a screenshot from Bloomberg of overnight rates in the franc, and a complete article from DailyFX can be found here http://www.dailyfx.com/forex/fundam...rt/2011/08/09/Swiss_Franc_Soars_Rollover.html

Let me know if you have any questions.

-Jason

Below is a screenshot from Bloomberg of overnight rates in the franc, and a complete article from DailyFX can be found here http://www.dailyfx.com/forex/fundam...rt/2011/08/09/Swiss_Franc_Soars_Rollover.html

Let me know if you have any questions.

-Jason

Hey Jason,

I'm interested in the new US Dollar index product... but:

Few quick questions:

How did FXCM come up with the weighting on their USDOLLAR index product?

Related to the first question, why didn't FXCM just use the weighting common to the US dollar index futures? (DX) As traded on various futures exchanges?

Why is the spread on said index 0.5-1 pip higher than the blend of spreads on the underlying components? (ie, people can build a synthetic position on that index at a lower costs by using currency pairs..)

Is the index considered a currency product or a CFD? Will my order be instantly executed with FXCM or will FXCM first need to settle the underlying positions before confirming my position price?

Thanks in advance!

-Jack

PS. I've been following your thread over at forexfactory and noticed you have to deal with a lot of crap from anti-FXCM people.. Don't let them bother you, keep up the good work, I think you're doing a great job.

I'm interested in the new US Dollar index product... but:

Few quick questions:

How did FXCM come up with the weighting on their USDOLLAR index product?

Related to the first question, why didn't FXCM just use the weighting common to the US dollar index futures? (DX) As traded on various futures exchanges?

Why is the spread on said index 0.5-1 pip higher than the blend of spreads on the underlying components? (ie, people can build a synthetic position on that index at a lower costs by using currency pairs..)

Is the index considered a currency product or a CFD? Will my order be instantly executed with FXCM or will FXCM first need to settle the underlying positions before confirming my position price?

Thanks in advance!

-Jack

PS. I've been following your thread over at forexfactory and noticed you have to deal with a lot of crap from anti-FXCM people.. Don't let them bother you, keep up the good work, I think you're doing a great job.

Jason Rogers

ET Sponsor

Quote from Jack_Larkin:

Hey Jason,

I'm interested in the new US Dollar index product... but:

Few quick questions:

How did FXCM come up with the weighting on their USDOLLAR index product?

Related to the first question, why didn't FXCM just use the weighting common to the US dollar index futures? (DX) As traded on various futures exchanges?

Why is the spread on said index 0.5-1 pip higher than the blend of spreads on the underlying components? (ie, people can build a synthetic position on that index at a lower costs by using currency pairs..)

Is the index considered a currency product or a CFD? Will my order be instantly executed with FXCM or will FXCM first need to settle the underlying positions before confirming my position price?

Thanks in advance!

-Jack

Hi Jack,

Thanks for the questions and happy to help.

FXCM looked at two things when creating the index: against which currencies does most USD volume occur and which areas of the world are most important in terms of trade with the US. When looking at these two questions, we thought the current currency futures index to be outdated.

The top currencies in the foreign exchange market by turnover against the US Dollar are the Euro, Japanese Yen, British Pound, and Australia Dollar. The Swiss Franc has about 1% more turnover than the Australian Dollar according to the BIS triennial survey released in 2010. The reason we included the Australian Dollar rather than the Swiss Franc is part of the second point. We wanted to make the index more representative of the current importance of geographic regions. The existing US Dollar Index (USDX) traded on the ICE futures exchange was created back in the 1970's when Europe was of much greater importance in terms of economic size and trade. It's no surprise then that the USDX is very euro-centric with nearly 78% of the basket being made up of European currencies (EUR, GBP, SEK, and CHF). However, much has changed since the 70's with Asian economies rising in importance. Giving a larger weighting to the JPY and AUD gives better reflects the rising importance of Asian economies and increased exchange versus the US Dollar. So that's some of the methodology behind the composition.

At the outset, the product will be a CFD. Our goal is to eventually have it executed via NDD whereby the trades are immediately offset with the liquidity providers, but it will take some time to have the technical abilities setup. The index basket has been rolled out to FXCM Asia in Hong Kong and FXCM UK. FXCM Australia will likely be next in the weeks ahead with FXCM US to follow sometime in the future.

We anticipate the spread on the Dow Jones FXCM US Dollar Index basket to possibly be one of the lowest we offer once fully launched. This would be a result of the large amount of liquidity among the 4 pairs that comprise the index, and also because volatility in the index basket tends to be very low. The average daily range for index basket since being launched in early January has been about 50-85 pips with the range increasing to only around 110 pips at its highest during last week's volatile market conditions. I'm not sure when we can expect this spread to come down, but I would guess it could occur after it's launched globally across all FXCM entities and trading volume in the index basket itself picks up. We also think lower volatility will mean a better product for our traders to trade since high amounts of volatility often translate into lower profitability for retail traders.

Thanks!PS. I've been following your thread over at forexfactory and noticed you have to deal with a lot of crap from anti-FXCM people.. Don't let them bother you, keep up the good work, I think you're doing a great job.

-Jason

Jason Rogers

ET Sponsor

A couple of announcements from FXCM...

1. Facebook Contest: Our facebook contest for a free trip to the FXCM currency trading expo in Las Vegas ends this Friday at 11:59pm. The prize includes (1) free round-trip ticket to Las Vegas and 3 day / 2 night stay at the Rio. Here's where to enter http://apps.facebook.com/promosapp/180941

2. CNBC Million Dollar Portfolio Challenge: FXCM is sponsoring this year's CNBC Million Dollar Portfolio challenge, and registration is now open to residents of the US, UK, and Australia. Every contestant is eligible to receive a free $50 account from FXCM (terms and conditions found through the contest site). The free account link is available after registering for the contest through http://milliondollar.cnbc.com

3. New AUS200 Spreads: The spread on the AUS200 stock index (which tracks the ASX200 stock index) is now 1 pip during local market trading hours, and 2 pips outside local market trading hours.

Let me know if you have any questions.

-Jason

1. Facebook Contest: Our facebook contest for a free trip to the FXCM currency trading expo in Las Vegas ends this Friday at 11:59pm. The prize includes (1) free round-trip ticket to Las Vegas and 3 day / 2 night stay at the Rio. Here's where to enter http://apps.facebook.com/promosapp/180941

2. CNBC Million Dollar Portfolio Challenge: FXCM is sponsoring this year's CNBC Million Dollar Portfolio challenge, and registration is now open to residents of the US, UK, and Australia. Every contestant is eligible to receive a free $50 account from FXCM (terms and conditions found through the contest site). The free account link is available after registering for the contest through http://milliondollar.cnbc.com

3. New AUS200 Spreads: The spread on the AUS200 stock index (which tracks the ASX200 stock index) is now 1 pip during local market trading hours, and 2 pips outside local market trading hours.

Let me know if you have any questions.

-Jason

Jason Rogers

ET Sponsor

There will be changes to CFD trading hours for oil, metals, and stock indices in observance of the US Labor Day Holiday on Monday, 5 September.

There will be no changes for forex trading hours due to the September 5th holiday. Below is a list and all times are in GMT.

CFD Trading Hours for Monday September 5th

Please Note: Oil, metals, and indices trading is not available to residents of the USA and its territories.

There will be no changes for forex trading hours due to the September 5th holiday. Below is a list and all times are in GMT.

CFD Trading Hours for Monday September 5th

Please Note: Oil, metals, and indices trading is not available to residents of the USA and its territories.

Jason Rogers

ET Sponsor

The FXCM Currency Trading Expo begins tomorrow at 9:30am PDT (16:30 GMT) and we will be broadcasting live from the expo onto FXCMExpo.com. The webpage has not launched yet, but I will post the link later today or early tomorrow. A total of 13 workshops will be broadcast live, including a workshop series on the characteristics of profitable traders hosted by David Rodriguez on Friday.

In between the workshops, there will also be interviews and Q&A with the DailyFX analysts hosted by myself and Jaclyn Sales along with Q&A. Questions can be sent by twitter to @FXCM and @JasonForex during the interview sessions. You can also send questions via twitter during the workshops for the DailyFX analysts and I'll do my best to get them answered during the 10 minute Q&A at the end of the workshop. Please make sure to include the hashtag #FXCMexpo in your tweet when sending questions.

The workshop schedule is below and I will post the link to website for watching the broadcast later today or early tomorrow. The times are listed in Pacific Daylight Time (GMT - 7) and GMT:

Please stop by and say hello if you are attending the expo. I will be floating around the exhibit hall and workshops during the weekend, and maybe we will even interview you")

-Jason

In between the workshops, there will also be interviews and Q&A with the DailyFX analysts hosted by myself and Jaclyn Sales along with Q&A. Questions can be sent by twitter to @FXCM and @JasonForex during the interview sessions. You can also send questions via twitter during the workshops for the DailyFX analysts and I'll do my best to get them answered during the 10 minute Q&A at the end of the workshop. Please make sure to include the hashtag #FXCMexpo in your tweet when sending questions.

The workshop schedule is below and I will post the link to website for watching the broadcast later today or early tomorrow. The times are listed in Pacific Daylight Time (GMT - 7) and GMT:

Please stop by and say hello if you are attending the expo. I will be floating around the exhibit hall and workshops during the weekend, and maybe we will even interview you

-Jason

Jason Rogers

ET Sponsor

Quote from Jason Rogers:

The FXCM Currency Trading Expo begins tomorrow at 9:30am PDT (16:30 GMT) and we will be broadcasting live from the expo onto www.FXCMExpo.com/live.

One small change to the Saturday schedule I posted previously. The final workshop being streamed online at 3pm PDT has been changed to "Developing a Trading Plan with Ilya Spivak". Here's today's schedule being streamed at www.fxcmexpo.com/live :

Jason Rogers

ET Sponsor

Last month, FXCM and H20 Markets hosted a seminar with guest speaker Richard Farleigh and the event booked out in 3 days. We will be hosting another seminar next Friday, September 23rd with Richard Farleigh again discussing "Trading Market Volatility".

The seminar will be hosted at The Grange Hotel on Friday September 23rd from 8:30am - 11:00am. If you're in the London area next Friday, we would love to see you there. Registration for the event can be found here http://www.fxcm.co.uk/richard.jsp

The seminar will be hosted at The Grange Hotel on Friday September 23rd from 8:30am - 11:00am. If you're in the London area next Friday, we would love to see you there. Registration for the event can be found here http://www.fxcm.co.uk/richard.jsp

Jason Rogers

ET Sponsor

The NYSE trading floor now has streaming currency rates provided by FXCM. The currency boards were turned on last week. Check it out!

<iframe width="560" height="315" src="http://www.youtube.com/embed/6Yl0TumZZf4" frameborder="0" allowfullscreen></iframe>

<iframe width="560" height="315" src="http://www.youtube.com/embed/6Yl0TumZZf4" frameborder="0" allowfullscreen></iframe>