Hi,

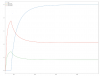

does anyone know why actual positions are really wild at the beginning of historical period? (See JPY below)

I wouldn't want to hold 100 contracts when trading a new instrument, so am trying to understand this effect.

Graphed using system.accounts.get_actual_position(instr).plot(title=instr)

Code to replicate, note I added JPY to my system...

from systems.provided.futures_chapter15.basesystem import futures_system

from matplotlib.pyplot import show

system = futures_system(log_level="on")

print(system.accounts.portfolio().sharpe())

#system.accounts.portfolio().curve().plot()

instr = system.get_instrument_list()[1]

instr = "JPY"

system.accounts.get_actual_position(instr).plot(title=instr)

show()

does anyone know why actual positions are really wild at the beginning of historical period? (See JPY below)

I wouldn't want to hold 100 contracts when trading a new instrument, so am trying to understand this effect.

Graphed using system.accounts.get_actual_position(instr).plot(title=instr)

Code to replicate, note I added JPY to my system...

from systems.provided.futures_chapter15.basesystem import futures_system

from matplotlib.pyplot import show

system = futures_system(log_level="on")

print(system.accounts.portfolio().sharpe())

#system.accounts.portfolio().curve().plot()

instr = system.get_instrument_list()[1]

instr = "JPY"

system.accounts.get_actual_position(instr).plot(title=instr)

show()