I've finally got round to producing a new backtest which can be found here

The bottom line is that the last year has indeed been exceptionally good, versus a realistic long run back tested Sharpe of 0.88.

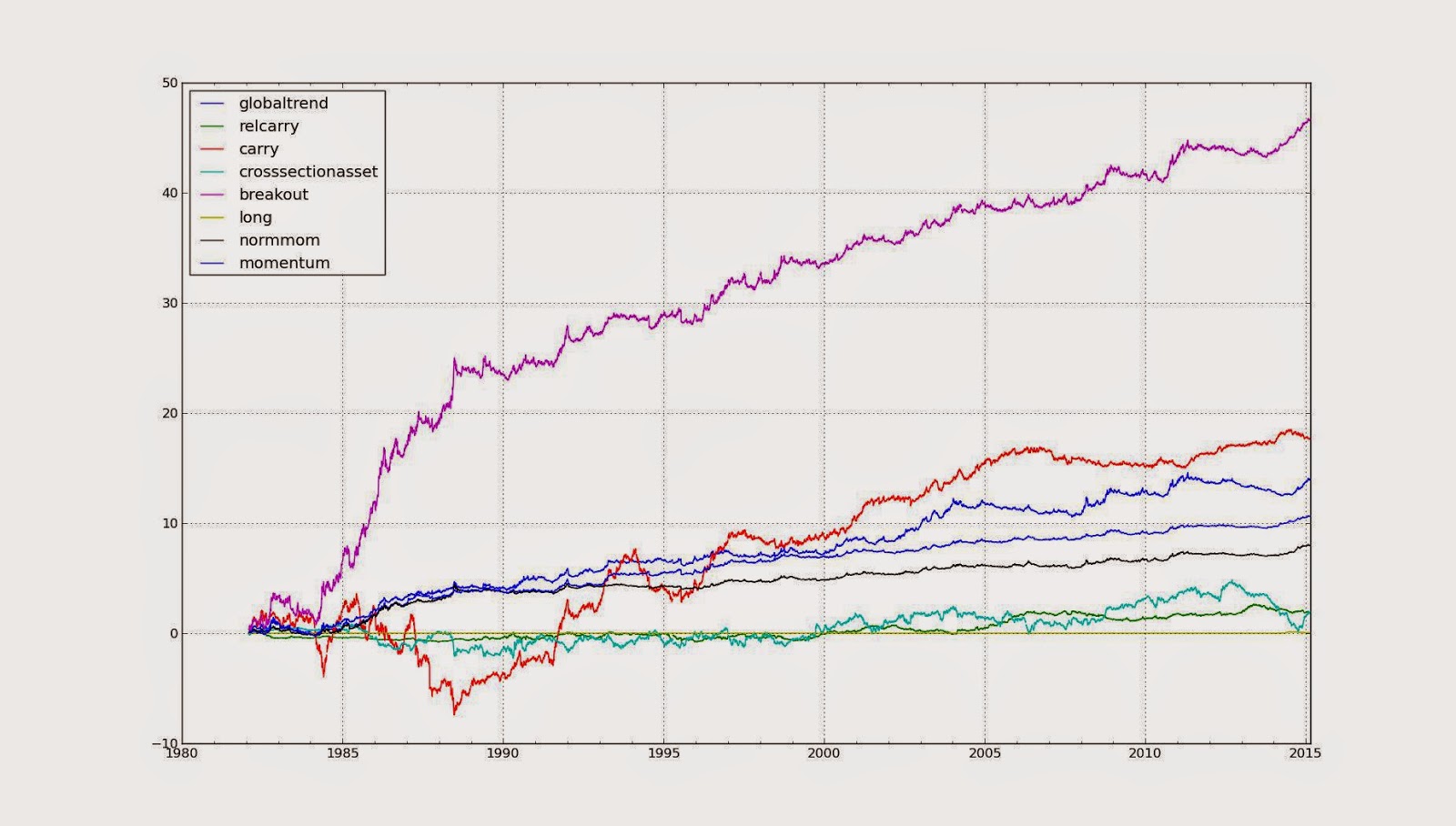

2009, 2011 - 2013 are flat. However 2010 is more interesting, as my backtest made some money whilst the CTA industry generally didn't. I've done a bit more digging since I wrote that post and this is a further breakdown by trading rule:

'globaltrend', 'breakout', 'normmom' and 'momentum' are different flavours of trend following. Although AHL (and I guess other CTA's) use similar versions of these rules (with the possible exception of 'normmom' which is my own entirely original, though very simple, creation) they don't have them in the same proportions as I do. In particular 'momentum', which is an EWMAC system, was a relatively large part of a typical CTA system in 2010*, wheras I have a more equal weighting. The highest blue line (below the red line) is this type of system, which did the worst in 2010.

This scale of outperformance may not be repeatable, but in general I think its better to have a spread of different kinds of trading rules rather than relying too much on one.

* I have no idea what the typical proportions are now.

Hi GAT,

What is the historical max drawdown for your system running at an annual vol target of 25% and the Sharpe Ratio?