Part two of regular update

Risk

Code:

Expected annual risk more than GBP6400 per year, GBP400 per day

code multisignal expected_annual_risk expected_annual_risk_per_contract position expected_annual_risk_rounded_pos

25 EUR -14.9 9531 21455 0 0

24 AUD -13.4 8609 5160 -1 5160

4 WHEAT -10.0 6411 5176 -1 5176

3 SOYBEAN -11.1 7138 6911 -1 6911

27 JPY -19.7 12592 4572 -2 9144

29 NZD -20.0 12812 5111 -2 10223

35 GAS_US -16.0 10247 5251 -2 10503

28 MXP -17.7 11335 1609 -7 11260

17 VIX -18.8 12033 5929 -2 11858

30 COPPER -30.1 19253 7835 -2 15670

33 PLAT -30.1 19253 4768 -4 19074

34 CRUDE_W -35.2 22514 9720 -2 19440

32 PALLAD -35.5 22763 10356 -2 20713

31 GOLD -35.5 22763 8432 -3 25297

21 SMI 11.2 7165 9712 1 9712

10 OAT 15.0 9577 6551 1 6551

36 EDOLLAR 16.7 10676 1474 7 10320

8 BTP 18.3 11692 7415 2 14830

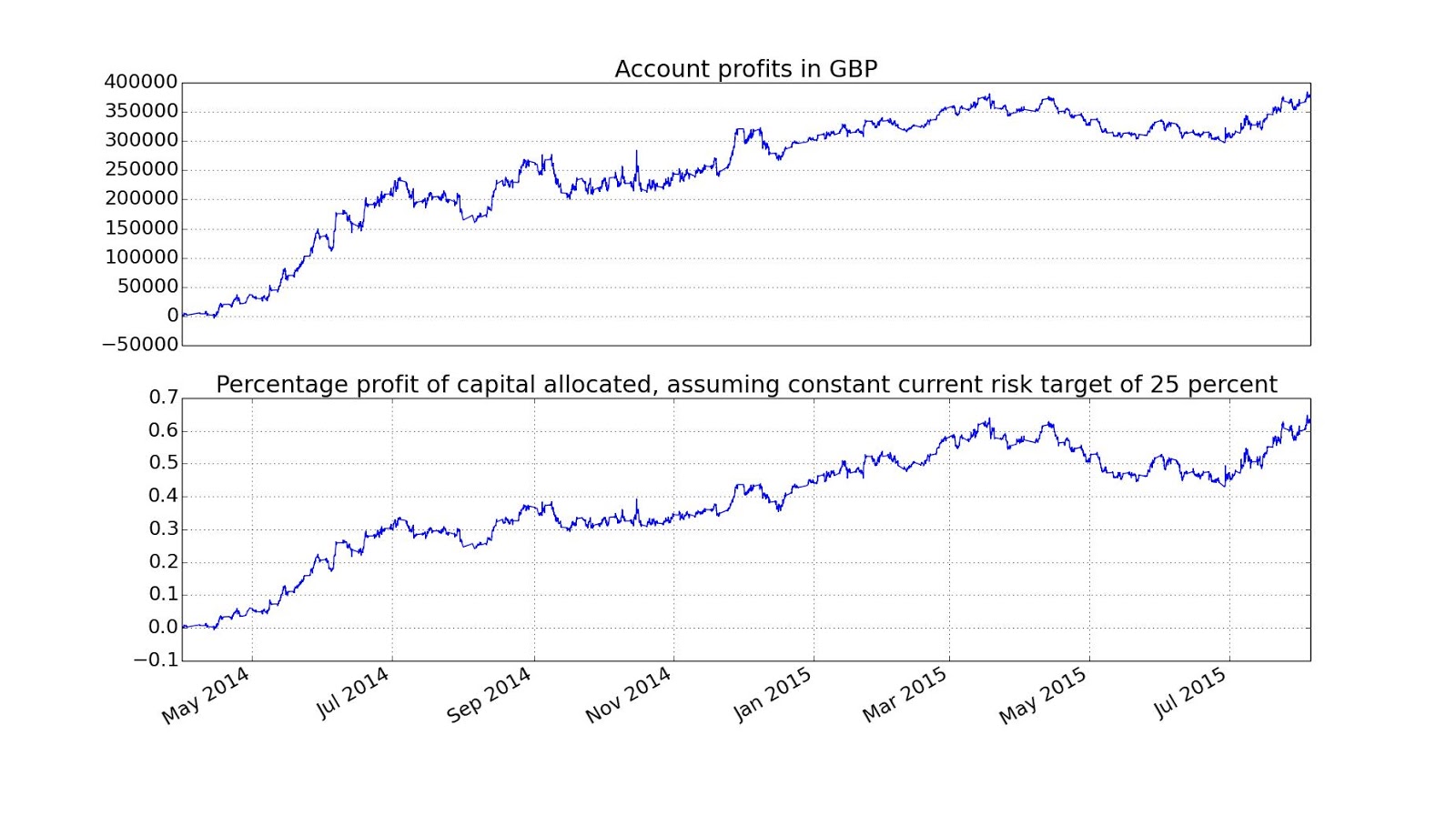

Current expected portfolio risk is @ 121% of average; on 97.7% of maximum capital (due to the drawdown) or in money terms £7371 a day or £118K a year (or if you like, 29.4% of my maximum capital, and 30.1% of my current reduced capital; versus long run targets of 25%).

Risk@121 % of average is slightly up from 118% a couple of weeks ago. My system has hit a risk ceiling (maximum total signal; or if you like the measure of risk that assumes in a crisis all correlations will go to 1 or -1, whichever is worse) which is mostly preventing it from scaling up any further.

Trades

Code:

code contractid filled_datetime filledtrade filledprice

4585 AEX 201508 2015-07-24 07:59:56 -1 491.400000

4660 AUD 201509 2015-07-31 16:00:00 1 0.732900

4684 AUD 201509 2015-08-04 01:25:33 -1 0.725100

4687 AUD 201509 2015-08-04 06:27:51 1 0.733400

4696 AUD 201509 2015-08-04 16:07:59 1 0.740300

4690 BTP 201509 2015-08-04 07:31:58 1 136.710000

4609 CAC 201508 2015-07-27 14:57:56 -1 4948.500000

4693 CAC 201509 2015-08-04 08:05:36 1 5099.000000

4567 COPPER 201512 2015-07-22 14:17:09 -1 2.447500

4633 COPPER 201512 2015-07-28 19:34:12 1 2.420000

4630 CORN 201512 2015-07-28 15:17:10 -1 384.250000

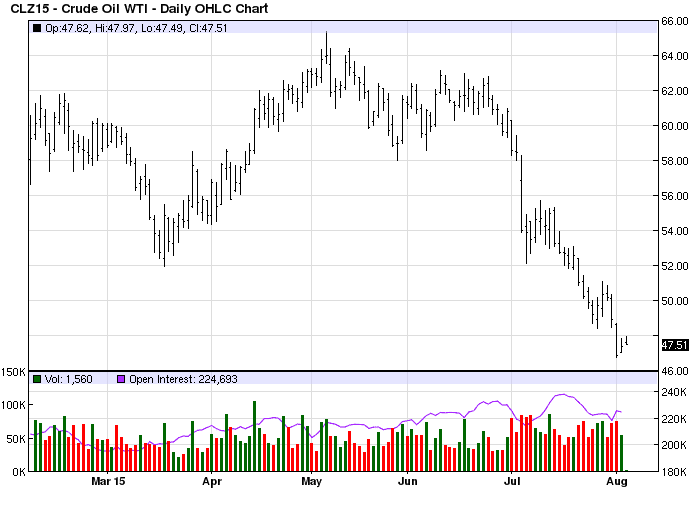

4597 CRUDE_W 201512 2015-07-27 12:10:03 -1 49.330000

4681 CRUDE_W 201512 2015-08-03 17:21:03 1 47.290000

4648 EDOLLAR 201812 2015-07-31 12:10:45 1 97.580000

4594 EUR 201509 2015-07-27 03:26:25 1 1.100900

4600 GAS_US 201510 2015-07-27 12:15:01 -1 2.790000

4666 GAS_US 201510 2015-08-03 12:17:00 -1 2.796000

4570 GBP 201509 2015-07-23 06:14:11 1 1.561700

4576 GBP 201509 2015-07-24 01:45:26 -1 1.550800

4636 GBP 201509 2015-07-29 01:34:55 1 1.560400

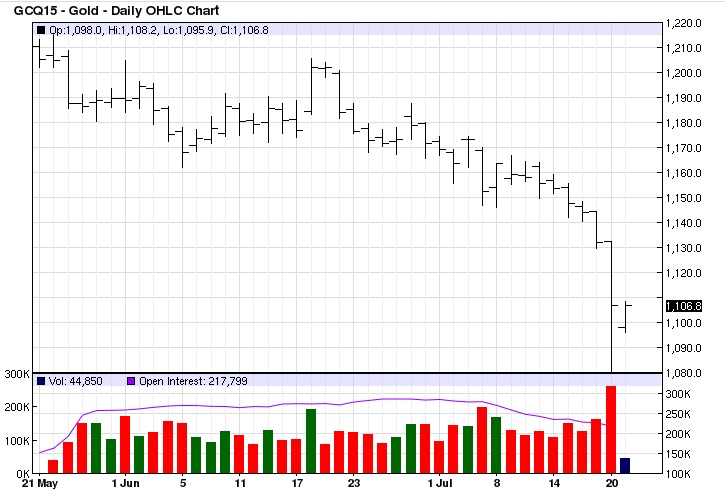

4669 GOLD 201508 2015-08-03 12:35:16 1 1091.000000

4672 GOLD 201512 2015-08-03 12:35:16 -1 1091.000000

4675 GOLD 201508 2015-08-03 12:47:32 2 1090.400000

4678 GOLD 201512 2015-08-03 12:47:32 -2 1090.400000

4699 JPY 201509 2015-08-05 01:43:52 -1 0.008046

4615 KOSPI 201509 2015-07-28 01:26:32 -1 244.000000

4591 KR10 201509 2015-07-27 01:39:29 1 123.700000

4618 MXP 201509 2015-07-28 01:49:46 -1 0.061170

4651 MXP 201509 2015-07-31 13:46:21 1 0.061970

4627 NASDAQ 201509 2015-07-28 14:13:57 -1 4531.500000

4573 NZD 201509 2015-07-23 09:21:14 1 0.665400

4579 NZD 201509 2015-07-24 01:55:11 -1 0.658700

4642 NZD 201509 2015-07-30 15:20:19 1 0.656300

4582 OAT 201509 2015-07-24 07:33:44 1 148.700000

4612 SMI 201509 2015-07-27 15:01:34 -1 9177.000000

4645 SMI 201509 2015-07-31 08:03:49 1 9397.000000

4564 SOYBEAN 201511 2015-07-22 12:02:12 -1 996.500000

4588 SOYBEAN 201511 2015-07-24 12:13:30 -1 978.000000

4639 SOYBEAN 201511 2015-07-29 12:05:00 -1 943.750000

4606 SP500 201509 2015-07-27 14:17:06 -1 2064.250000

4654 SP500 201509 2015-07-31 14:11:16 1 2106.250000

4603 US2 201509 2015-07-27 14:11:34 1 109.507812

4657 US2 201509 2015-07-31 15:47:47 -1 109.539062

4621 V2X 201509 2015-07-28 08:08:28 -1 21.200000

4624 WHEAT 201512 2015-07-28 12:05:09 -1 516.750000

Slippage £72.50 vs £185 expectated

Just to say, if there is any information you'd like to see included in these regular updates, or any questions you have, fire away. It will be far more interesting for me.

There won't be another of these updates for about a month, as I'm taking some holiday. During that time I'll be away from my trading system with only a brief day back at home in late August. That will enable me to do the early quarterly rolls for bond contracts. The monthly rolls for VIX, V2X, AEX and CAC I've already done.

How should one deal with holidays as a slowish automated trader (a day trader can probably not trade)? The first option is to close all your positions. This incurs two lots of slippage (though if you're smart you can do it in conjunction with rolling) - probably several thousand; and opportunity cost from not trading (depending on what I think my Sharpe Ratio is, between £1K and £2K a week lost on average, though it could be a gain). This strikes me as very conservative.

The second option is to keep your positions open, but turn off your trading system so you won't react to anything that happens. If you're trading slowly enough you might just get away with it. Personally that scares me a little.

The third option is to keep your system on, but reduce your risk in some way. You can do this across the board (eg cut all positions in half) or selectively. Last year for example I had some massive short VIX/V2X positions. That kind of negative skew whilst being away from the system was a little worrying. This year I could cut my big shorts in crude and metals. Theoretically it's better just to cut all your positions than to do it selectively. I'm giving this option some serious consideration.

The fourth option is to keep your system on with full initial positions, but only allow trading which reduces your risk (eg closing positions). This is an option which I find tempting.

The final option is of course to let everything run just as it is. I'm a little more confident in my system than I was last summer, but it's still a bit worrying.

If anyone has any thoughts on this, I'd be interested to hear them (before Sunday morning, when I have to action them!).

GAT

")