After briefly reading the first 2 pages, I can see there could be 3 questions.

1. Systemic risk. I think, just unsure whether adding more instruments (like 40 - Pros and Cons) would reduce the portfolio's systemic risk. It could be. I could be most likely not (due to such as some overseas exchanges still close/illiquid during crash).

2. SAR strategy. My guess is using robot for SAR strategy (without your personal ongoing attention) could possibly sometimes encounter huge risk/loss if volatility is drastic. (perhaps back-testing with intraday data would be required/ necessary)

3. Hedge. Just unclear how you perform hedging for the 'A' trading portfolio (while maintaining good returns). ( I assume All your hedge is just for 'B' Investment. If not, then even more confusing!)

1. I guess the definition of systematic risk is that it won't be reduced through diversification. Will it be increased? Are we talking about market risk, or other risks (like market closure, which you mention).

With market risk I think the biggest danger is you add diversification and then ramp up gearing in line with perceived correlation and the fall in vol. I have measures to prevent that; limits on the 'ramping up multiplier' and a check on the total size of my positions assuming all correlations 'go to one'. (

http://www.elitetrader.com/et/index...ed-futures-trading.289589/page-5#post-4092502).

With non market risk; well I suppose spreading across multiple exchanges / clearers is probably safer than not. I'm UK based so nearly all the markets I trade are 'foreign'.

By the way one thing that would worry about cross country trading is where it's done on a relative value basis. Would you want to be long UK / short US after september 11th happened? No way; you'd be getting margin calls on your UK position whilst receiving no benefit from your US short whilst the market was closed.

2. I'm unclear here if you are talking about

a) a sharp jump / gap in prices

b) a sharp move in prices over the day, which for some reason the robot (a term, by the way I hate) doesn't trade out of

c) the robot doing something crazy on a day when prices seesaw up and down wildily.

With (a) I guess humans and robots are both equally vulnerable (although a low latency robot - not what I'm running - would react faster). However you're right that daily market data will give a rosy picture of peak losses compared to intra day.

With (b), perhaps in the event of system failure this is a problem; but this needs to be balanced against the benefit of not having an emotional human debating with itself whether to cut or not; it would just cut.

I think you're talking about (c). Few points to make here:

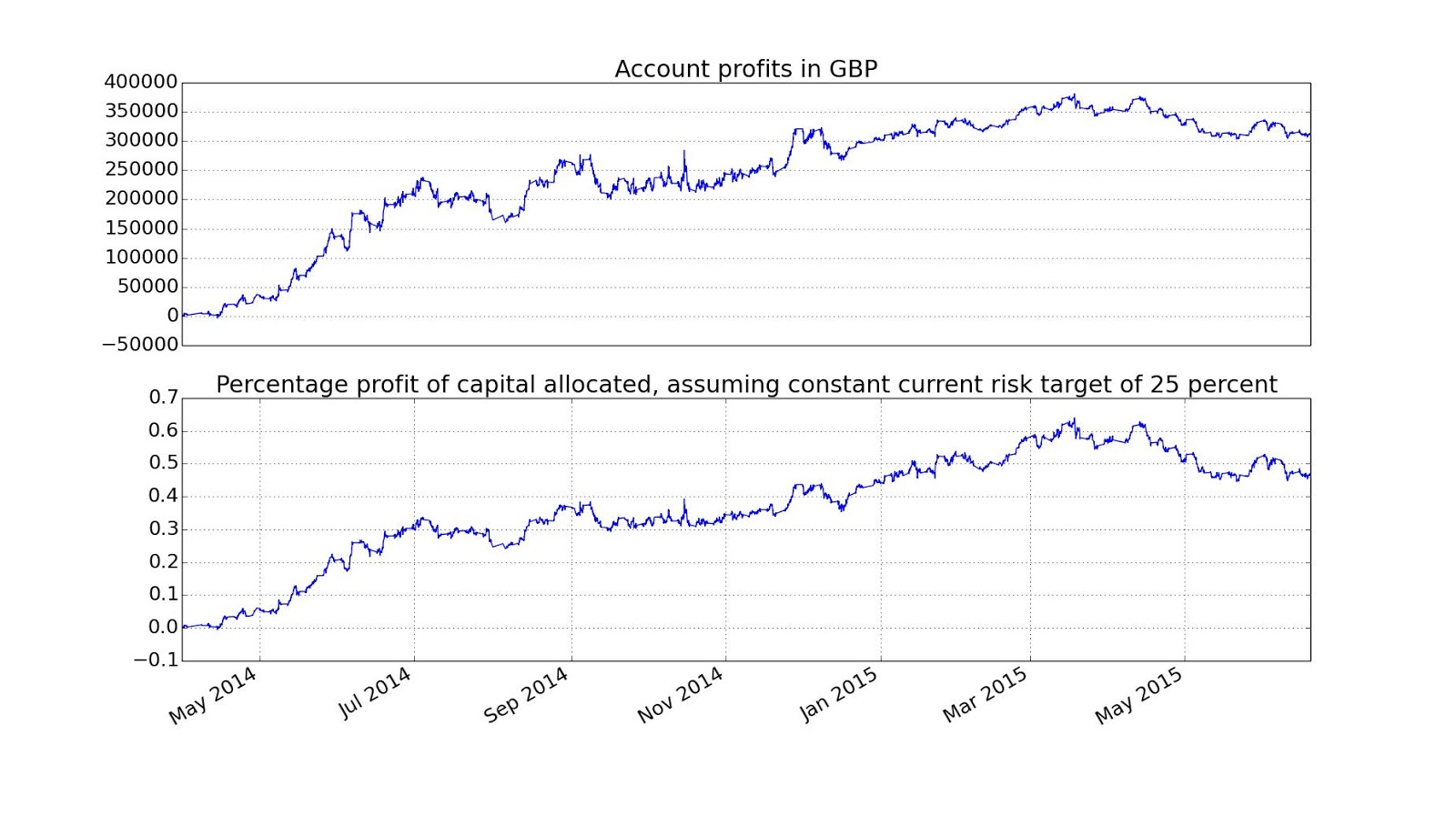

One is I trade relatively slowly (average holding period of perhaps a month), so I don't react much to intraday moves. Suppose I was long Emini and the market dropped 300 points; then reversed and rose 300 points, and then dropped 300 points. On the first drop I would have cut my position massively; partly because the trend has started to fade, mainly because volatility has spiked. On the move up I wouldn't do anything. Volatility hasn't fallen, if anything it's gone up. On the next down move again I wouldn't do anything.

Two, I have controls in place to prevent over trading. The crudest is a limit on the number of contracts I will trade per day. I also have a 'lifetime' limit which I would set before a holiday where I can't monitor my trading.

Here is an excerpt

Code:

run@bilbo ~/workspace/systematic_engine/sysdiag/scripts $ . displaylimits LIVE

EDOLLAR 2015-06-18 12:07:42 Max pos:40 Current pos 5 Max day:10 Done:2 Max all:1000 Done:259

SP500 2015-06-18 06:05:41 Max pos:6 Current pos 0 Max day:2 Done:0 Max all:1000 Done:61

For S&P after I've traded two contracts I'll stop. Right now with a max strength signal I'd own 2 or at most 3 contracts (although the maximum position I'd allow is 6 contracts as shown). A trade of two contracts in a day is plenty (or two trades of one contract each).

Were I to go on holiday I'd set the lifetime limit (max all) maybe to 10 contracts for a 2 week holiday.

Notice the limits for Eurodollar, a lower risk contract, are higher.

3. Hedging.

It's a very simple hedge of two equity portfolios with two equity index futures (eurostoxx and FTSE); roughly delta neutral (or as close I can get given the size of the futures contracts).

GAT