Time for the semi regular update (sorry been busy proofreading the

book [pre-ordering system is now working] and doing

TV stuff).

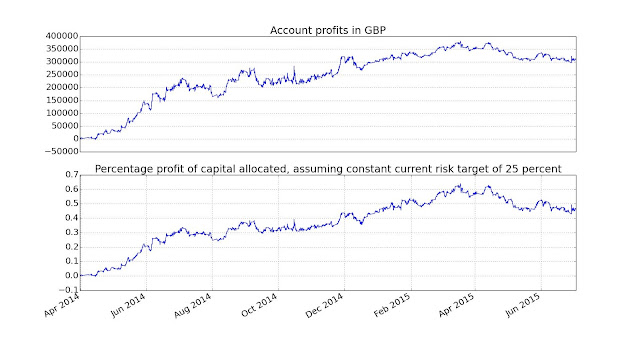

Up a 'massive' 0.4% or £1600 in money terms, although it's been an interesting ride (you can probably see the point at which the greek government decided to shrug their shoulders and say 'sue' me). I had to reduce my Eurostoxx hedge, since it was clear that the beta was all wrong with what was going on.

Drawdown is 17.1%.

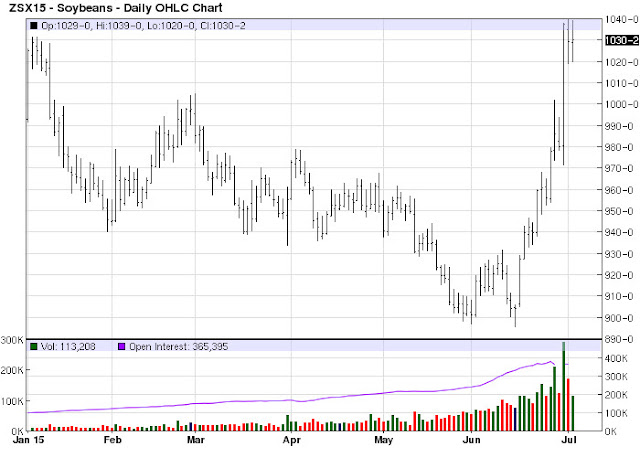

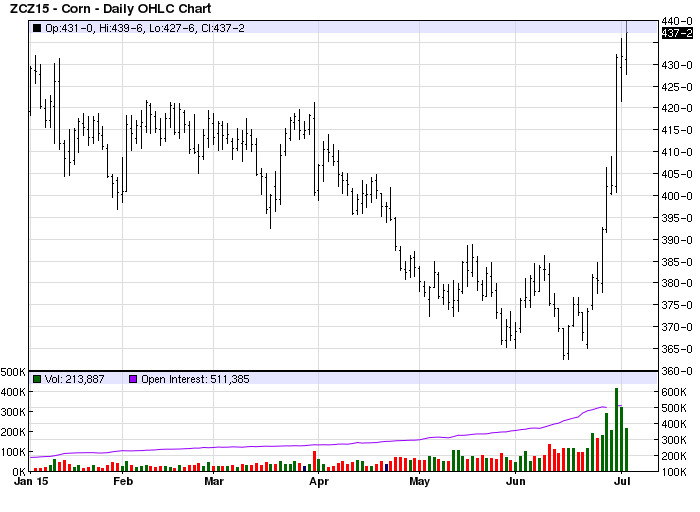

All about the ags complex this fortnight:

Big gainers

Soybeans £8.9K

Wheat £2.6K

NZD £2.4K

PALLAD £1.9K

GOLD £1.8K

MXP £1.8K

Big losers:

Corn -£5.8K

Kospi -£1.6K

Soya: Was long 1 contract 2 weeks ago; now long 3 contracts

Trades:

4267 SOYBEAN 201511 2015-06-22 14:30:00 1 947.250000

4294 SOYBEAN 201511 2015-06-24 15:22:48 1 961.750000

4315 SOYBEAN 201511 2015-06-29 12:15:04 1 985.250000

4375 SOYBEAN 201511 2015-07-02 12:03:36 -1 1029.750000

Corn: Was short 5 contracts two weeks ago; now short just one contract

Trades:

4291 CORN 201512 2015-06-24 14:30:00 1 378.750000

4303 CORN 201512 2015-06-25 18:11:08 1 391.250000

4354 CORN 201512 2015-06-30 17:18:26 1 412.750000

4390 CORN 201512 2015-07-02 14:30:00 1 430.000000

.... I think this is what is known as a 'hedge'. Classic trend following behaviour; one system was the right way round and bought into the strengthening rally (with a little bit of profit taking at the end), the other cut it's position which was the wrong way round.

These are such fascinating moves I will do a blog post in more detail explaining in more detail why I had these two positions on, and why I traded as I did.

Current position:

Code:

code contractid positions Lock WrongContract InFwdNotRoll

1 AUD 201509 -1 False False False

3 BOBL 201509 1 False False False

16 COPPER 201512 -1 False False False

17 CORN 201512 -1 False False False

10 CRUDE_W 201512 -1 False False False

18 EDOLLAR 201812 3 False False False

19 EDOLLAR 201809 2 False False False

11 EUROSTX 201509 -13 False False False (hedge)

2 GAS_US 201509 -1 False False False

8 GOLD 201508 -2 False False False

14 JPY 201509 -1 False False False

6 KR3 201509 6 False False False

9 MXP 201509 -6 False False False

15 NZD 201509 -3 False False False

20 PALLAD 201509 -2 False False False

12 PLAT 201510 -3 False False False

13 SOYBEAN 201511 3 False False False

7 US2 201509 3 False False False

5 US5 201509 1 False False False

0 V2X 201508 3 False False False

4 VIX 201508 -2 False False False

Risk:

Code:

Expected annual risk more than GBP6400 per year, GBP400 per day

code multisignal expected_annual_risk expected_annual_risk_per_contract position expected_annual_risk_rounded_pos

25 EUR -23.4 14867 38552 0 0

24 AUD -11.4 7227 5549 -1 5549

30 COPPER -16.3 10342 6898 -1 6898

34 CRUDE_W -15.8 10039 9963 -1 9963

28 MXP -16.1 10227 1845 -6 11067

17 VIX -20.6 13104 5852 -2 11704

33 PLAT -25.6 16259 4882 -3 14645

31 GOLD -32.1 20418 8127 -2 16254

29 NZD -23.1 14677 5472 -3 16415

32 PALLAD -26.5 16858 9646 -2 19292

36 EDOLLAR 11.7 7466 1757 5 8786

3 SOYBEAN 35.5 22576 7342 3 22026

This is a new table so let me explain. 'multisignal' is the signal I have on. 'expected annual risk expected' is the risk I would ideally have on if I could buy/sell partial contracts (in £ of annualised standard deviation). 'annal_risk_per_contract' is the risk of each contract. 'position' is in contracts. 'annual_risk_rounded' is the risk I actually have on. So you can see the effects of rounding; I'd like to have a EUR position on but each contract has an enormous risk so I can't justify it.

Current expected portfolio risk is @ 95% of average; on 82% of maximum capital (due to the drawdown) or in money terms £4,880 a day or £78K a year (or if you like, 19.5% of my maximum capital, and 23.7% of my current reduced capital; versus long run targets of 25%).

Trades:

Code:

code contractid filled_datetime filledtrade filledprice

4306 AUD 201509 2015-06-29 01:29:33 -1 0.759200

4372 BOBL 201509 2015-07-02 07:32:49 1 129.590000

4264 BTP 201509 2015-06-22 07:34:45 1 131.260000

4291 CORN 201512 2015-06-24 14:30:00 1 378.750000

4303 CORN 201512 2015-06-25 18:11:08 1 391.250000

4354 CORN 201512 2015-06-30 17:18:26 1 412.750000

4390 CORN 201512 2015-07-02 14:30:00 1 430.000000

4312 CRUDE_W 201512 2015-06-29 12:09:45 -1 59.480000

4255 EUROSTX 201509 2015-06-19 13:53:52 -10 3478.000000

4336 EUROSTX 201509 2015-06-30 08:06:16 3 3460.000000

4363 EUROSTX 201509 2015-07-01 07:59:58 3 3465.000000

4366 EUROSTX 201509 2015-07-01 19:59:09 -1 3474.000000

4252 FTSE 201509 2015-06-19 13:46:46 2 6677.500000

4273 GAS_US 201508 2015-06-23 12:02:37 1 2.768000

4276 GAS_US 201509 2015-06-23 12:02:37 -1 2.782000

4261 GBP 201509 2015-06-22 02:39:42 1 1.587800

4282 GBP 201509 2015-06-23 13:51:13 -1 1.573100

4249 GOLD 201508 2015-06-19 12:05:23 1 1200.200000

4279 GOLD 201508 2015-06-23 12:09:48 -1 1181.800000

4300 GOLD 201508 2015-06-25 12:10:40 -1 1172.900000

4360 JPY 201509 2015-07-01 01:45:00 1 0.008167

4369 JPY 201509 2015-07-02 06:01:53 -1 0.008113

4270 KOSPI 201509 2015-06-23 02:42:08 1 255.250000

4297 KR3 201509 2015-06-25 01:48:59 1 108.970000

4387 MXP 201509 2015-07-02 12:38:43 -1 0.062870

4285 NASDAQ 201509 2015-06-23 14:41:02 1 4537.000000

4318 NASDAQ 201509 2015-06-29 14:08:05 -1 4429.000000

4393 NZD 201509 2015-07-02 18:20:29 -1 0.668300

4309 PALLAD 201509 2015-06-29 12:08:42 -1 670.750000

4378 PALLAD 201509 2015-07-02 12:09:34 1 695.850000

4342 PLAT 201507 2015-06-30 12:01:36 2 1081.700000

4345 PLAT 201510 2015-06-30 12:01:36 -2 1082.700000

4348 PLAT 201507 2015-06-30 12:04:28 1 1081.500000

4351 PLAT 201510 2015-06-30 12:04:28 -1 1082.500000

4267 SOYBEAN 201511 2015-06-22 14:30:00 1 947.250000

4294 SOYBEAN 201511 2015-06-24 15:22:48 1 961.750000

4315 SOYBEAN 201511 2015-06-29 12:15:04 1 985.250000

4375 SOYBEAN 201511 2015-07-02 12:03:36 -1 1029.750000

4288 SP500 201509 2015-06-23 14:44:03 1 2116.500000

4321 SP500 201509 2015-06-29 14:11:26 -1 2075.000000

4258 US5 201509 2015-06-19 14:36:31 1 119.328125

4333 VIX 201508 2015-06-29 17:12:02 1 16.400000

4339 VIX 201508 2015-06-30 11:08:56 1 16.600000

4357 WHEAT 201512 2015-06-30 18:23:59 1 603.750000

Slippage was £192 vs £204 expected (so my simple execution algo saved me £12).