This is why out of sample testing and actual trading are useful.

This is why curated non-obvious data sets are important.

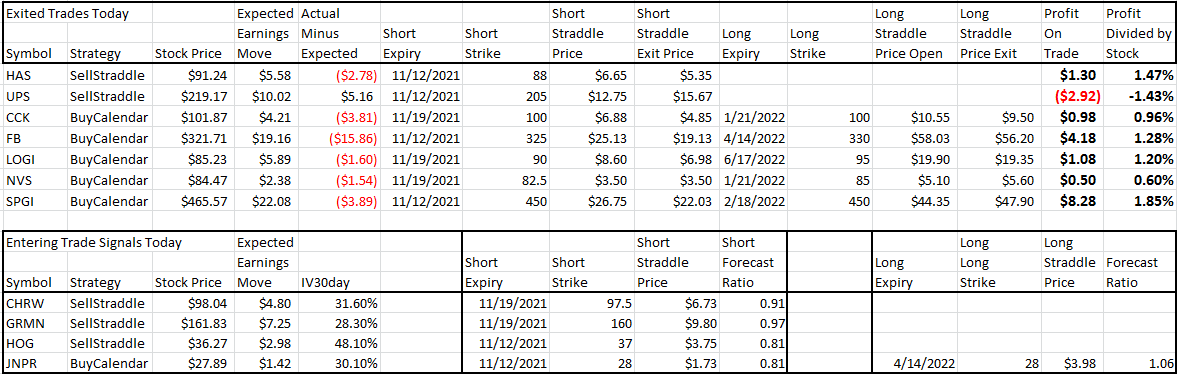

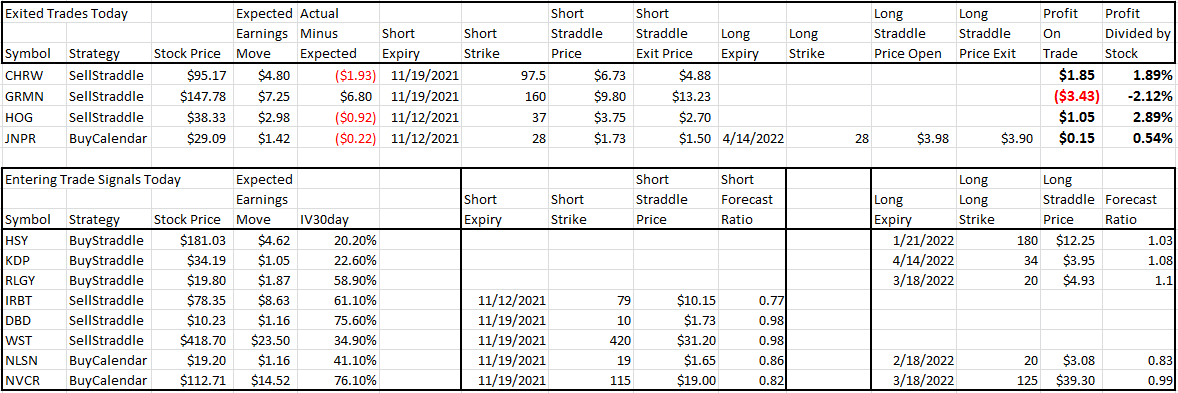

This is how edge is developed and determined.

What makes the data curated non-obvious?

My working theory is that the calendar performs better because it takes advantage of the (curated non-obvious) data better than the other strategies tested. The calendar benefits from estimates of earnings moves, where IV will fall after earnings, good HV calculations, term skew modelling, and theoretical values to identify the trades.

- Earnings move estimates use residual straddle valuations based on distributions developed with years of actual earnings moves and IV crush related data.

- Ex earnings IV modelling utilizes term structure shapes developed from years of data.

- Forecasted theoretical values utilzes forecasts of HV, long-term cross sectional IV analysis, slope and derivative short and long term forecasts, and earnings moves.

Testing with superior data is the way to verify, tweak, and ultimately develop a successful trading strategy.

How is this not overfitting