Being cheeky or serious? I assume you may be referring to the VIX, which I don't happen to know much about other than the fact that it may not be very accurate for tracking actual volatility.

I track volatility for my chosen instrument (ES) in several clever ways, but my price database is currently not updated. It will be in a month or so and then I'll come back to this thread and see if your 'truth' was the truth.

I do however suspect that they volatility I was referring to when starting this thread has NOT been the norm for the last 2-3 years.

You're absolutely correct...when you started this thread on Tuesday February 9th and using the VIX as your chosen volatility measurement...the VIX open @ 28.3 and closed @ 26.7

The volatility you saw on that trading day and from January 1st to February 9th was NOT the norm for the past 2 - 3 years. In fact, it was above the norm of year 2013 of 14.7, year 2014 of 14.5 and year 2015 of 17.5 based upon the average closing prices of the VIX per month.

In contrast, in my own personal databse, I prefer to use all data (every tick) instead of the average monthly close and Tuesday February 9th is still way above the norm. I also have my own personal (private) way to measure volatility in any trading instrument and for the Emini ES futures for the past 3 years...Tuesday February 9th was approximately 71.68 % above its norm.

In fact, in my personal database...January set a 10 year record involving the speed in the price action movement in the Emini ES futures during certain times of the trading day involving the Emini ES futures. In addition, the Emini TF futures set a 6 year speed record...same with the other Emini futures. Most of that is attributed to algorithm systems from around the world.

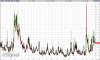

Simply, just looking (visually) at the traditional volatility measurement called the VIX...anybody can pull up a chart of the VIX and see that any time it goes above 18 its NOT the norm and they can see that it doesn't last too long. Therefore, enjoy it while it last if you're someone that profits from such. In contrast, if you're someone that prefers low volatility conditions as in you tend to get more losses in high volatility...you should be on the sidelines (no trades) right now and waiting for it to decline back to the norm.

As Amalgam stated in this thread...volatility is mean reverting. It always goes back to norm until the next global event triggers high volatility conditions. In fact, my documentation of the VIX (since its birth)...it can only spike above 25 due to a global event that impacts many key markets at the same time regardless if that event was trigger by the U.S, Europe or Asia.

Markets are more globally connected today than ever before and growing.

Also, as a reminder, some retail traders prefer volatility above the norm and others prefer volatility below the norm. Only your history of your real trading results measure against whatever volatility measurement you're using will tell you when you should be trading and when you should not be trading...

Volatility also gives lots of clues about position size management, when trend days are most likely to appear and many other wealth of information. In fact, think about this...financial institutions don't ignore it...retail traders should not ignore it too.

Attachments

Last edited: