taken from seekingalpha:

US Government's New Housing Bubble

by Jeff Nielson

December 11, 2009

As readers here have heard regularly, it is absolutely certain that there will be another down-leg for the U.S. housing market, beginning no later than spring of next year. We already know the latest date, since that is when the next spike in U.S. mortgage resets kicks-in.

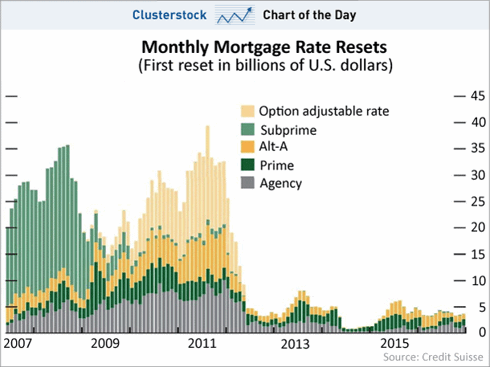

There are two differences between the first spike in mortgage resets and the second. Not only will the second spike last for at least two years (longer than the first), but it will be much nastier. A chart from Credit Suisse spells this out perfectly.

Roughly 75% of these mortgages are either âoption-ARMâ loans, âAlt-Aâ loans, or âagencyâ loans (i.e. from Fannie (FNM)/Freddie (FRE)/FHA), with still a few, remaining sub-prime loans sprinkled into the mix. Put another way, only about ¼ of the these mortgages are âprimeâ - a word which certainly doesn't mean what it used to, given that these âprimeâ mortgages are also experiencing their highest level of defaults in history.

The largest category are the option-ARMs, the category of loans which has already had the highest level of defaults. With the vast majority of these mortgage-holders having made minimum payments (or less) on these mortgages, their monthly mortgage payments will increase to multiples of their current payments â even with interest rates at record-lows.

The next-largest category in this group, the so-called âAlt-Aâ loans were supposed to be of a better quality than sub-prime. However, with default rates on Alt-A mortgages approaching the levels for sub-prime (given that many Alt-A mortgages were also âliar's loansâ), it is clear that this supposed higher quality was yet one more fiction in this massive bubble.

Then we have the âagencyâ mortgages, from the money-hemorrhaging entities Fannie Mae, Freddie Mac, and now the FHA. If the massive losses which these quasi-government entities have already suffered on previous loans isn't enough to frighten people about the future defaults coming from this source, then their current lending practices should certainly do the trick.

Providing over 90% of all mortgage-funding for new home loans, the U.S. government has essentially nationalized the U.S. mortgage-market (âinsuredâ by taxpayers), but with the free-loading banker-oligarchs able to insert themselves as âmiddlemenâ - taking a cut of profits for themselves, while having zero, personal risk (the new âbusiness modelâ for the U.S. banking oligarchy).

If this level of risk for the U.S. government is not proof enough of insanity, in itself, then its âlending standardsâ (or lack thereof) clearly pushes it past that threshhold. The same U.S. government which is taking miniscule down-payments on these mortgages (90% of which are only 4% or less) with one hand, is handing out an $8,000 cheque (again paid for by taxpayers) with the other hand.

The net effect is that for virtually every new mortgage which these government entities are initiating of $250,000 or less there is zero (net) down-payment. Given that a large majority of current sales in the U.S. are below this level, this means that most of the home-buyers in the U.S. this year are putting up zero down-payments.

To perfect their new Ponzi-scheme for the U.S. housing market, the Federal Reserve allows the banksters to âborrowâ money at 0%. The banksters then âdepositâ this money with the Federal Reserve as a âsavings accountâ for which they collect interest, while paying no interest on the âloanâ. In other words the Federal Reserve is simply giving the banksters free money (they are currently collecting interest on over $1 trillion of these âloansâ).

But the money doesn't actually sit there. Instead the Fed uses that money to buy U.S. mortgage bonds â the only thing keeping U.S. mortgage rates several percent lower than they would be otherwise. So, to begin with, the new Ponzi-scheme implodes as soon as the U.S. government stops âbuyingâ its own mortgage bonds (with 100% of the money used to âbuyâ those bonds simply being printed on Bernanke's magic printing-press).

Obviously, even the U.S. government can only soak-up so many trillions of dollars in this manner without taking the U.S. dollar down to zero. So we already know this next Ponzi-scheme will end badly. The U.S. government is initiating millions of new mortgages, to questionable buyers, at interest rates which can only remain artificially low for as long as the U.S. keeps âbuyingâ all of its own mortgage bonds.

However, this new (and even more fraudulent) bubble is taking place at a time when:

U.S. mortgage defaults and delinquencies are at all-time record levels

U.S. banks are holding millions of foreclosed properties off the market

Millions more homes are already in the âforeclosure pipelineâ

U.S. unemployment continues to worsen (even the phony numbers)

U.S. banks are still starving the economy of credit

Record numbers of homeowners are already âunderwaterâ

A second, larger, worse spike in U.S. mortgage resets is about to begin

Retiring baby-boomers need to sell at least $1 trillion in real estate

Does this seem like the time that U.S. taxpayers should be bank-rolling the entire U.S. mortgage market, with most of those new mortgages being zero down-payment loans (and in many cases to people of questionable creditworthiness)?

Keep this analysis in mind the next time you hear some clueless, talking-head talk about a âbottomâ in the U.S. housing market.

US Government's New Housing Bubble

by Jeff Nielson

December 11, 2009

As readers here have heard regularly, it is absolutely certain that there will be another down-leg for the U.S. housing market, beginning no later than spring of next year. We already know the latest date, since that is when the next spike in U.S. mortgage resets kicks-in.

There are two differences between the first spike in mortgage resets and the second. Not only will the second spike last for at least two years (longer than the first), but it will be much nastier. A chart from Credit Suisse spells this out perfectly.

Roughly 75% of these mortgages are either âoption-ARMâ loans, âAlt-Aâ loans, or âagencyâ loans (i.e. from Fannie (FNM)/Freddie (FRE)/FHA), with still a few, remaining sub-prime loans sprinkled into the mix. Put another way, only about ¼ of the these mortgages are âprimeâ - a word which certainly doesn't mean what it used to, given that these âprimeâ mortgages are also experiencing their highest level of defaults in history.

The largest category are the option-ARMs, the category of loans which has already had the highest level of defaults. With the vast majority of these mortgage-holders having made minimum payments (or less) on these mortgages, their monthly mortgage payments will increase to multiples of their current payments â even with interest rates at record-lows.

The next-largest category in this group, the so-called âAlt-Aâ loans were supposed to be of a better quality than sub-prime. However, with default rates on Alt-A mortgages approaching the levels for sub-prime (given that many Alt-A mortgages were also âliar's loansâ), it is clear that this supposed higher quality was yet one more fiction in this massive bubble.

Then we have the âagencyâ mortgages, from the money-hemorrhaging entities Fannie Mae, Freddie Mac, and now the FHA. If the massive losses which these quasi-government entities have already suffered on previous loans isn't enough to frighten people about the future defaults coming from this source, then their current lending practices should certainly do the trick.

Providing over 90% of all mortgage-funding for new home loans, the U.S. government has essentially nationalized the U.S. mortgage-market (âinsuredâ by taxpayers), but with the free-loading banker-oligarchs able to insert themselves as âmiddlemenâ - taking a cut of profits for themselves, while having zero, personal risk (the new âbusiness modelâ for the U.S. banking oligarchy).

If this level of risk for the U.S. government is not proof enough of insanity, in itself, then its âlending standardsâ (or lack thereof) clearly pushes it past that threshhold. The same U.S. government which is taking miniscule down-payments on these mortgages (90% of which are only 4% or less) with one hand, is handing out an $8,000 cheque (again paid for by taxpayers) with the other hand.

The net effect is that for virtually every new mortgage which these government entities are initiating of $250,000 or less there is zero (net) down-payment. Given that a large majority of current sales in the U.S. are below this level, this means that most of the home-buyers in the U.S. this year are putting up zero down-payments.

To perfect their new Ponzi-scheme for the U.S. housing market, the Federal Reserve allows the banksters to âborrowâ money at 0%. The banksters then âdepositâ this money with the Federal Reserve as a âsavings accountâ for which they collect interest, while paying no interest on the âloanâ. In other words the Federal Reserve is simply giving the banksters free money (they are currently collecting interest on over $1 trillion of these âloansâ).

But the money doesn't actually sit there. Instead the Fed uses that money to buy U.S. mortgage bonds â the only thing keeping U.S. mortgage rates several percent lower than they would be otherwise. So, to begin with, the new Ponzi-scheme implodes as soon as the U.S. government stops âbuyingâ its own mortgage bonds (with 100% of the money used to âbuyâ those bonds simply being printed on Bernanke's magic printing-press).

Obviously, even the U.S. government can only soak-up so many trillions of dollars in this manner without taking the U.S. dollar down to zero. So we already know this next Ponzi-scheme will end badly. The U.S. government is initiating millions of new mortgages, to questionable buyers, at interest rates which can only remain artificially low for as long as the U.S. keeps âbuyingâ all of its own mortgage bonds.

However, this new (and even more fraudulent) bubble is taking place at a time when:

U.S. mortgage defaults and delinquencies are at all-time record levels

U.S. banks are holding millions of foreclosed properties off the market

Millions more homes are already in the âforeclosure pipelineâ

U.S. unemployment continues to worsen (even the phony numbers)

U.S. banks are still starving the economy of credit

Record numbers of homeowners are already âunderwaterâ

A second, larger, worse spike in U.S. mortgage resets is about to begin

Retiring baby-boomers need to sell at least $1 trillion in real estate

Does this seem like the time that U.S. taxpayers should be bank-rolling the entire U.S. mortgage market, with most of those new mortgages being zero down-payment loans (and in many cases to people of questionable creditworthiness)?

Keep this analysis in mind the next time you hear some clueless, talking-head talk about a âbottomâ in the U.S. housing market.

")