You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Why we haven't hit the bottom: Alt-A and Option ARM Mortgage Resets are coming

- Thread starter daveportman

- Start date

What's another trillion in bailout money? At this point what does it matter?

I'm not upside down but got a nice shock last month. I have a 800 FICO score and 6 figure salary and my only debt is the mortgage that I took out 2 years ago. I'm currently on a 6.0% 10 year ARM and looked to refinance down to a 4.5% 5 year ARM (plan to sell in 5 years and move as kids will be gone) and save $400/month. Maybe spend the $400 on stimulating the economyQuote from slapshot:

The far bigger problem is all of the people that are upside down on their houses and stuck in a some-what high fixed rate, say 6.5 or so. This is a whole crapload of people that can't re-fi becuase their house won't appraise, and our dumbshit government hasn't figured out we desperately need Conforming Streamline loans (no appraisal or income check, just the same balance at a lower rate)

.......................

") . So what a surprise to be declined by bank. The appraisal and comparable sales in our well-to-do town have dropped our home value 30%. Bank also wants a minimum 25% (use to be 20%) equity.

. So what a surprise to be declined by bank. The appraisal and comparable sales in our well-to-do town have dropped our home value 30%. Bank also wants a minimum 25% (use to be 20%) equity. Now multiply this scenario out many times over and the FED and banks could drops i-rates to zero and it won't help the economy here (will help the banks though).

Now overseas most mortgage holders have floating mortgage rates, as soon as their central banks lower rates the banks follow suit. Australia and similar countries will recover faster than the US as they have already lowered rates for their countries home owners. In fact home sales and prices are stabilizing and starting to climb.

We are stuffed.

this is partly why the fed wants to keep treasury rates low, because prime ARMs are based on intermediate-term rates (typically libor 1 year or MTA). as long as those rates are low, the resetting of the ARMs won't be a problem.

someone with a prime ARM that's resetting now would likely see a rate of 4.25%-4.625% -- that's probably better than what their fixed rate was.

someone with a prime ARM that's resetting now would likely see a rate of 4.25%-4.625% -- that's probably better than what their fixed rate was.

Quote from blackjack007:

this is partly why the fed wants to keep treasury rates low, because prime ARMs are based on intermediate-term rates (typically libor 1 year or MTA). as long as those rates are low, the resetting of the ARMs won't be a problem.

someone with a prime ARM that's resetting now would likely see a rate of 4.25%-4.625% -- that's probably better than what their fixed rate was.

Yeah thats why its hard to judge what the impact of the Alt-A resets will be. If there was a way to determine what index those Alt-a and payoption arms were tied to then it would be easier to figure out if this is gonna be a mess or not. My ARM is tied to the CMT and it adjusted down to 4.25% for this year and it looks like its heading to 3.25% next year. It can only go up or down by 1% per year. So I have a pretty good setup even though I've got resets so who knows how many of those Alt-As are similar to mine and how many arent'.

Quote from blackjack007:

this is partly why the fed wants to keep treasury rates low, because prime ARMs are based on intermediate-term rates (typically libor 1 year or MTA). as long as those rates are low, the resetting of the ARMs won't be a problem.

someone with a prime ARM that's resetting now would likely see a rate of 4.25%-4.625% -- that's probably better than what their fixed rate was.

EXACTLY.

For the sake of clarity on this discussion:

ALT-A loans typically refer to light or low or no documentation - the term does not designate if the loan is fully fixed or ARM (with some kind of fixed period)

ARM loans can be high quality, low-margin products that will adjust down. Or they can be crappy, high-margin products with a big reset up.

ARM's can be: Conforming, Alt-A, Sub-Prime or Portfolio - all are different.

For the last 50 years, ARM products have been successfully used and have not caused problems. They only adjust incrementally in normal markets if the margin is reasonable.

In fact, for most people, they are a smarter choice than paying a higher fixed rate. Most people only stay in a mortgage for about 4 years on average. The 5/1 ARM (again, a high quality one) saves the average person about $5k to $15k in payments over the 5 year fixed period when compared to a 30 year fixed.

It is only the slew of high-margin Sub-Prime products recently introduced that caused some issues. They were only fixed for 2 years, had big prepayment penalties and high margins, up to 400% higher.

All that being said, it is the equity collapse after an insane up-run of prices that caused the problem. It is not ARM resets.

There are as many people foreclosing on fixed rate loans as ARM's. The problem, no matter what loan they have, is that they are either upside-down or have a high rate - or both.

If they have both problems, they are very high risk to foreclose.

THE ONLY WAY that this problem can be solved is STREAMLINE (no appraisal, rate/term only no cash out re-fi's) just like FHA and VA already allow.

If we do not do this on Conventional mortgages, the foreclosure crisis will continue unabated.

But our shitty Congress and now our Administration is choosing to ignore this reality and has for about 1.5 years now. They prefer Loan Modifications - which are only good in the long run for legal firms and lawyers, no one else.

ALT-A loans typically refer to light or low or no documentation - the term does not designate if the loan is fully fixed or ARM (with some kind of fixed period)

ARM loans can be high quality, low-margin products that will adjust down. Or they can be crappy, high-margin products with a big reset up.

ARM's can be: Conforming, Alt-A, Sub-Prime or Portfolio - all are different.

For the last 50 years, ARM products have been successfully used and have not caused problems. They only adjust incrementally in normal markets if the margin is reasonable.

In fact, for most people, they are a smarter choice than paying a higher fixed rate. Most people only stay in a mortgage for about 4 years on average. The 5/1 ARM (again, a high quality one) saves the average person about $5k to $15k in payments over the 5 year fixed period when compared to a 30 year fixed.

It is only the slew of high-margin Sub-Prime products recently introduced that caused some issues. They were only fixed for 2 years, had big prepayment penalties and high margins, up to 400% higher.

All that being said, it is the equity collapse after an insane up-run of prices that caused the problem. It is not ARM resets.

There are as many people foreclosing on fixed rate loans as ARM's. The problem, no matter what loan they have, is that they are either upside-down or have a high rate - or both.

If they have both problems, they are very high risk to foreclose.

THE ONLY WAY that this problem can be solved is STREAMLINE (no appraisal, rate/term only no cash out re-fi's) just like FHA and VA already allow.

If we do not do this on Conventional mortgages, the foreclosure crisis will continue unabated.

But our shitty Congress and now our Administration is choosing to ignore this reality and has for about 1.5 years now. They prefer Loan Modifications - which are only good in the long run for legal firms and lawyers, no one else.

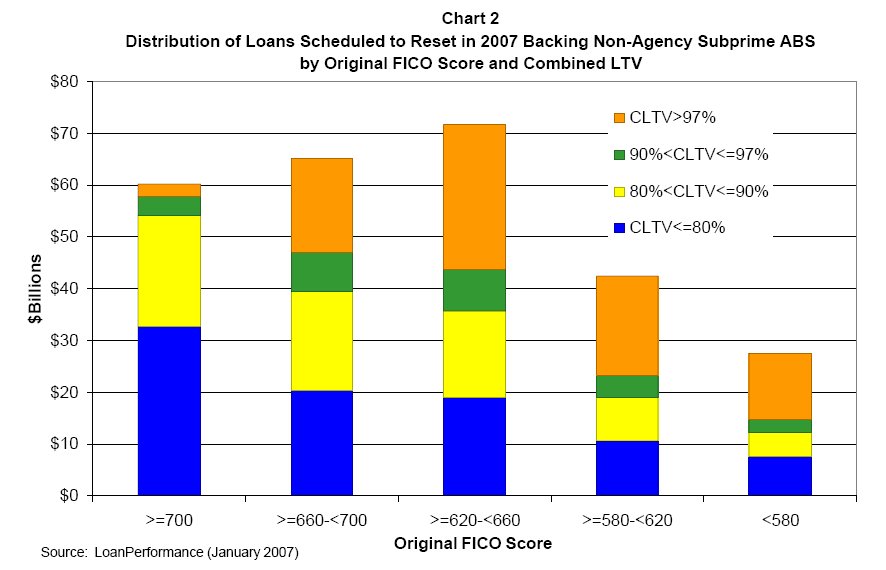

I have not acces to the 2009 figures...maybe someone may help out ?

Thx for the great summary, slapshot, and I am in agreement with you. It's all about collateral or, rather, lack thereof.