If you can't easily make money from it, the prices are correct.

"Ohhhhh, there's that whole reality thing again....."

If you can't easily make money from it, the prices are correct.

No, I do not. Your definition is different than mine and I'm not interested in this debate anymore. If you can't easily make money from it, the prices are correct.

I'm not interested in this debate anymore.

Since you're both blind and dumb, let me just quote Robert:

"yes, but Put/Call party includes dividends and cost of carry"

"There is still put-call parity"

This means that put-call parity always holds.

Is this clear now? Oh, you're blind so it may still not be clear. Too bad.

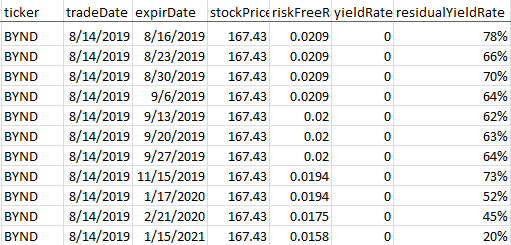

Here's how we handle this situation. We create a residual yield rate to line up the calls and puts. For BYND the residual rate is the market's implied borrow rate.

For Robert's example, the Sep implied borrow is 63%. This lines up the call and put IVs to about a 55%.

When you have a systematic way to calculate borrow, you can compare (as Robert says) the implied borrow to your borrow rate.

You can also graph the borrow.

We graph the constant maturity borrow at 30 days and 2 years to expiration interpolated. Above is the borrow at 30 days.

Notice how borrow spikes when the stock runs up.

Guru ... the name itself is one of life's delicious ironies ... still believe that put-call parity always holds ... or like Bob ... just not interested in this debate anymore ?

It depends on how you look at it. Bob is explaining in a VERY professional way. Most likely hard to understand for a non pro though. Guru is also right, albeit less patient.

P/C parity always holds.

Here we go again

... when Bob lost the argument about p-c parity ... he claimed he just wasn't interested in the debate any more

If you think p-c parity always holds, then try to do what Bob/Guru refused to do

... and explain why it always holds when the following example clearly shows that it doesn't

For American Style options

... Spot $100

... with 30 days to expiry

... IV 20%

... interest rates 0%

... Dividend $10

... $80 strike shows a put-call difference / inequality of 9.9643

View attachment 207785

Of course, you may be confusing p-c parity with non-arbitrage

... but that is a different subject