You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

When P-C parity does not hold

- Thread starter Baozi

- Start date

Matt_ORATS

Sponsor

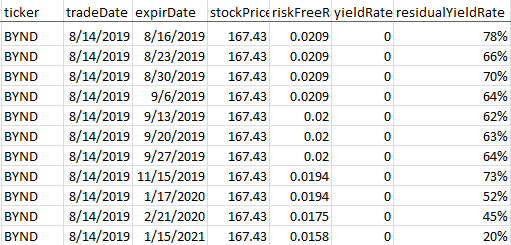

Here's how we handle this situation. We create a residual yield rate to line up the calls and puts. For BYND the residual rate is the market's implied borrow rate.Yes and no. The trading platform will use a default interest rate and dividend flow. It will not adjust for very hard to borrow or your rate. Here is an example. BYND is very hard to borrow. The Sept ATM calls are 38.11 and the pouts are 82.95. There is still put-call parity but the default rate of 1.68% (10 year T-bill). That is not accurate for this symbol. I'd have to put in my cost to short it. Then add extra because you can't get a locate.

View attachment 207053

For Robert's example, the Sep implied borrow is 63%. This lines up the call and put IVs to about a 55%.

When you have a systematic way to calculate borrow, you can compare (as Robert says) the implied borrow to your borrow rate.

You can also graph the borrow.

We graph the constant maturity borrow at 30 days and 2 years to expiration interpolated. Above is the borrow at 30 days.

Notice how borrow spikes when the stock runs up.

Yes. Absolutely. I'd even go so far as to say, "Typical" of every major divot on the S&P over the last decade.

"...Stop playing...?" That depends on what you do now, right? This all signals danger. Danger means risk. Along with risk *should*come* reward. Yep!

But as an option *seller*, I'm going to be VERY cautious -- I'm going to push out wings and shorten legs and be *really* picky about when I write. If I move (and I need to expect to!), I'm going to L.A.M.B. -- leave a man behind -- If I have 5 spreads on, I'll roll 4.5 of 'em, leaving a long behind. If vol is high enough, I'll look at calendars and diagonals. And finally, I'll take earlier/larger losses if it will reduce my (worst) exposures -- taking partial profits frees 100% of margin consumed, hey.

Not so much "stop playing" as playing with altogether different tactics.

eh eh eh.. Agreed.. different conditions call for different tactics. My question however was more about the playground than the game itself.. The responses I'm receiving are kind of comforting.

Here's how we handle this situation. We create a residual yield rate to line up the calls and puts. For BYND the residual rate is the market's implied borrow rate.

If I understand what you are saying

... the 'residual yield rate' forces the call-put vols to line up ... but is really just a number that can cover quite a lot of sins

This was really a discussion on whether put-call parity holds for dividend paying stocks with early exercise ... and not whether you can force vols to line up ... do you have similar analysis that shows p-c parity at each strike ?

Matt_ORATS

Sponsor

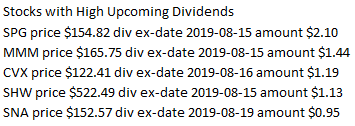

Okay, let's look a dividend paying stock. Here's a report we put out on high upcoming dividends.If I understand what you are saying

... the 'residual yield rate' forces the call-put vols to line up ... but is really just a number that can cover quite a lot of sins

This was really a discussion on whether put-call parity holds for dividend paying stocks with early exercise ... and not whether you can force vols to line up ... do you have similar analysis that shows p-c parity at each strike ?

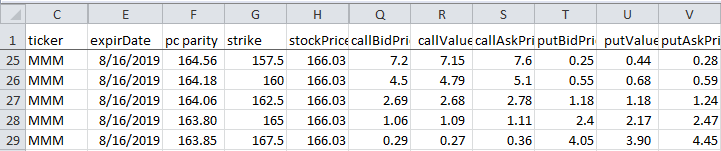

Let's look at MMM. That $1.44 dividend is going to play havoc with pc parity.

In column F, I put the formula, = strike + call mid - put mid bid-ask. So options are being priced off of the forward price of the stock less the dividend, or about $164.59 (stock price - dividend).

The calls are an exercise on 8/14/19 if the price of the put ex-div are < dividend.

The puts priced off of the $164.59 are all about a 44% volatility. The premium in the calls will vary depending on the probability of exercise.

It will be interesting to see where these prices go out tomorrow.

We seem to be dancing around the issue a little

... what has Ivol got to do with put-call parity ... except by showing there is a difference between call-put Vols ... you seem to be saying by definition that put-call parity does not hold for SPY

One final request for you to show the formula that reconciles put-call parity at say the 260 / 293 strikes

I clearly understood Robert explaining that even such out-of-whack stocks like BYND have put-call-parity, despite it not looking so. Therefore he wouldn’t have a reason to imply that SPY doesn’t hold put-call parity. And neither SPX or SPY are good examples because they perfectly hold put-call parity and there is nothing to see there.

Dividends also have nothing to do with this because they don’t change anything about put-call-parity. It is stocks that don’t have dividend and don’t seem to hold put-call parity that are best examples.

That’s why BYND was a great example because if you try to buy, for example, a 10 wide box, it costs more than $10. This is perfect example of where someone may try to sell such box for more than $10 thinking that they’re arbitraging lack of put-call parity, but they’d be wrong and would lose by missing that the seeming lack of put-call parity is caused by high short borrow %rates on BYND.

Okay, let's look a dividend paying stock. Here's a report we put out on high upcoming dividends.

Let's look at MMM.

That $1.44 dividend is going to play havoc with pc parity.

Thanks for all the analysis ... that's the point I have been trying to make

... that p-c parity does not hold for dividend paying stocks that can be exercised before expiry

Robert Morse

Sponsor

Thanks for all the analysis ... that's the point I have been trying to make

... that p-c parity does not hold for dividend paying stocks that can be exercised before expiry

In the BYND example, the question is if there is not P/C parity, how do you make free money? If you can't there is parity. Well, you can if you want to be long BYND. If you hold until expiration, long the ATM call and short the ATM put will provide a lower cost basis then long stock with less implied interest.

With regard to stocks with dividends, the ITM calls before X-date can provide a better return for being long stock, short the ITM call and long the OTM put if the call is not assigned and the put and carry is less than the dividend.

With regard to stocks with dividends, the ITM calls before X-date can provide a better return for being long stock, short the ITM call and long the OTM put if the call is not assigned and the put and carry is less than the dividend.

So you are effectively saying that put-call parity does not hold for stocks with dividends ...

Robert Morse

Sponsor

So you are effectively saying that put-call parity does not hold for stocks with dividends ...

You’re looking for absolutes, I am not going to give you that. The reality is that there’s no perfect price that fits everybody’s cost structure. Your long and short rate is completely different than a market maker. If you are long an ITM call and want to stay long and don’t care about a dime or don’t have BP to be long the stock, it makes sense not to exercise before a dividend while to someone else it’s a clean profit to be short that call vs the common.