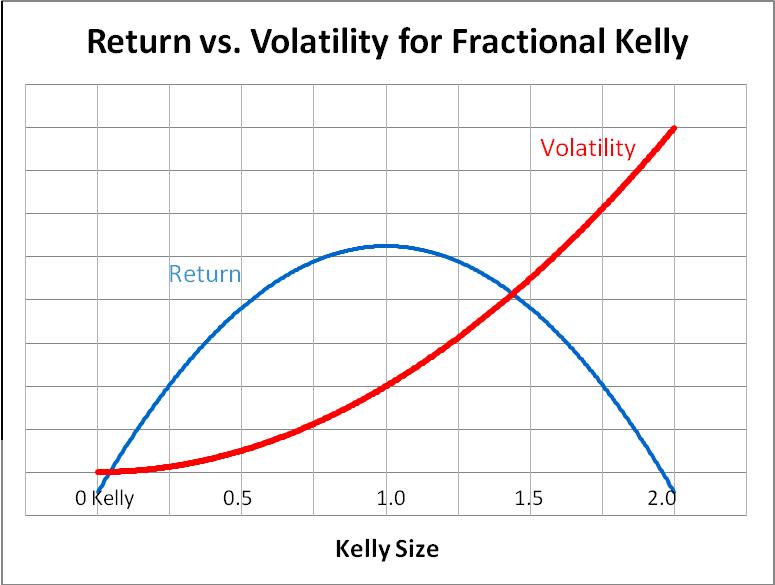

The general relationship between an increase in bet size and variance is if you double your bet size, the variance increases by a factor of root 2 and vice versa. Hope that helps in what you are looking for.

What's the formula from which this relationship is derived? And how does the growth rate scales when Kelly is reduced?

As Kelly is reduced, the growth rate decreases slower than the variance, which implies that the risk-adjusted growth (growth divided by variance) goes up. I'd like to know at which fraction of Kelly this risk-adjusted growth reaches its peak. I am guessing it would occur at somewhere around 1/4 of full Kelly.