Europeans aren't in debt like Americans (mortgage and cars are their primary debt) because rules regarding credit cards are strict.So what?? EVERYBODY is up to their neck in debt nowadays. Our houses are at least 75% financed by debt. Our purchases are 99% by credit card (why should they be in cash when I can enjoy one more month of interest by delaying my payment by one month?). Our tradings are all financed by margin loans. Without debt, you are not able to do anything nowadays. But somehow when it's America, it's because credit is handed out like "drugs to junkies". LOL

The issue is not with incurring debt; it's with how to manage one's debt properly. Like I said, you really don't know what you are talking about.

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Welcome to the 21st Century America!

- Thread starter VicBee

- Start date

(mortgage and cars are their primary debt)

Same here in America. Again, like I said, you don't know much.

because rules regarding credit cards are strict.

Being in debt is not the problem, not able to manage it is. You can have a whole closet of credit cards but if you manage your debt well, it's not a problem.

Last edited:

No, not "Same here in America". Credit card debt in America isn't mortgage or car payments which, most often, are not credit card purchases.Same here in America. Again, like I said, you don't know much.

Being in debt is not the problem, not able to manage it is. You can have a whole closet of credit cards but if you manage your debt well, it's not a problem.

Doing drugs isn't a problem is you learn to manage your habit. You can have a whole lotta variety in your closet but if you're careful, it's not a problem.

No, not "Same here in America". Credit card debt in America isn't mortgage or car payments which, most often, are not credit card purchases.

Doing drugs isn't a problem is you learn to manage your habit. You can have a whole lotta variety in your closet but if you're careful, it's not a problem.

Credit cards are not drugs. It's a noble and effective way to manage finance if managed right. You obviously don't know how to handle credit cards correctly. Seeing the amount of intelligence that's displayed in your troll posts, it's not difficult to see why.

Our purchases are 99% by credit card (why should they be in cash when I can enjoy one more month of interest by delaying my payment by one month?). Our tradings are all financed by margin loans. Without debt, you are not able to do anything nowadays.

These are no valid arguments. In Europe every tenth day of the month your credit card should be reset at zero, and till that reset, your total available credit amount cannot pass the monthly limit. So if the limit would be EUR 2,500 you can use that credit from the first day of the month till the tenth day of next month. But as you use that credit card the entire month, only the first few day you can enjoy of a month credit. The amount used during the rest of the month has a much shorter credit "advantage" as it dfeclines every time you pay with your credit card.

Second remark is: how much money can you save by using a credit card instead of cash payment?

If you buy for $ 2,000 food each month, you can "save" nothing as the cash that you don't use is on your normal bank account which does not give you any interest advantages. So there is no advantage.

I know people who use their credit card fully every month. These people are forced to do that as they digged a financial hole and have no money to live normally. Some of them even take two credit cards, with differnt banks and use one card to pay for the restet of the second card each motnh. In that way they can get over each reset without even paying anything. people without financial problems use rarely credit cards in Europe.

If the code of your bank card is stolen or hacked you have indeed a problem. But if the same happens with your credit card, the damage is much bigger as the limits on spending per transaction are higher then on a normal bank card.

Last edited:

This article shows clearly how horrible the situation can be in the US: https://www.cardrates.com/advice/average-credit-card-debt-by-country/

What?

Especially this part is shocking for Europeans to read:

5 Ways Americans Can Reduce What They Owe

Struggling to knock out your credit card debt? Here are some tips and tricks to pay down your balance while minimizing the interest owed.

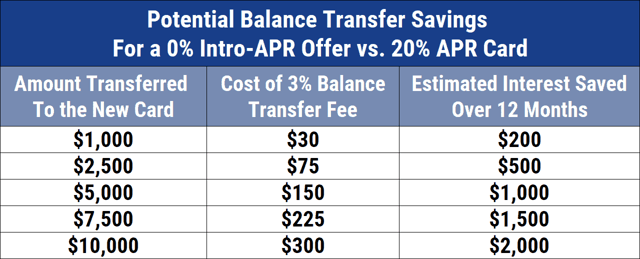

Apply For a Balance Transfer Card

High interest rates are one reason people struggle to pay off credit card debt. When you have a high interest rate, a large percentage of your payment will go toward the accrued interest — not the principal.

To maximize how much you’re paying toward the principal, you can apply for a new credit card with a 0% APR on balance transfers. These special offers only last for a limited period of time, usually between six and 21 months. During that time, interest will not accrue.

When you transfer an existing balance to a new card, you will likely have to pay a balance transfer fee. This fee is usually 3% or 5% of the amount transferred, depending on the card. For example, if you transfer $5,000, you could pay $150 to $250 in fees.

But here’s how much you could save by transferring your balance: Let’s say you qualify for a 0% APR offer for 18 months. You transfer a $5,000 balance from your card with 20% APR. If you can pay off the entire balance in 18 months, you would save $907 in interest charges.

If you have multiple balances on different cards, you may be able to transfer all of them onto your new card to help consolidate payment obligations, as long as the credit limit is high enough.

Request an Interest Rate Reduction

If you don’t qualify for a 0% APR balance transfer offer, you can still try to decrease your credit card interest rate by calling the credit card provider.

Make a list of all the credit cards you have with a current balance and divide them by provider. Next, take an afternoon to sit down and contact each company to ask them for a lower interest rate.

Take out a Debt Consolidation Loan

Sometimes you can get a lower interest rate with a debt consolidation loan than with a credit card. A debt consolidation loan is essentially a personal loan that is used to pay off existing debt, including credit cards.

Terms for debt consolidation loans usually range from 24 to 60 months, depending on the lender. These loans have fixed interest rates, while credit cards have variable interest rates. Monthly payments will stay the same for the entire term.

Interest rates for debt consolidation loans will vary depending on the loan amount, repayment term, and your personal credit score. The higher your score, the better rate you will receive. Also, longer terms will usually have higher rates, while shorter terms usually have lower rates.

Make sure to choose a term with monthly payments you’re comfortable making. If you choose a term with a high monthly payment and end up not being able to afford those payments, you’ll be in a worse position than if you had not consolidated at all.

Debt Relief Services

If your credit card debt is unmanageable and you’re considering bankruptcy, try using a debt relief service first. A qualified debt relief company can negotiate the terms of your debt directly with the lender or credit card provider.7

The debt relief company will then put you on its own payment plan that you must adhere to. Using a debt relief service can save you money, but there are some critical downsides.

A debt relief service should be your last resort because using one can negatively affect your credit score. And it may be unable to work with all your loan providers.

What?

- multiple balances on different cards

- take out a debt consolidation loan

- your credit card debt is unmanageable and you’re considering bankruptcy, try using a debt relief service first

Especially this part is shocking for Europeans to read:

5 Ways Americans Can Reduce What They Owe

Struggling to knock out your credit card debt? Here are some tips and tricks to pay down your balance while minimizing the interest owed.

Apply For a Balance Transfer Card

High interest rates are one reason people struggle to pay off credit card debt. When you have a high interest rate, a large percentage of your payment will go toward the accrued interest — not the principal.

To maximize how much you’re paying toward the principal, you can apply for a new credit card with a 0% APR on balance transfers. These special offers only last for a limited period of time, usually between six and 21 months. During that time, interest will not accrue.

When you transfer an existing balance to a new card, you will likely have to pay a balance transfer fee. This fee is usually 3% or 5% of the amount transferred, depending on the card. For example, if you transfer $5,000, you could pay $150 to $250 in fees.

But here’s how much you could save by transferring your balance: Let’s say you qualify for a 0% APR offer for 18 months. You transfer a $5,000 balance from your card with 20% APR. If you can pay off the entire balance in 18 months, you would save $907 in interest charges.

If you have multiple balances on different cards, you may be able to transfer all of them onto your new card to help consolidate payment obligations, as long as the credit limit is high enough.

Request an Interest Rate Reduction

If you don’t qualify for a 0% APR balance transfer offer, you can still try to decrease your credit card interest rate by calling the credit card provider.

Make a list of all the credit cards you have with a current balance and divide them by provider. Next, take an afternoon to sit down and contact each company to ask them for a lower interest rate.

Take out a Debt Consolidation Loan

Sometimes you can get a lower interest rate with a debt consolidation loan than with a credit card. A debt consolidation loan is essentially a personal loan that is used to pay off existing debt, including credit cards.

Terms for debt consolidation loans usually range from 24 to 60 months, depending on the lender. These loans have fixed interest rates, while credit cards have variable interest rates. Monthly payments will stay the same for the entire term.

Interest rates for debt consolidation loans will vary depending on the loan amount, repayment term, and your personal credit score. The higher your score, the better rate you will receive. Also, longer terms will usually have higher rates, while shorter terms usually have lower rates.

Make sure to choose a term with monthly payments you’re comfortable making. If you choose a term with a high monthly payment and end up not being able to afford those payments, you’ll be in a worse position than if you had not consolidated at all.

Debt Relief Services

If your credit card debt is unmanageable and you’re considering bankruptcy, try using a debt relief service first. A qualified debt relief company can negotiate the terms of your debt directly with the lender or credit card provider.7

The debt relief company will then put you on its own payment plan that you must adhere to. Using a debt relief service can save you money, but there are some critical downsides.

A debt relief service should be your last resort because using one can negatively affect your credit score. And it may be unable to work with all your loan providers.

Last edited:

Funny guy... Perhaps you can explain then why Europe keeps a strict control over bank issuing credit (not debit) cards?Credit cards are not drugs. It's a noble and effective way to manage finance if managed right. You obviously don't know how to handle credit cards correctly. Seeing the amount of intelligence that's displayed in your troll posts, it's not difficult to see why.

Fact, Americans have the world's highest credit card debt in the world, to the tune of $986 billion, the highest ever. Perhaps you manage your cards wisely, but evidently you're an outlier. Other fact, the entire US consumer economy is based on credit worthiness and every citizen is scored accordingly, a bit like China's good citizen score. Except in the US we like bad behavior, because a credit card holder who always pays their card charges on time is a bore to the lending industry. It wants minimum payments and will entice you with large credit lines to minimize the pain from that fist up your ass, funny guy.

Thank you.Perhaps you manage your cards wisely,

I am the norm. If you look at any statistics, bankrupcy due to credit card debt is still the very small minority.but evidently you're an outlier.

Fact, Americans have the world's highest credit card debt in the world, to the tune of $986 billion, the highest ever.

Doesn't mean they are not able to pay it off or worse bankrupt over it.

If you look at my credit cards before I pay them off, it amounts to a huge proportion of my income as well. But does it mean I am actually bankrupt over it? No.

So the amount of debt doesn't mean anything. You have to look at the ability to pay. Grow a brain and you might have a chance of understanding it.

Like youself I pay my creditcard balance in full every month. Good money management.So the amount of debt doesn't mean anything. You have to look at the ability to pay.

But I wonder how many would have to declare bankruptcy if they had to pay the full balance.

Look at the number of people who live paycheck to paycheck.

I am the norm. If you look at any statistics, bankrupcy due to credit card debt is still the very small minority.

This article contradicts what you say. You don't seem to be the norm.

Americans are not paying off their credit-card debt. We should be concerned.

https://www.morningstar.com/news/ma...their-credit-card-debt-we-should-be-concerned