Hey guys, I’ve been looking at basic options tables and reading about them, and I wanted to better understand the theory of how the market prices the options and what benefits are being traded.

Taking for example basic SPY calls; I was looking at June 2019 expirations, and if you buy an option right at the money, if the market was anywhere from negative to completely flat from here to expiration, you’d be at a 100% loss since the option is worthless at expiry.

Then, there would be some sort of partial loss for the range of 0% - 10%--because the premium paid would likely be greater than the (Expiry – Strike) value. A marginally positive return on the underlying still nets a loss because the option doesn’t just provide exposure; you’re also buying leverage, paying cost of carry, and especially buying the possibility of outsized returns if the market were to go further into a positive return.

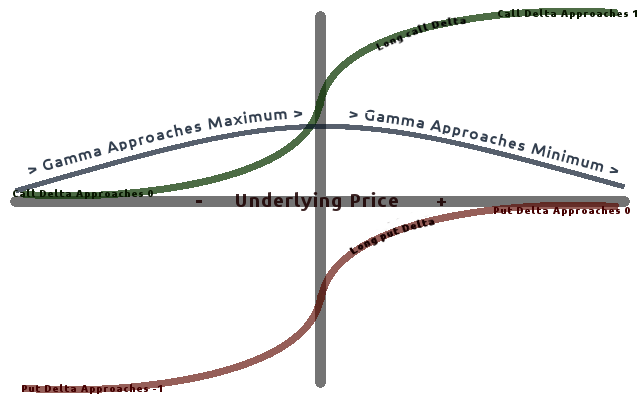

[That’s not because of delta, which decreases when you start to come out from deep ITM. This specific metric means the option value actually fluctuates less when the underlying moves at first because it may expire worthless. The potential of greater returns come from realized gamma? Or just a function of leverage? I’m probably the most fuzzy on understanding gamma.]

Tangent aside, I noticed once you get about ~30% ITM the call prices pretty much start to approach [Present Value – Strike]. This is because of increasing delta as the chance of the option expiring OTM becomes less and less. As delta approaches one, do things get simpler and we’re pretty much buying leveraged exposure to the underlying? Is there a premium priced into the value of deep ITM options for the benefit of having a fixed total loss and no direct cost of carry for a leveraged position, which is superior to a leveraged long?

In theory, what is the expected value of continually buying a single deep ITM call on the SPY year after year? Should it average out close to the returns of SPY itself? Or greater from the leverage yet with more volatility and the inability to compound because you can/will eventually hit a year where even 30% ITM expires worthless? Or less because you get net returns less the cost of benefits provided from the option?

Sorry if this is a bit of a ramble; trying to get my head around some conceptuals and would like to dive into this basic example of SPY calls to understand a few of these components intrinsic to options.

Taking for example basic SPY calls; I was looking at June 2019 expirations, and if you buy an option right at the money, if the market was anywhere from negative to completely flat from here to expiration, you’d be at a 100% loss since the option is worthless at expiry.

Then, there would be some sort of partial loss for the range of 0% - 10%--because the premium paid would likely be greater than the (Expiry – Strike) value. A marginally positive return on the underlying still nets a loss because the option doesn’t just provide exposure; you’re also buying leverage, paying cost of carry, and especially buying the possibility of outsized returns if the market were to go further into a positive return.

[That’s not because of delta, which decreases when you start to come out from deep ITM. This specific metric means the option value actually fluctuates less when the underlying moves at first because it may expire worthless. The potential of greater returns come from realized gamma? Or just a function of leverage? I’m probably the most fuzzy on understanding gamma.]

Tangent aside, I noticed once you get about ~30% ITM the call prices pretty much start to approach [Present Value – Strike]. This is because of increasing delta as the chance of the option expiring OTM becomes less and less. As delta approaches one, do things get simpler and we’re pretty much buying leveraged exposure to the underlying? Is there a premium priced into the value of deep ITM options for the benefit of having a fixed total loss and no direct cost of carry for a leveraged position, which is superior to a leveraged long?

In theory, what is the expected value of continually buying a single deep ITM call on the SPY year after year? Should it average out close to the returns of SPY itself? Or greater from the leverage yet with more volatility and the inability to compound because you can/will eventually hit a year where even 30% ITM expires worthless? Or less because you get net returns less the cost of benefits provided from the option?

Sorry if this is a bit of a ramble; trying to get my head around some conceptuals and would like to dive into this basic example of SPY calls to understand a few of these components intrinsic to options.