You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

"Tight spreads" (atm, itm, slightly otm) trading

- Thread starter conduit3030

- Start date

Sketchy trade of the month...CHK 12/15/2014

expiration: December 20

Bought the 18 sold the 16 put for ~400 debit.

See attached, executed around 10:30am EST

1. CHK is extremely weak, has pulled back more than it has in ~20 days since it gapped down originally.

Meh. See (2) below.

2. CHK RR vs probability structure indicates profitability.

Meh. I stand to gain $600 on $400 risked, 1.5:1 need to be right around 40% of the time. This is the tricky part. First, I'm basing this decision on the hourly chart rather than the daily as the price just hasn't pulled back in CHK, this is actualy its largest pullback (and if you look at the daily it's almost a nil retracement).

So it comes down to the probability vs RR. Short itnerest is high I'm sure right now, and a pop on CHK is very possible, let's put it around 40%. Should CHK rally, there's little hope for the trade because it's likely to burst and this spread is only 4 days out.

The odds still favor a trend continuation, because a trend is a trend, but as stated originally, it's a very sketchy trade.

Should CHK stay where it is (which seems unlikely) I'm out about $250-300, but again this seems unlikely. I see it popping or continuing down, not likely flat.

3. IV situation helps and hurts me.

Check. IV is getting very high, and I paid a premium to be in the trade. The problem is had I sold a credit spread otm, I'd get a lower RR and based on (2) above that's not acceptable in this upside-risky environment.

The good thing is high IV like this slightly favors more downside movement IMO, but I don't think that outweighs the extra cost.

4. Very little options-on-options rolling value here.

Check. Should CHK rally, it's probably not coming back for the next few weeks, at least as low as it currently is. This is disconcerting as I would usually roll 2 weeks further if the trade didn't work; I won't be able to do that on CHK.

5. The market is looking like it might tank this week.

Meh. After gapping up today and pushing into the red like it did, it certainly does look like it has some freefall potential. But it's just not enough of an edge. I have a 1.5:1 ratio on the spread, there's probaly a 30-40% chance of a tank this week, so they would seem to even out. But CHK has already dropped out a lot and there's no guarantee it tanks with the rest of the market for this reason.

Conclusion: (4) is probably the tipping factor in making this a net bad trade. I might take off tomorrow, not sure yet. (5) is also a bit disconcerting.

expiration: December 20

Bought the 18 sold the 16 put for ~400 debit.

See attached, executed around 10:30am EST

1. CHK is extremely weak, has pulled back more than it has in ~20 days since it gapped down originally.

Meh. See (2) below.

2. CHK RR vs probability structure indicates profitability.

Meh. I stand to gain $600 on $400 risked, 1.5:1 need to be right around 40% of the time. This is the tricky part. First, I'm basing this decision on the hourly chart rather than the daily as the price just hasn't pulled back in CHK, this is actualy its largest pullback (and if you look at the daily it's almost a nil retracement).

So it comes down to the probability vs RR. Short itnerest is high I'm sure right now, and a pop on CHK is very possible, let's put it around 40%. Should CHK rally, there's little hope for the trade because it's likely to burst and this spread is only 4 days out.

The odds still favor a trend continuation, because a trend is a trend, but as stated originally, it's a very sketchy trade.

Should CHK stay where it is (which seems unlikely) I'm out about $250-300, but again this seems unlikely. I see it popping or continuing down, not likely flat.

3. IV situation helps and hurts me.

Check. IV is getting very high, and I paid a premium to be in the trade. The problem is had I sold a credit spread otm, I'd get a lower RR and based on (2) above that's not acceptable in this upside-risky environment.

The good thing is high IV like this slightly favors more downside movement IMO, but I don't think that outweighs the extra cost.

4. Very little options-on-options rolling value here.

Check. Should CHK rally, it's probably not coming back for the next few weeks, at least as low as it currently is. This is disconcerting as I would usually roll 2 weeks further if the trade didn't work; I won't be able to do that on CHK.

5. The market is looking like it might tank this week.

Meh. After gapping up today and pushing into the red like it did, it certainly does look like it has some freefall potential. But it's just not enough of an edge. I have a 1.5:1 ratio on the spread, there's probaly a 30-40% chance of a tank this week, so they would seem to even out. But CHK has already dropped out a lot and there's no guarantee it tanks with the rest of the market for this reason.

Conclusion: (4) is probably the tipping factor in making this a net bad trade. I might take off tomorrow, not sure yet. (5) is also a bit disconcerting.

Attachments

Theoretical YHOO trade - 12/16/2014

Background: Someone I'm trading with came up with this idea.

YHOO is at 49.82 @ close. Assume it's around the same price on the open tomorrow.

See attached, we have two options, buy the 30-day spread or buy the 1-week spread (and roll the 1 week spread repeatedly, given our parameters are reached).

Choice 1:

Buy JAN 3 4x 48 calls, sell the 50 calls for $448, max gain of $352

Choice 2:

Buy DEC 3 4x 48 calls, sell the 50 calls for $546, max gain $254

Rationale for both:

1. YHOO is in a strong uptrend and has been consolidating for ~3 weeks. Should it start to break up, we may want to try a long. But we don't want to just buy calls, instead we want to spread for a cheaper cost and be ready to de-leg should our conviction go up.

Check. The question is which date do we choose to spread on?

2. This spread gives us huge options-on-options value.

Dec 3 vs. Jan 3 expirations:

1. Dec 3 gives a lower RR, Jan 3 a higher RR (about .5:1 vs. about .8:1, a pretty substantial difference.)

Note though that if we commit to auto-rolling the dec 3 spread at the end of the week, this RR really goes up. It's more like looking at .8:1 vs .8:1 when we consider that we MUST roll the the DEC spread, no matter what.

2. We believe that the move, should it come, is going to occur quickly over a short period of time.

This favors the short term options. Time decay gives us good value throughout the week and should YHOO start to take off in the next few days like we're hoping, we can easily deleg. Thus, within a few days we've covered the cost of the spread, whereas theta won't come close to doing that on the 30 day spread. This favors the short term spread

3. However, the detractor to the short term spread is we'll have to roll the long part of the delegged spread (the 48 calls) no matter what.

We're not looking to hold this for the 2-4 days remaining to expiration, this is for a bigger RR play. This is the tricky part, and I think favors the 30-day spread.

-------------

Any thoughts?

Background: Someone I'm trading with came up with this idea.

YHOO is at 49.82 @ close. Assume it's around the same price on the open tomorrow.

See attached, we have two options, buy the 30-day spread or buy the 1-week spread (and roll the 1 week spread repeatedly, given our parameters are reached).

Choice 1:

Buy JAN 3 4x 48 calls, sell the 50 calls for $448, max gain of $352

Choice 2:

Buy DEC 3 4x 48 calls, sell the 50 calls for $546, max gain $254

Rationale for both:

1. YHOO is in a strong uptrend and has been consolidating for ~3 weeks. Should it start to break up, we may want to try a long. But we don't want to just buy calls, instead we want to spread for a cheaper cost and be ready to de-leg should our conviction go up.

Check. The question is which date do we choose to spread on?

2. This spread gives us huge options-on-options value.

Dec 3 vs. Jan 3 expirations:

1. Dec 3 gives a lower RR, Jan 3 a higher RR (about .5:1 vs. about .8:1, a pretty substantial difference.)

Note though that if we commit to auto-rolling the dec 3 spread at the end of the week, this RR really goes up. It's more like looking at .8:1 vs .8:1 when we consider that we MUST roll the the DEC spread, no matter what.

2. We believe that the move, should it come, is going to occur quickly over a short period of time.

This favors the short term options. Time decay gives us good value throughout the week and should YHOO start to take off in the next few days like we're hoping, we can easily deleg. Thus, within a few days we've covered the cost of the spread, whereas theta won't come close to doing that on the 30 day spread. This favors the short term spread

3. However, the detractor to the short term spread is we'll have to roll the long part of the delegged spread (the 48 calls) no matter what.

We're not looking to hold this for the 2-4 days remaining to expiration, this is for a bigger RR play. This is the tricky part, and I think favors the 30-day spread.

-------------

Any thoughts?

Attachments

Theoretical YHOO trade - 12/16/2014

Background: Someone I'm trading with came up with this idea.

YHOO is at 49.82 @ close. Assume it's around the same price on the open tomorrow.

See attached, we have two options, buy the 30-day spread or buy the 1-week spread (and roll the 1 week spread repeatedly, given our parameters are reached).

Choice 1:

Buy JAN 3 4x 48 calls, sell the 50 calls for $448, max gain of $352

Choice 2:

Buy DEC 3 4x 48 calls, sell the 50 calls for $546, max gain $254

Rationale for both:

1. YHOO is in a strong uptrend and has been consolidating for ~3 weeks. Should it start to break up, we may want to try a long. But we don't want to just buy calls, instead we want to spread for a cheaper cost and be ready to de-leg should our conviction go up.

Check. The question is which date do we choose to spread on?

2. This spread gives us huge options-on-options value.

Dec 3 vs. Jan 3 expirations:

1. Dec 3 gives a lower RR, Jan 3 a higher RR (about .5:1 vs. about .8:1, a pretty substantial difference.)

Note though that if we commit to auto-rolling the dec 3 spread at the end of the week, this RR really goes up. It's more like looking at .8:1 vs .8:1 when we consider that we MUST roll the the DEC spread, no matter what.

2. We believe that the move, should it come, is going to occur quickly over a short period of time.

This favors the short term options. Time decay gives us good value throughout the week and should YHOO start to take off in the next few days like we're hoping, we can easily deleg. Thus, within a few days we've covered the cost of the spread, whereas theta won't come close to doing that on the 30 day spread. This favors the short term spread

3. However, the detractor to the short term spread is we'll have to roll the long part of the delegged spread (the 48 calls) no matter what.

We're not looking to hold this for the 2-4 days remaining to expiration, this is for a bigger RR play. This is the tricky part, and I think favors the 30-day spread.

-------------

Any thoughts?

If you think it's going to be a hard, fast move up why not put on a call backspread and leave yourself open to capture bigger upside?

Hey Longthewings,

A couple reasons, but note that I've not done back-spreads before so that's reason #1 lol

1. It's not a 60%, high RR trade (if those actually exist.) I used to do higher RR spreads in these scenarios but am trying to find something better.

2. Should the price not move up fast, we have good odds on the original debit-like credit spread. That trade alone might be marginally profitable

How about giving a detailed breakdown of how you'd trade the situation? I'd like to hear more detail in this regard.

A couple reasons, but note that I've not done back-spreads before so that's reason #1 lol

1. It's not a 60%, high RR trade (if those actually exist.) I used to do higher RR spreads in these scenarios but am trying to find something better.

2. Should the price not move up fast, we have good odds on the original debit-like credit spread. That trade alone might be marginally profitable

How about giving a detailed breakdown of how you'd trade the situation? I'd like to hear more detail in this regard.

Sell at the money calls and buy more OTM such that you're delta and vega neutral. As the stock moves around, buy or sell options in order to remain neutral atm, but long a lot of gamma in the right tail. You won't make or lose much if the stock sits still but if it pops up you'll quickly get long a lot of deltas.

Alright, here's the end of week update. Really quiet week for my account and now I literally have no positions, so most of this will focus on what to do next week.

1. Didn't roll CHK

Check. See attached. CHK had a burst to the upside and my option was to roll it 1-2 weeks out, it seemse like there's enough momentum that where iate currently stands (above 19.5) makes getting below the 18 strike less viable, and much moresoe the 16 strike. So agreed, don't gamble/roll.

2. Don't roll any of the TWTR calls.

Check. Originally I had planned to roll either the 40.5s or 43s a month out, but changd my mind over the course of the week. See attached; there just doesn't seem any indication TWTR is breaking this downtrend yet and I don't see any edge in rolling.

3. GG spread worked out pretty good, I got off 1 of the 2 outright puts when GG was around 17 on wednesday, GG then rallied a bit for the remainder of the week and I ended up making a decent amount when it finished around 18.5.

Overall, a pretty slow week for me as I was busy at work etc. but I do need to be putting on more risk than this week, just make sure not to force it.

--------------------------

Next week:

1. I think we're in a bit of limbo in the stock market and so no real bias to the upside or downside coming in. Last week's rally really surpised me given its being the strongest in a while. If you see the attached spy pic you'll see what I'm talking about. Notice that it reversed back up to the highs so abruptly, many new articles are saying it's bullish. I have no opinion on that yet.

2. I had expected less upside than what happened this week, or even expected downside some of the time. This was mostly based on the historical moves over the past 2-3 years we've consistently been seeing where the SPY drops out 5-8% before it has a sharp rally. So this threw me off a bit and probably was a factor in not putting on positions.

3. Next week I'm going to leave it open in terms of longs/shorts, but a few notes:

a. Don't focus on the higher RR debit spreads too much. I don't have a market directional conviction so focus on high IV credit spreads.

b. GG - gg worked out pretty good and given its IV level I might put on another spread early next week.

c. Again, be pretty liberal about the credit spreads but less so regaring higher RR (lower prob) trades.

--------------

Also, one more thing. I need to be less selective than I was this week. For instance, seeing the rally on thursday should have given me some confidence in putting on credit spreads to the upside that would expire next friday

1. Didn't roll CHK

Check. See attached. CHK had a burst to the upside and my option was to roll it 1-2 weeks out, it seemse like there's enough momentum that where iate currently stands (above 19.5) makes getting below the 18 strike less viable, and much moresoe the 16 strike. So agreed, don't gamble/roll.

2. Don't roll any of the TWTR calls.

Check. Originally I had planned to roll either the 40.5s or 43s a month out, but changd my mind over the course of the week. See attached; there just doesn't seem any indication TWTR is breaking this downtrend yet and I don't see any edge in rolling.

3. GG spread worked out pretty good, I got off 1 of the 2 outright puts when GG was around 17 on wednesday, GG then rallied a bit for the remainder of the week and I ended up making a decent amount when it finished around 18.5.

Overall, a pretty slow week for me as I was busy at work etc. but I do need to be putting on more risk than this week, just make sure not to force it.

--------------------------

Next week:

1. I think we're in a bit of limbo in the stock market and so no real bias to the upside or downside coming in. Last week's rally really surpised me given its being the strongest in a while. If you see the attached spy pic you'll see what I'm talking about. Notice that it reversed back up to the highs so abruptly, many new articles are saying it's bullish. I have no opinion on that yet.

2. I had expected less upside than what happened this week, or even expected downside some of the time. This was mostly based on the historical moves over the past 2-3 years we've consistently been seeing where the SPY drops out 5-8% before it has a sharp rally. So this threw me off a bit and probably was a factor in not putting on positions.

3. Next week I'm going to leave it open in terms of longs/shorts, but a few notes:

a. Don't focus on the higher RR debit spreads too much. I don't have a market directional conviction so focus on high IV credit spreads.

b. GG - gg worked out pretty good and given its IV level I might put on another spread early next week.

c. Again, be pretty liberal about the credit spreads but less so regaring higher RR (lower prob) trades.

--------------

Also, one more thing. I need to be less selective than I was this week. For instance, seeing the rally on thursday should have given me some confidence in putting on credit spreads to the upside that would expire next friday

Attachments

Hey,

Currently long Molycorp calls (which hasn't been going good and will discuss below the rationale, mistakes etc.) and am back under $2k in the account. Lol...so goes leverage I guess.

Anyways, I've been trading Nadex the last 6 months since the risk controls are much more versatile. I'd say the obvious number one lesson I've learned trading the Thinkorswim account is that I need to have better risk controls, and I think Nadex's smaller position sizing (for a small acount) takes advantage of that. Will discuss Nadex in a minute.

Currently long Molycorp calls (which hasn't been going good and will discuss below the rationale, mistakes etc.) and am back under $2k in the account. Lol...so goes leverage I guess.

Anyways, I've been trading Nadex the last 6 months since the risk controls are much more versatile. I'd say the obvious number one lesson I've learned trading the Thinkorswim account is that I need to have better risk controls, and I think Nadex's smaller position sizing (for a small acount) takes advantage of that. Will discuss Nadex in a minute.

Alright so essentially what I've noticed is people who trade exclusively technically, generally are not doing very well. It's also shown by the Hedge Fund Wizards books that the majority of macro traders are a mix of fundamental, technical, and sentiment. Meanwhile, if you go onto, say, forexfactory.com, people are constantly making threads about reading into weird candlestick patterns and other types of voodoo.

So what I'm doing on Nadex now is *trying* to mix fundamental asset correlations with trend-following techniques. I don't think looking at the last 30 candlesticks offers an edge, because there's little to no logic behind it. It's kind of like a modern version of practicing magic IMO...

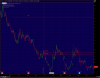

Anyways here's an overview of the rationale behind the MCP calls trades...see attached.

1. Molycorp is either going bankrupt or it's going to go into a recovery (as of 6 months ago, now it's clearly bankrupt). This means we should either be seeing a recovery in the share price, or about 0.

2. This *might* offer an asymmetrical payoff in the option pricing of MCP, if the IV doesn't account for it. My conclusion was that the IV wasn't accounting for the potential upside at the time...which I thought was about the $2 range in terms of a recovery. $1 Calls when the underlying was at 60c-80c we're roughly 20c...my breakeven was 1.20 and I planned to start taking some profits if it got above 2. That means I have to be right about 30% of the time on the trade, which I thought I was. Still kind of do actually...

3. The problem is I entered $1 calls when MCP = 80c, then added a substantial amount after it got above $1 a month or so later. This might be fine, too, but there was too much risk (about $2,500 of a 4.5k account) involved for a lower probability trade. I think the add when it got above $1 was standard, but it was too large an add (about $1,500 worth)...see attached photo.

So what I'm doing on Nadex now is *trying* to mix fundamental asset correlations with trend-following techniques. I don't think looking at the last 30 candlesticks offers an edge, because there's little to no logic behind it. It's kind of like a modern version of practicing magic IMO...

Anyways here's an overview of the rationale behind the MCP calls trades...see attached.

1. Molycorp is either going bankrupt or it's going to go into a recovery (as of 6 months ago, now it's clearly bankrupt). This means we should either be seeing a recovery in the share price, or about 0.

2. This *might* offer an asymmetrical payoff in the option pricing of MCP, if the IV doesn't account for it. My conclusion was that the IV wasn't accounting for the potential upside at the time...which I thought was about the $2 range in terms of a recovery. $1 Calls when the underlying was at 60c-80c we're roughly 20c...my breakeven was 1.20 and I planned to start taking some profits if it got above 2. That means I have to be right about 30% of the time on the trade, which I thought I was. Still kind of do actually...

3. The problem is I entered $1 calls when MCP = 80c, then added a substantial amount after it got above $1 a month or so later. This might be fine, too, but there was too much risk (about $2,500 of a 4.5k account) involved for a lower probability trade. I think the add when it got above $1 was standard, but it was too large an add (about $1,500 worth)...see attached photo.

Attachments

Here's an example of an intermarket correlation trade on Nadex:

7/27/2015 - 7:51 am - Long USDCAD expiry on 7/27 @ 3 pm

Rationale:

1. Crude oil has been tanking all night (and for the past several days/months)...clear trend down. USDCAD has a very strong negative correlation with Crude (Symbol /CL), one of the stronger market relationships. See the correlation coefficient in image 2, and the image of CL in in figure 1

2. USDCAD for the past day has been lagging behind CL. While crude is making new lows, USDCAD has been oscillating, not going anywhere. This looks like it might be a lagging relationship, with falling crude potentially leading USDCAD higher

3. So long USDCAD - I prefer a longer expiry than I took (7 am to 3 pm gives only 8 hours to catch up)...that was a mistake, should have given a longer expiry.

Result:

See image 3 - arrow 1 is the entry point long into USDCAD

1. Strike 1.304 - Slightly OTM, bought for $40 per spread with a max gain of $60, so I need to be right about 40% of the time on USDCAD ending above 1.304

2. USDCAD ends up @ ~1.303, below the strike, lose $40 per contract. (arrow 2)

7/27/2015 - 7:51 am - Long USDCAD expiry on 7/27 @ 3 pm

Rationale:

1. Crude oil has been tanking all night (and for the past several days/months)...clear trend down. USDCAD has a very strong negative correlation with Crude (Symbol /CL), one of the stronger market relationships. See the correlation coefficient in image 2, and the image of CL in in figure 1

2. USDCAD for the past day has been lagging behind CL. While crude is making new lows, USDCAD has been oscillating, not going anywhere. This looks like it might be a lagging relationship, with falling crude potentially leading USDCAD higher

3. So long USDCAD - I prefer a longer expiry than I took (7 am to 3 pm gives only 8 hours to catch up)...that was a mistake, should have given a longer expiry.

Result:

See image 3 - arrow 1 is the entry point long into USDCAD

1. Strike 1.304 - Slightly OTM, bought for $40 per spread with a max gain of $60, so I need to be right about 40% of the time on USDCAD ending above 1.304

2. USDCAD ends up @ ~1.303, below the strike, lose $40 per contract. (arrow 2)