The Truth Behind Broker Routing: Don't Believe The Hype

Traders Magazine Online News, June 7, 2017

John D'Antona Jr.

inShare

When we have asked most traders what their ideal liquidity seeking algorithm does, we usually hear something like “find the contra side of an order as quickly as possible, preferably without moving the price too much.” If a trader was working an order manually—that is, without using an algorithm, liquidity seeking would also be described in terms of urgency, but, a fairly typical answer for a non-urgent order would be, “check the blotter scrapers for naturals, then find active contras in dark pools, and finally clean up the order by crossing the spread and taking in lit markets.”

If buy-side traders were constructing liquidity seeking algorithms, this is how they would behave—and the best algorithms feel like an extension of a good trader’s thought process. Unfortunately, as many of us know (and a recent SEC fine confirmed), just because an algorithm should behave this way doesn’t mean that it will.

A Real-Life Example of Bad Routing

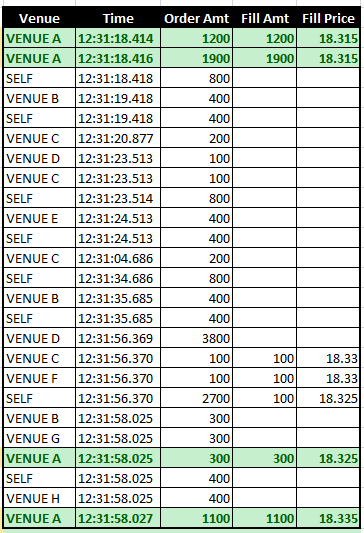

Here is client data that shows a broker's conflicted routing strategy.

In this example, 3,100 shares were executed in Venue A as a result of sending 1,200 shares (fully filled) and then 1,900 shares (fully filled) 2 milliseconds later.

The concerning part is that 19 routes to other venues took place before the algorithm went back to Venue A. Of these 19 routes, 7 were to the algorithm provider’s own venue, which resulted in only 100 shares executed.

Later in the routing sequence, even after getting full fills back at Venue A – the router still decides to go back and check their own pool and a new venue (Venue H).

All things being equal, executing in fewer places is preferable to executing in more places. Sources of liquidity should be tapped until they are dry, especially if that liquidity can be accessed without adverse price movements.

So clearly this type of routing should be a concern to all buy-side traders and requires analysis to uncover.

http://www.tradersmagazine.com/news...l?ET=tradersmagazine:e3048:1175783a:&st=email

Traders Magazine Online News, June 7, 2017

John D'Antona Jr.

inShare

When we have asked most traders what their ideal liquidity seeking algorithm does, we usually hear something like “find the contra side of an order as quickly as possible, preferably without moving the price too much.” If a trader was working an order manually—that is, without using an algorithm, liquidity seeking would also be described in terms of urgency, but, a fairly typical answer for a non-urgent order would be, “check the blotter scrapers for naturals, then find active contras in dark pools, and finally clean up the order by crossing the spread and taking in lit markets.”

If buy-side traders were constructing liquidity seeking algorithms, this is how they would behave—and the best algorithms feel like an extension of a good trader’s thought process. Unfortunately, as many of us know (and a recent SEC fine confirmed), just because an algorithm should behave this way doesn’t mean that it will.

A Real-Life Example of Bad Routing

Here is client data that shows a broker's conflicted routing strategy.

In this example, 3,100 shares were executed in Venue A as a result of sending 1,200 shares (fully filled) and then 1,900 shares (fully filled) 2 milliseconds later.

The concerning part is that 19 routes to other venues took place before the algorithm went back to Venue A. Of these 19 routes, 7 were to the algorithm provider’s own venue, which resulted in only 100 shares executed.

Later in the routing sequence, even after getting full fills back at Venue A – the router still decides to go back and check their own pool and a new venue (Venue H).

All things being equal, executing in fewer places is preferable to executing in more places. Sources of liquidity should be tapped until they are dry, especially if that liquidity can be accessed without adverse price movements.

So clearly this type of routing should be a concern to all buy-side traders and requires analysis to uncover.

http://www.tradersmagazine.com/news...l?ET=tradersmagazine:e3048:1175783a:&st=email