The fact that I'm a bit bullish on the dollar and in gold at the same time can be summed in this argument 'Gold will outperform the other members of the DX over the course of this cycle'. At least thats my bet, if it goes down it will come back faster/go down less then say EUR/JPY or other DX members and so on as the devaluation fear bid keeps supporting the metal

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

The Credit Crisis Financial Stocks Short Journal

- Thread starter Daal

- Start date

Geithner is a former FOMC member and now just made a move to increase the monetary base by $200b

http://www.google.com/hostednews/ap/article/ALeqM5h1yFbpRakAxYLao_y6lSl6x0nOSAD9AODCR80

This program worked as follows, the treasury would issue bills, take the cash deposit at the Fed. Effectively removing cash(monetary base) from the system. As the bill matures and Tres doesnt roll over, cash will be going from Geithner's checking account at the Fed to the treasury bill holders at maturity, that cash will officially become money base(Geithner's account is not counted as bank reserves as far as I know). I would SHOCKED if Geithner didnt talk with Bernanke before doing this, they are buddies, and this is a monetary policy move as well as fiscal. This is effectively the same as the Fed announcing more $200b in purchases, this means Bernanke is still dovish here as he would strongly advise against this if he thought it was time to get out

This rumor of fed hike and bond sell off is just that, a rumor

http://www.google.com/hostednews/ap/article/ALeqM5h1yFbpRakAxYLao_y6lSl6x0nOSAD9AODCR80

This program worked as follows, the treasury would issue bills, take the cash deposit at the Fed. Effectively removing cash(monetary base) from the system. As the bill matures and Tres doesnt roll over, cash will be going from Geithner's checking account at the Fed to the treasury bill holders at maturity, that cash will officially become money base(Geithner's account is not counted as bank reserves as far as I know). I would SHOCKED if Geithner didnt talk with Bernanke before doing this, they are buddies, and this is a monetary policy move as well as fiscal. This is effectively the same as the Fed announcing more $200b in purchases, this means Bernanke is still dovish here as he would strongly advise against this if he thought it was time to get out

This rumor of fed hike and bond sell off is just that, a rumor

Quote from ralph00:

Treasury market has been doing well also.

This is making me confident the equity market is wrong. We are seeing all this better than expected data all over the place and yet USTs have been trending up since June, short term rates futures have been on a nice rally since May and barely went down as equities soared to new highs. Yesterday people bought stocks as if the NYSE were going into closed for a year yet UST barely sold off

The smart money is also skeptical, Whitney Tilson says the home price rise is seasonal and prices are headed to new lows says is hedging longs and shorting financials('playing defense'), yet Greenspan was cheerleading the price rise as if housing bottomed, then said if it went down again the economy would have another downturn

Treasuries did ok, but it was a nasty day in E$ futures yesterday.

Reminds me of the action in Japan a bit. For a time, JGBs traded at an inverse correlation in stocks. Then, occassionally stocks would rally, but JGBs wouldn't sell off. Eventually it came to pass, and folks came to realize that the rally in stocks was just a bounce off the continuing secular bear market - therefore no reason for bond yields to rise just because stocks were having a nice run.

Reminds me of the action in Japan a bit. For a time, JGBs traded at an inverse correlation in stocks. Then, occassionally stocks would rally, but JGBs wouldn't sell off. Eventually it came to pass, and folks came to realize that the rally in stocks was just a bounce off the continuing secular bear market - therefore no reason for bond yields to rise just because stocks were having a nice run.

One stock that I'm long, the chinese company ACTS is flying right now, and I have no idea why(there is no news), about frigging time I benefit from the equity insanity

I bought because the company had more cash and marketable securities(Bank CDs) than the entire market cap, there was no pending lawsuit or debt coming due and the company was losing very little money, a chunk of the revenue was derived from interest income from the cash pile. So it was a simply arb that the market cap would go up to the level of the cash at least, the gap is closing(they got $3 a share in cash) but I cant seem to figure out why now

I bought because the company had more cash and marketable securities(Bank CDs) than the entire market cap, there was no pending lawsuit or debt coming due and the company was losing very little money, a chunk of the revenue was derived from interest income from the cash pile. So it was a simply arb that the market cap would go up to the level of the cash at least, the gap is closing(they got $3 a share in cash) but I cant seem to figure out why now

Looks like Geithner still havent implemented his own QE

http://www.federalreserve.gov/releases/h41/Current/

His checking accounts still havent moved much

U.S. Treasury, general Account 25,346

U.S. Treasury, supplementary financing account 199,932

The general account actually increased $8b, this might be just the liquidity management account of the Treasury

The supplementary is where he will do his QE and dump $200b more in bank reserves in the system as he winds down the SFP, we will see when this happens

http://www.federalreserve.gov/releases/h41/Current/

His checking accounts still havent moved much

U.S. Treasury, general Account 25,346

U.S. Treasury, supplementary financing account 199,932

The general account actually increased $8b, this might be just the liquidity management account of the Treasury

The supplementary is where he will do his QE and dump $200b more in bank reserves in the system as he winds down the SFP, we will see when this happens

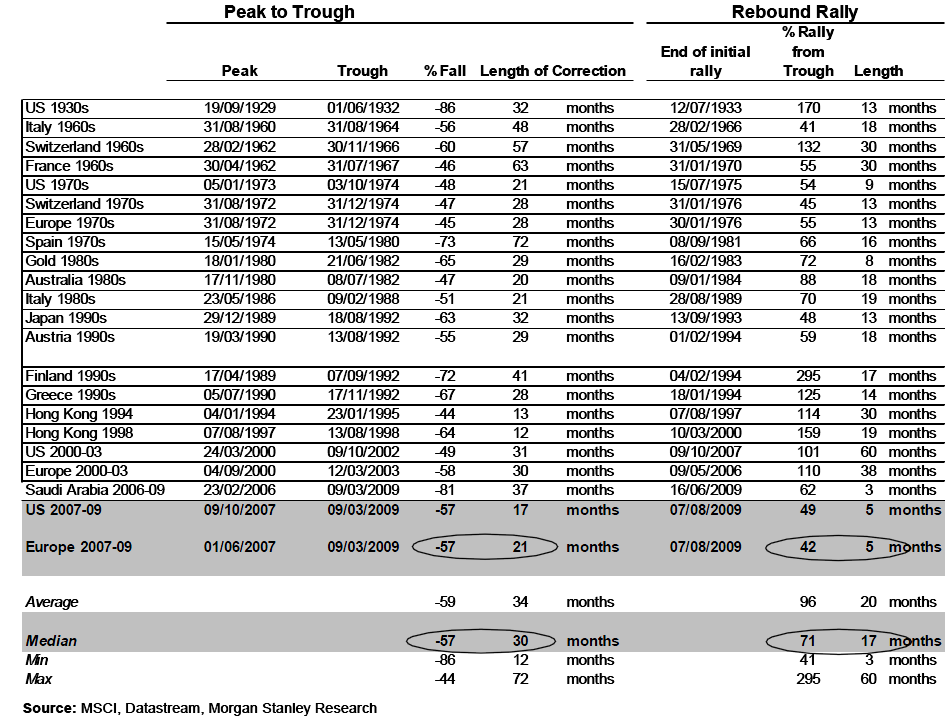

Maybe it was a mistake on my part in looking at this rally in a US historical context only. Perhaps I should have looked in a global scale

Cant help but to notice that the rallies in the 70's were far weaker and shorter than the ones in the 90's

PE ratios were expanding then(90's) and now we are in a secular bear. That makes me think even though the median is a 71% move in 17 months, the rally is already getting extended and due to end unless a 90's type period is about to start

Furthermore the betas of the countries in the sample are higher as they were riskier(like HK in 98), so this distorts the number a bit if you use it to forecast US equities

Cant help but to notice that the rallies in the 70's were far weaker and shorter than the ones in the 90's

PE ratios were expanding then(90's) and now we are in a secular bear. That makes me think even though the median is a 71% move in 17 months, the rally is already getting extended and due to end unless a 90's type period is about to start

Furthermore the betas of the countries in the sample are higher as they were riskier(like HK in 98), so this distorts the number a bit if you use it to forecast US equities

Jim Grant w/a nice piece in today's WSJ ...If he's right, you won't want to be long euro$'s of any sort. In a more comforting vein, Jim 'bozo' Cramer is now very publicly and very strongly bearish on US treasuries.

http://online.wsj.com/article/SB100...475582956.html#mod=WSJ_hpp_sections_lifestyle

As if they really knew, leading economists predict that recovery from our Great Recession will be plodding, gray and jobless. But they don't know, and can't. The future is unfathomable.

Not famously a glass half-full kind of fellow, I am about to propose that the recovery will be a bit of a barn burner. Not that I can really know, either, the future being what it is. However, though I can't predict, I can guess. No, not "guess." Let us say infer.

The very best investors don't even try to forecast the future. Rather, they seize such opportunities as the present affords them. Henry Singleton, chief executive officer of Teledyne Inc. from the 1960s through the 1980s, was one of these enlightened opportunists. The best plan, he believed, was no plan. Better to approach an uncertain world with an open mind. "I know a lot of people have very strong and definite plans that they've worked out on all kinds of things," Singleton once remarked at a Teledyne annual meeting, "but we're subject to a tremendous number of outside influences and the vast majority of them cannot be predicted. So my idea is to stay flexible." Then how many influences, outside and inside, must bear on the U.S. economy?

Though we can't see into the future, we can observe how people are preparing to meet it. Depleted inventories, bloated jobless rolls and rock-bottom interest rates suggest that people are preparing for to meet it from the inside of a bomb shelter.

The Great Recession destroyed confidence as much as it did jobs and wealth. Here was a slump out of central casting. From the peak, inflation-adjusted gross domestic product has fallen by 3.9%. The meek and mild downturns of 1990-91 and 2001 (each, coincidentally, just eight months long, hardly worth the bother), brought losses to the real GDP of just 1.4% and 0.3%, respectively. The recession that sunk its hooks into the U.S. economy in the fourth quarter of 2007 has set unwanted records in such vital statistical categories as manufacturing and trade inventories (the steepest decline since 1949), capacity utilization (lowest since at least 1967) and industrial production (sharpest fall since 1946).

It isn't just every postwar disturbance that sends Citigroup Inc. (founded in 1812) into the arms of the state or has General Electric Co. (triple-A rated from 1956 to just this past March) borrowing under the wing of the Federal Deposit Insurance Corp. Neither does every recession feature zero percent Treasury bill yields, a coast-to-coast bear market in residential real estate or a Federal Reserve balance sheet beginning to resemble that of the Reserve Bank of Zimbabwe. Yet these things have come to pass.

Americans are blessedly out of practice at bearing up under economic adversity. Individuals take their knocks, always, as do companies and communities. But it has been a generation since a business cycle downturn exacted the collective pain that this one has done. Knocked for a loop, we forget a truism. With regard to the recession that precedes the recovery, worse is subsequently better. The deeper the slump, the zippier the recovery. To quote a dissenter from the forecasting consensus, Michael T. Darda, chief economist of MKM Partners, Greenwich, Conn.: "[T]he most important determinant of the strength of an economy recovery is the depth of the downturn that preceded it. There are no exceptions to this rule, including the 1929-1939 period."

Click the link for the whole article.

http://online.wsj.com/article/SB100...475582956.html#mod=WSJ_hpp_sections_lifestyle

As if they really knew, leading economists predict that recovery from our Great Recession will be plodding, gray and jobless. But they don't know, and can't. The future is unfathomable.

Not famously a glass half-full kind of fellow, I am about to propose that the recovery will be a bit of a barn burner. Not that I can really know, either, the future being what it is. However, though I can't predict, I can guess. No, not "guess." Let us say infer.

The very best investors don't even try to forecast the future. Rather, they seize such opportunities as the present affords them. Henry Singleton, chief executive officer of Teledyne Inc. from the 1960s through the 1980s, was one of these enlightened opportunists. The best plan, he believed, was no plan. Better to approach an uncertain world with an open mind. "I know a lot of people have very strong and definite plans that they've worked out on all kinds of things," Singleton once remarked at a Teledyne annual meeting, "but we're subject to a tremendous number of outside influences and the vast majority of them cannot be predicted. So my idea is to stay flexible." Then how many influences, outside and inside, must bear on the U.S. economy?

Though we can't see into the future, we can observe how people are preparing to meet it. Depleted inventories, bloated jobless rolls and rock-bottom interest rates suggest that people are preparing for to meet it from the inside of a bomb shelter.

The Great Recession destroyed confidence as much as it did jobs and wealth. Here was a slump out of central casting. From the peak, inflation-adjusted gross domestic product has fallen by 3.9%. The meek and mild downturns of 1990-91 and 2001 (each, coincidentally, just eight months long, hardly worth the bother), brought losses to the real GDP of just 1.4% and 0.3%, respectively. The recession that sunk its hooks into the U.S. economy in the fourth quarter of 2007 has set unwanted records in such vital statistical categories as manufacturing and trade inventories (the steepest decline since 1949), capacity utilization (lowest since at least 1967) and industrial production (sharpest fall since 1946).

It isn't just every postwar disturbance that sends Citigroup Inc. (founded in 1812) into the arms of the state or has General Electric Co. (triple-A rated from 1956 to just this past March) borrowing under the wing of the Federal Deposit Insurance Corp. Neither does every recession feature zero percent Treasury bill yields, a coast-to-coast bear market in residential real estate or a Federal Reserve balance sheet beginning to resemble that of the Reserve Bank of Zimbabwe. Yet these things have come to pass.

Americans are blessedly out of practice at bearing up under economic adversity. Individuals take their knocks, always, as do companies and communities. But it has been a generation since a business cycle downturn exacted the collective pain that this one has done. Knocked for a loop, we forget a truism. With regard to the recession that precedes the recovery, worse is subsequently better. The deeper the slump, the zippier the recovery. To quote a dissenter from the forecasting consensus, Michael T. Darda, chief economist of MKM Partners, Greenwich, Conn.: "[T]he most important determinant of the strength of an economy recovery is the depth of the downturn that preceded it. There are no exceptions to this rule, including the 1929-1939 period."

Click the link for the whole article.

Quote from ralph00:

Jim Grant w/a nice piece in today's WSJ ...If he's right, you won't want to be long euro$'s of any sort.

I remember Grant talking in 07 how the fed cuts were hurting savers to save people who made mistakes. I will take 4-1 odds that Grant is wrong in monetary policy any day and twice on holidays

Furthermore his 'sharp rebounds always follow sharp corrections' is totally contradicted by both the IMFs study of financial crisis(2% growth in the first year of recovery) and the Rogoff sample(which shows recoveries take a long time), he is looking at the US only.

Even in the case of US only GDP growth is not that big of a deal for fed policy, its GDP growth ex-government that matters. You wont see the FOMC hiking rates in government induced GDP booms because they know that as soon they cut back the economy is back on recession(What I dubbed 1937 paranoia)

But here is the argument that will shred any Grant bs hawkish sentiment to pieces, the discount rate(the 30's version of the fed funds rate as the Fed used that to manipulate IR instead of FF) was at 2.5% in 1933, it finished 1938 at 1%!(Source: A Monetary History of the United States), only cuts happened in that period. CPI inflation was also contained(apart from the period right after FDR devalued the dollar), although PPI inflation was quite high

Heres more grant counterarguments

http://economistsview.typepad.com/timduy/