I suggest you look at my graphs again or reference your numbers.Umm no.

-54.641% (TSLA) is more than {not good}

-52.241% (F) and

-49.437% (GM)

or Tesla is still down more than Ford and GM is down the least.

Even with TSLA coming back the most of the three, percentwise, off their respective lows.

That is the reality.

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Tesla 2023

- Thread starter VicBee

- Start date

Appreciate itI suggest you look at my graphs again or reference your numbers.

") but I don't need to.

but I don't need to.As my chart pic clearly shows TSLA had the biggest drop, the biggest (so far) retracement back up but is still don't the most - percentagewise.

+ + +

Sidenote: you can't be happy with Musk pivoting to DeSantis. Yea yea keep it on Tesla. Haha

Meanwhile Elon rips Biden for union support but gladly accepts buyers tax subsidies that Reps would kill pronto if they had the votes.

I shall stick to my data then and agree to disagree. But we're disagreeing on tiny % and I just don't know how F or GM are going to raise their stock value.Appreciate it

As my chart pic clearly shows TSLA had the biggest drop, the biggest (so far) retracement back up but is still don't the most - percentagewise.

+ + +

Sidenote: you can't be happy with Musk pivoting to DeSantis. Yea yea keep it on Tesla. Haha

Meanwhile Elon rips Biden for union support but gladly accepts buyers tax subsidies that Reps would kill pronto if they had the votes.

On the side note, no I don't like Musk meddling openly in politics for its impact on the Tesla brand, which has taken as serious hit last year.

Musk has frequently said he would rather there were no subsidies but if there are, Tesla should also get them. Subsidies distort markets, something traditional energy companies and auto manufacturers have benefited from since their beginnings.

I've said before, unions are a plague, a mafia headed by the Democrat party. The only thing Trump did right was to break their stranglehold by turning white union members in mixed race union shops into Trumpists. It's the only reason Trump still manages to have such high support. A further light on America's underbelly of shame.

I thought I'd put my neck out and post this Seeking Alpha article -well known Tesla bears- as the basis to challenge their and other negative spin about the future of Tesla and its share price. I edited the article for clarity but link is there for reference.

I also decided to leave in the writer's background, for fun.

For context, TSLA today closed at 184, so the author's 188 price rating is essentially a bearish assessment of the company.

After reading this article, I maintain a high of 300 in 2023.

https://seekingalpha.com/article/4607026-tesla-stock-pumped-and-warned-by-elon-musk?

Ahan Vashi

Investing Group LeaderThe Quantamental Investor

Summary

A new wave of investor optimism seems to be pushing Tesla, Inc. (NASDAQ:TSLA) stock higher in the aftermath of its shareholder meeting (held on 16th May 2023), wherein CEO Elon Musk highlighted Tesla's long-term business prospects in emerging areas such as autonomous driving [FSD] and robotics [Optimus].

GoogleFinance

In late-2022/early-2023, I was incredibly bullish on Tesla in the mid to low $100s, at a time when Mr. Market was selling it off like a drunken psycho on a daily basis. After having accumulated Tesla for several months in the mid to low $100s, we sold half of our Tesla position at ~$194 a few weeks ago as the wild rally in TSLA took a pause at a key technical level at ~$200-215.

While market participants are clearly getting excited about Tesla once again, I am sticking to a "Neutral" rating for TSLA after having shifted my stance in light of Tesla's Q1 earnings back in April. If you have been following my work on Tesla, you know that my rationale for the downgrade was based on greater macroeconomic uncertainties, dangers of Tesla's recession playbook [making it a binary bet on FSD], and ominous technical setup. Find a more detailed explanation here:

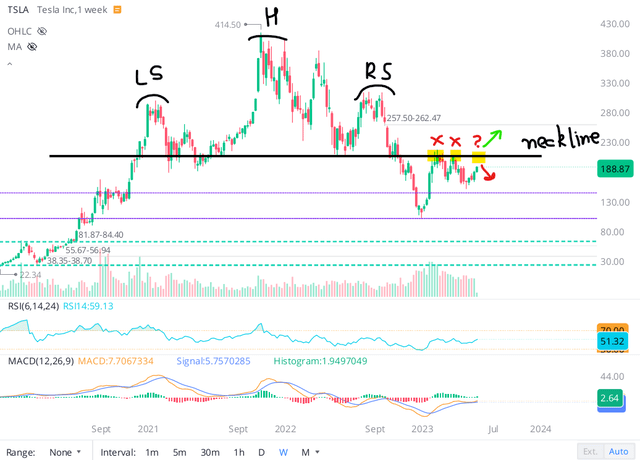

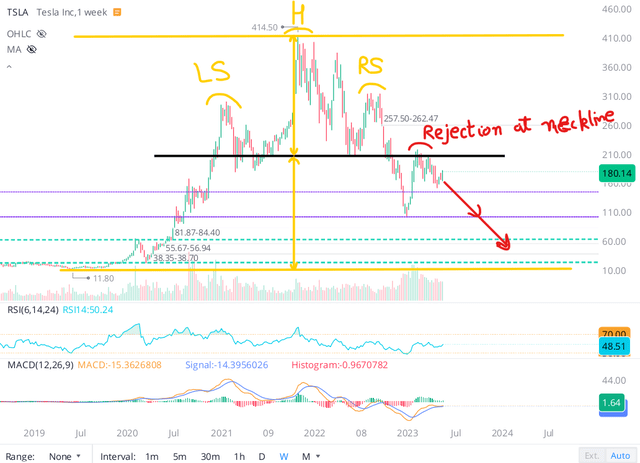

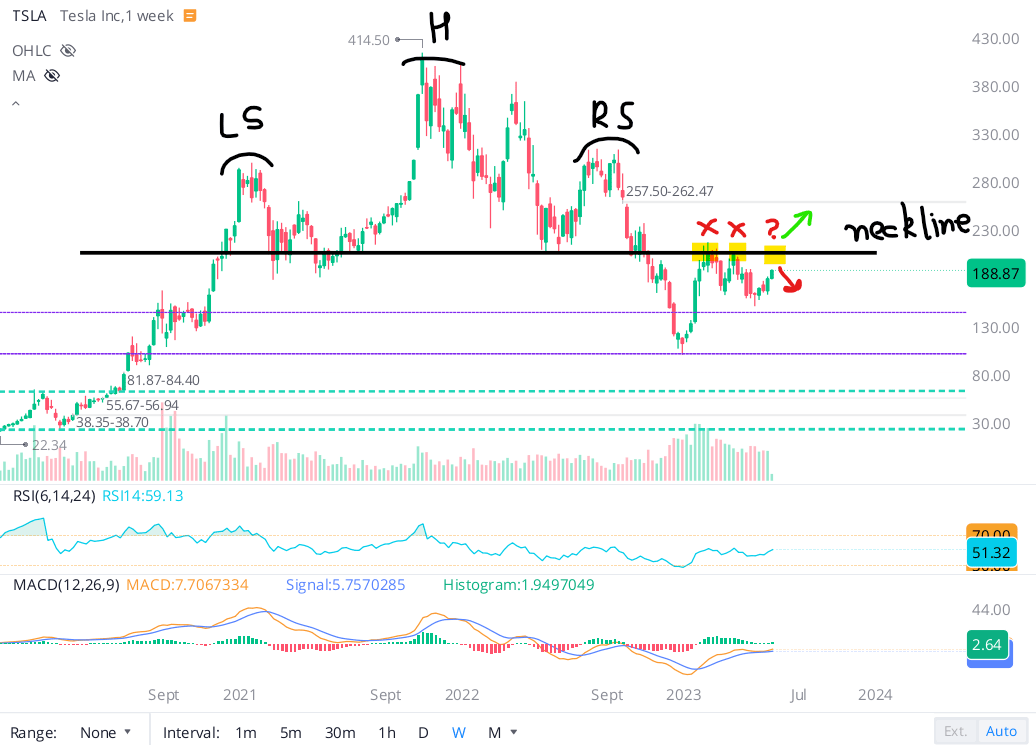

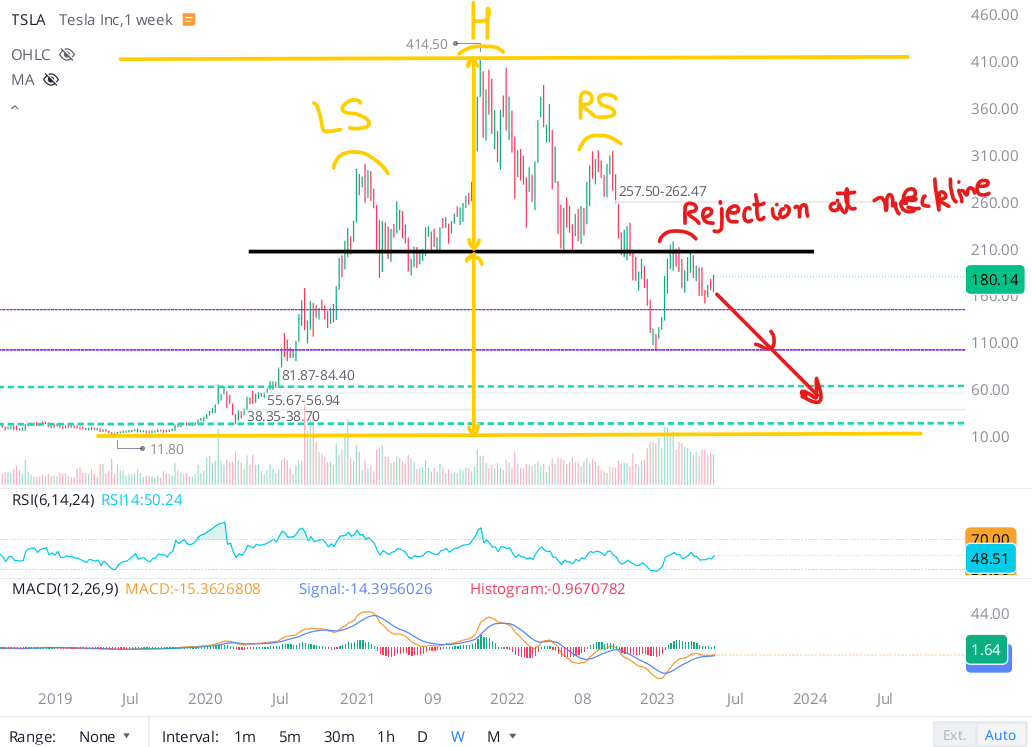

Despite Elon Musk's dire warnings on the economy, investors have been piling into TSLA stock, which apparently looks set to re-test the neckline of its head and shoulders pattern. As you can observe in the chart below, Tesla's stock has already been rejected twice at this key technical level. If Tesla fails to break past this area of resistance, technically, the stock could be headed back down to the mid $100s [and even to the low $100s] in a continuation of the reverse gamma squeeze we saw in late-2022.

WeBull Desktop

In this note, we will discuss major takeaways from Tesla's Annual Shareholder Meeting. And then check up on TSLA's ominous-looking technical chart.

Highlights Of Tesla 2023 Shareholder Meeting

Keeping in tradition with past investor events, Tesla's 2023 Annual Shareholder Meeting and Musk's subsequent CNBC interview (with David Faber) were filled with lots of hyperbolic statements such as "FSD could be the ChatGPT moment for Tesla" and "Demand for Tesla's Optimus Humanoid Bot could be 10 billion units."

Here's a list of noteworthy announcements from the meeting:

Now, let's discuss Tesla's business outlook in light of its shareholder meeting.

What Is The Long-Term Business Outlook?

While Musk stoked the hype engine quite a bit with positive commentary on ambitious projects such as FSD, Cybertruck, Optimus humanoid bot, and two new EV vehicle models (likely a compact car and a Van), none of these are likely to move the needle for Tesla in the near-term.

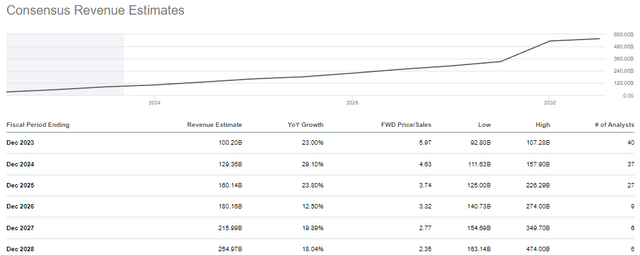

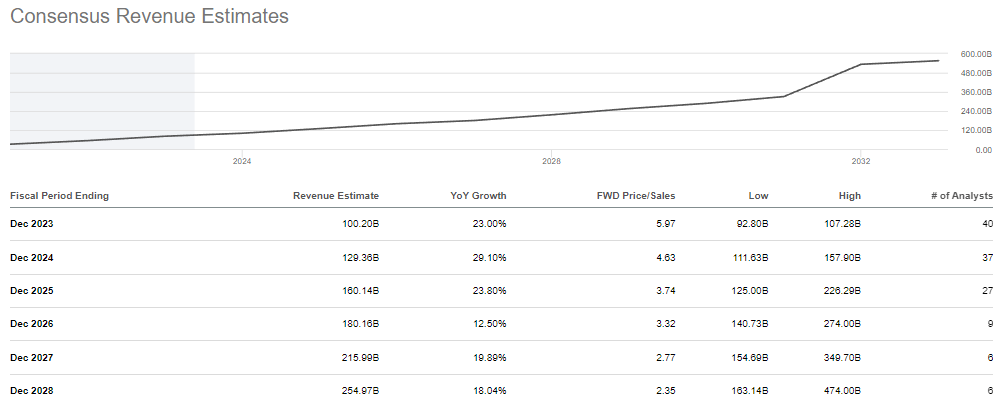

That said, Tesla's recession playbook is still expected to result in volume growth during 2023. According to consensus street estimates (and Musk), Tesla is likely to do $100B in revenue this year.

SeekingAlpha

Going forward, consensus analyst estimates peg CAGR sales growth to be in the low-to-mid-20s, which is a far cry from where Tesla's growth has been over the past decade. Given Tesla's scale, I think a slowdown is natural; however, a growth slowdown raises question marks over TSLA's valuation premium. Now, bulls like to value Tesla as a high-margin software company, whereas bears prefer a valuation more in line with other automakers.

Personally, I think the reality is somewhere in between. As I said in my previous note, Tesla is turning into a binary bet on FSD. According to Musk, FSD could boost Tesla's gross margins to ~80%. While I am skeptical about that figure, I think that if FSD achieves full autonomy, Tesla can deliver software-like margins. In this scenario, Tesla would deserve a multiple similar to an Apple Inc. (AAPL) (~25-30x earnings) and not a Ford Motor Company (F) (~5-10x earnings).

Will Tesla FSD reach full autonomy in 2023 or 2024? I don't know. While the likes of Cathie Wood (and many Tesla bulls) think it could happen this year, the jury is still out there. As an investor, I prefer to wait for evidence before trying to model something like FSD into my valuation estimate for the company. And so, I am not altering my model based on Musk's positive FSD commentary from the annual shareholder meeting.

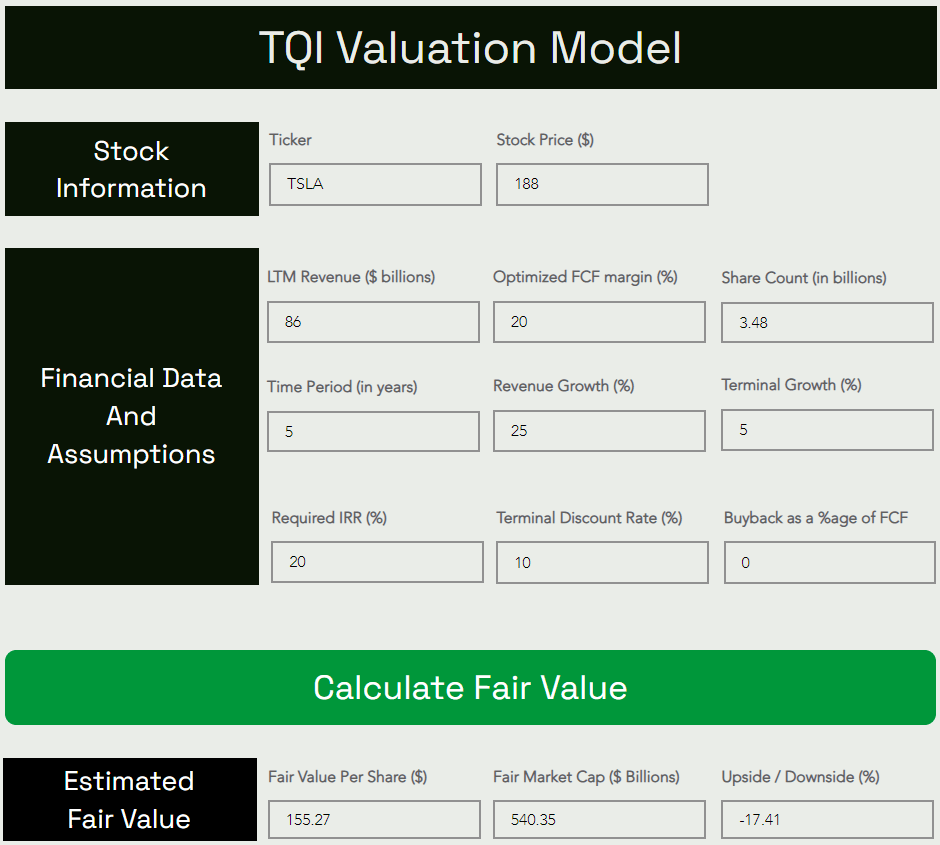

TQI's Valuation Model For Tesla

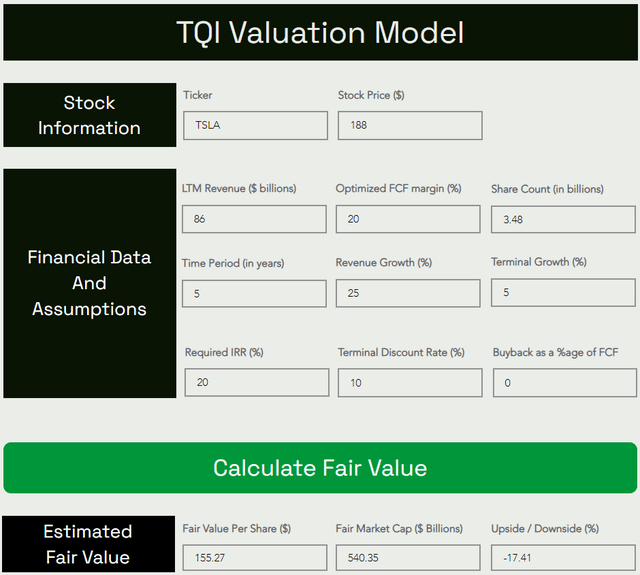

With Q1 results coming (more or less) in line with expectations, I am sticking to most of my pre-earnings assumptions for Tesla. However, in order to factor in the added risk of Tesla turning into a binary bet on FSD due to Musk's recession playbook, I raised our model's "Required IRR" from 15% to 20%.

Also, Tesla's recession playbook is killing its free cash flow ("FCF") generation, and in the interest of improving the margin of safety in our model, I reduced the "Buyback as a % of FCF" (capital return program) assumption from 25% to 0%.

Here's my updated valuation for Tesla:

TQI Valuation Model (TQIG.org)

According to these results, Tesla's fair value is ~$155 per share. With the stock trading at $188 per share, it is currently overvalued by ~17.5%. Now, I am happy to pay a premium for a high-quality company like Tesla; however, is the risk/reward attractive enough to justify an investment at current levels?

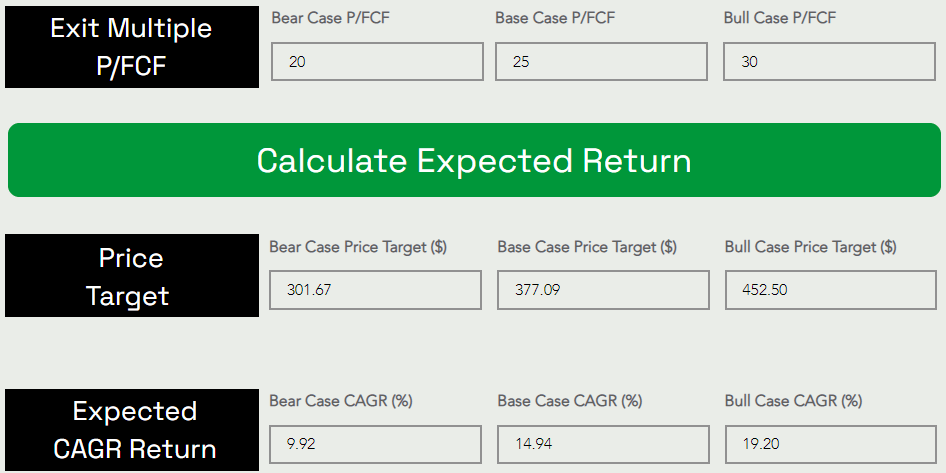

TQI Valuation Model (TQIG.org)

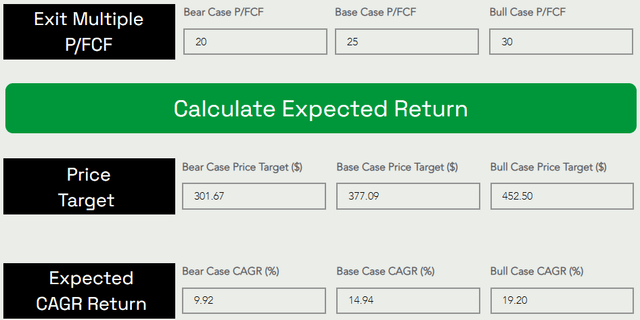

Assuming a base case P/FCF exit multiple of 25x, I see Tesla hitting $377 per share by 2027. As can be seen below, Tesla is projected to deliver CAGR returns of 14.94% for the next five years, which more or less meets my investment hurdle rate of 15%.

However, the valuation is not exciting enough to justify a long position by itself, as was the case in late-2022 when Tesla was trading in the low $100s. Since then, macroeconomic conditions have worsened, with multiple bank failures threatening a credit crunch for the economy and a demand crunch for Tesla. In response to flagging demand, Tesla's management has instituted multiple price cuts this year, and this move is causing margin pressures. The longer Musk and Co. execute this aggressive playbook, Tesla's margins are likely to remain under pressure. While we are modeling Tesla using long-term steady-state margins, Mr. Market is a far short-sighted person, and he could sell TSLA off during lean economic times.

And Musk warned about this during the annual shareholder meeting (emphasis added):

This is going to be a challenging 12 months, I sort of want to be realistic about it that Tesla is not immune to the global economic environment. I expect things to be just at a macroeconomic level difficult for at least the next 12 months. Like, Tesla will get through it, and we'll do well and I think we'll see a lot of companies go bankrupt.

The economy moves in cycles, and we've had a very long period of upcycle, and next twelve months will be [I think] difficult for everyone. During Berkshire Hathaway's annual meeting, Warren and Charlie actually said this year Berkshire companies are going to make less money. These are very well run organizations and that is generally true for the economy. It's important to remember that there are good times, and there are dark times, which are followed by good times. So my advice would be -

Don't look at the market for the next 12 months. If there's a dip, buy the dip, and you'll not be sorry. My guess is tough times for a year and then Tesla will emerge stronger than ever. Net present value of future cash flows will be incredibly high in my opinion. (Italic added for attribution clarity)

The long-term future for Tesla remains bright; however, near-term price action is likely to be volatile, and the technical chart does look ominous.

Final Thoughts: Tesla's Ominous-Looking Tryst With Technicals

Earlier in this note, we looked at the H&S pattern on Tesla's chart, and in my view, another rejection from the neckline would be extremely bearish for the stock. From a technical perspective, a breakdown of an H&S formation could result in a downward move equivalent to the gap between the head and the neckline. In Tesla's case, that level falls in the range of $40-60 (based on how you draw the neckline [horizontal or slanted]).

Now, I am not saying Tesla, Inc. stock is headed down to the mid-double digits; however, technicals suggest that this is a possible outcome. From a valuation perspective, Tesla can trade at such levels if it loses growth in a dire economy and the stock gets priced like a traditional automaker (~5-10x earnings). Hence, it is not unrealistic.

WeBull Desktop

While I don't think Tesla should be valued like a traditional automaker, I wouldn't rule it out, as Mr. Market can do crazy things. That said, I would view such a sharp selloff as a massive buying opportunity. Now, such a move is very unlikely to materialize until and unless we end up in a deep recession, which is certainly not my base case right now.

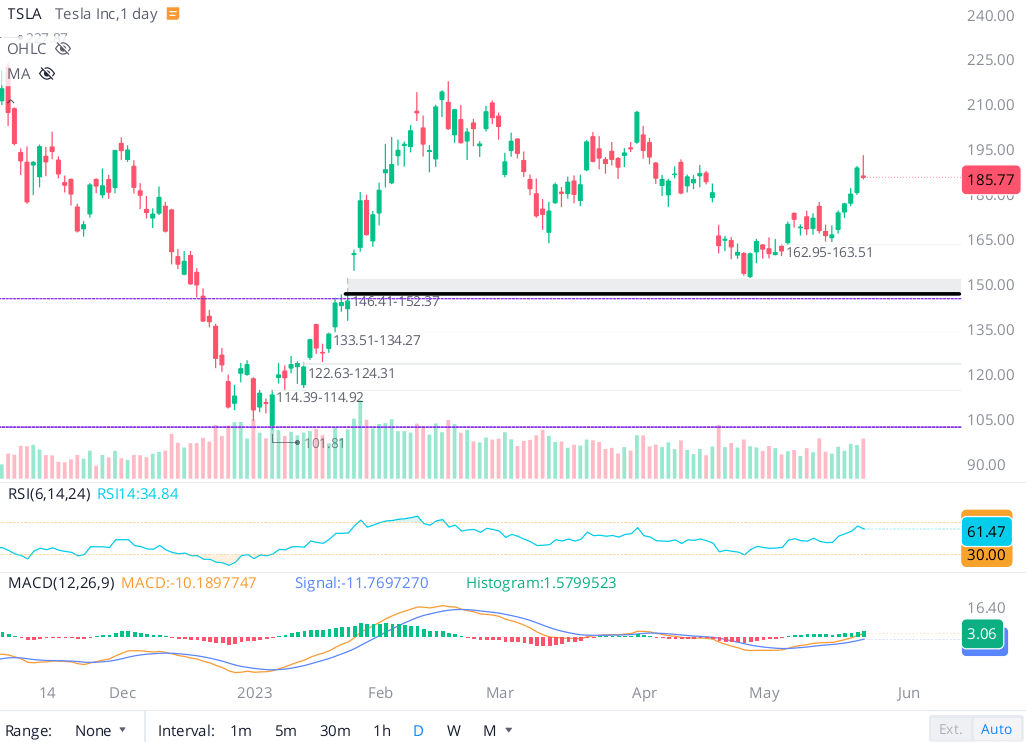

In the short term, I think a move down to $145 is very much on the table, given we still haven't filled the gap there. And if Tesla fails to hold that level, I can even see a re-test of recent lows, i.e., the low $100s.

WeBull Desktop

In a nutshell, Tesla's technical chart is looking ominous. A breakout of the neckline at $215 would make me change my view here. However, for the time being, I think investors can afford to remain patient with Tesla, Inc. stock and wait for a better entry point. If Tesla gets down to the mid-$100s, I will resume accumulation via a DCA plan.

Key Takeaway: I continue to rate Tesla, Inc. stock "Neutral" at ~$188 per share.

Thank you for reading, and happy investing! Please share any questions, thoughts, and/or concerns in the comments section below or DM me.

This article was written by

Ahan Vashi

5.24K Followers

Leader of The Quantamental Investor

We make investing in equity markets simple, fun, and profitable

I am the Author and Chief Financial Engineer at "The Quantamental Investor" - a community pursuing bold, active investing with proactive risk management. At TQI, our mission is to help retail investors build generational wealth in equity markets. To do so, we share robust model portfolios that cater to investor needs across different stages of the investor lifecycle. All of our investment ideas are thoroughly vetted through TQI's Quantamental Analysis process, which uses a mix of fundamental, quantitative, technical, and valuation analysis. If you're interested in learning more about our marketplace service, visit: The Quantamental Investor

Prior to joining The Quantamental Investment Group LLC, I served as the Head of Equity Research at LASI's SA Marketplace service - Beating The Market, for two years. In the past, I have worked as an Associate Fellow with Jacmel Growth Partners, a middle-market private equity firm in New York. My resume also includes a stint at Capgemini as a software engineer. With regards to academia, I hold a Master of Quantitative Finance degree from Rutgers Business School and a Bachelor of Technology degree in Electronics and Communication Engineering, whilst I am also pursuing the CFA certification (Level 2 candidate).

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

I also decided to leave in the writer's background, for fun.

For context, TSLA today closed at 184, so the author's 188 price rating is essentially a bearish assessment of the company.

After reading this article, I maintain a high of 300 in 2023.

https://seekingalpha.com/article/4607026-tesla-stock-pumped-and-warned-by-elon-musk?

- Tesla Stock: You Have Been Pumped And Warned By Elon Musk

Ahan Vashi

Investing Group LeaderThe Quantamental Investor

Summary

- Post its 2023 annual shareholder meeting, Tesla, Inc. stock is rallying higher, with investors seemingly buying the dip on Musk's advice.

- Traditionally, such events have served as boosters for Tesla's hype engine, and the latest shareholder meeting was no different.

- While Musk acknowledged the challenging macroeconomic environment, he reiterated a bullish long-term outlook for Tesla, citing exciting developments such as FSD [generalized AI], Cybertruck, Optimus Humanoid Bot, and more.

- The technical setup for Tesla continues to look precarious, and the stock is looking slightly overvalued after baking in Q1 results into the model.

- Hence, I continue to rate Tesla stock "Neutral/Hold" at $188.

A new wave of investor optimism seems to be pushing Tesla, Inc. (NASDAQ:TSLA) stock higher in the aftermath of its shareholder meeting (held on 16th May 2023), wherein CEO Elon Musk highlighted Tesla's long-term business prospects in emerging areas such as autonomous driving [FSD] and robotics [Optimus].

GoogleFinance

In late-2022/early-2023, I was incredibly bullish on Tesla in the mid to low $100s, at a time when Mr. Market was selling it off like a drunken psycho on a daily basis. After having accumulated Tesla for several months in the mid to low $100s, we sold half of our Tesla position at ~$194 a few weeks ago as the wild rally in TSLA took a pause at a key technical level at ~$200-215.

While market participants are clearly getting excited about Tesla once again, I am sticking to a "Neutral" rating for TSLA after having shifted my stance in light of Tesla's Q1 earnings back in April. If you have been following my work on Tesla, you know that my rationale for the downgrade was based on greater macroeconomic uncertainties, dangers of Tesla's recession playbook [making it a binary bet on FSD], and ominous technical setup. Find a more detailed explanation here:

Despite Elon Musk's dire warnings on the economy, investors have been piling into TSLA stock, which apparently looks set to re-test the neckline of its head and shoulders pattern. As you can observe in the chart below, Tesla's stock has already been rejected twice at this key technical level. If Tesla fails to break past this area of resistance, technically, the stock could be headed back down to the mid $100s [and even to the low $100s] in a continuation of the reverse gamma squeeze we saw in late-2022.

WeBull Desktop

In this note, we will discuss major takeaways from Tesla's Annual Shareholder Meeting. And then check up on TSLA's ominous-looking technical chart.

Highlights Of Tesla 2023 Shareholder Meeting

Keeping in tradition with past investor events, Tesla's 2023 Annual Shareholder Meeting and Musk's subsequent CNBC interview (with David Faber) were filled with lots of hyperbolic statements such as "FSD could be the ChatGPT moment for Tesla" and "Demand for Tesla's Optimus Humanoid Bot could be 10 billion units."

Here's a list of noteworthy announcements from the meeting:

- Elon Musk is staying on as CEO of Tesla for the foreseeable future and is planning to refocus his efforts on the EV giant's AI products (FSD and Optimus) after handing over the reins at Twitter to Linda Yaccarino.

- The macroeconomic environment is likely to remain tough for the next 12 months, and Tesla is not immune to global economic conditions.

- Tesla will try traditional advertising to spur additional demand for its electric vehicles ("EVs").

- Tesla is set to start deliveries for Cybertruck in 2023, targeting production of 250-500K units per year (at scale).

- Tesla is working on two new EV models that can result in additional production of 5M units per year. (Potentially a compact car and a van.)

- Tesla FSD is close to reaching full autonomy, and reaching this feat could lead to the greatest increase in asset value of all time, as Tesla FSD can boost the value of Tesla's fleet by 4-5x. Tesla EV gross margins could shoot up to ~80% (from ~20%) when FSD reaches full autonomy.

- Optimus bot will use the same generalized AI being created for FSD. And demand for Optimus could be ~10B or ~20B units because every human will want one or two. (The video shared during the meeting showed that Optimus had come a long way from where it was at the last reveal, but I would take that demand figure with a pinch of salt.)

- Musk strongly believes "Optimus will be the majority of Tesla's value over the long-term."

- Tesla's energy business is scaling well, and the margins here are likely to remain in the 20-30% range.

Now, let's discuss Tesla's business outlook in light of its shareholder meeting.

What Is The Long-Term Business Outlook?

While Musk stoked the hype engine quite a bit with positive commentary on ambitious projects such as FSD, Cybertruck, Optimus humanoid bot, and two new EV vehicle models (likely a compact car and a Van), none of these are likely to move the needle for Tesla in the near-term.

That said, Tesla's recession playbook is still expected to result in volume growth during 2023. According to consensus street estimates (and Musk), Tesla is likely to do $100B in revenue this year.

SeekingAlpha

Going forward, consensus analyst estimates peg CAGR sales growth to be in the low-to-mid-20s, which is a far cry from where Tesla's growth has been over the past decade. Given Tesla's scale, I think a slowdown is natural; however, a growth slowdown raises question marks over TSLA's valuation premium. Now, bulls like to value Tesla as a high-margin software company, whereas bears prefer a valuation more in line with other automakers.

Personally, I think the reality is somewhere in between. As I said in my previous note, Tesla is turning into a binary bet on FSD. According to Musk, FSD could boost Tesla's gross margins to ~80%. While I am skeptical about that figure, I think that if FSD achieves full autonomy, Tesla can deliver software-like margins. In this scenario, Tesla would deserve a multiple similar to an Apple Inc. (AAPL) (~25-30x earnings) and not a Ford Motor Company (F) (~5-10x earnings).

Will Tesla FSD reach full autonomy in 2023 or 2024? I don't know. While the likes of Cathie Wood (and many Tesla bulls) think it could happen this year, the jury is still out there. As an investor, I prefer to wait for evidence before trying to model something like FSD into my valuation estimate for the company. And so, I am not altering my model based on Musk's positive FSD commentary from the annual shareholder meeting.

TQI's Valuation Model For Tesla

With Q1 results coming (more or less) in line with expectations, I am sticking to most of my pre-earnings assumptions for Tesla. However, in order to factor in the added risk of Tesla turning into a binary bet on FSD due to Musk's recession playbook, I raised our model's "Required IRR" from 15% to 20%.

Also, Tesla's recession playbook is killing its free cash flow ("FCF") generation, and in the interest of improving the margin of safety in our model, I reduced the "Buyback as a % of FCF" (capital return program) assumption from 25% to 0%.

Here's my updated valuation for Tesla:

TQI Valuation Model (TQIG.org)

According to these results, Tesla's fair value is ~$155 per share. With the stock trading at $188 per share, it is currently overvalued by ~17.5%. Now, I am happy to pay a premium for a high-quality company like Tesla; however, is the risk/reward attractive enough to justify an investment at current levels?

TQI Valuation Model (TQIG.org)

Assuming a base case P/FCF exit multiple of 25x, I see Tesla hitting $377 per share by 2027. As can be seen below, Tesla is projected to deliver CAGR returns of 14.94% for the next five years, which more or less meets my investment hurdle rate of 15%.

However, the valuation is not exciting enough to justify a long position by itself, as was the case in late-2022 when Tesla was trading in the low $100s. Since then, macroeconomic conditions have worsened, with multiple bank failures threatening a credit crunch for the economy and a demand crunch for Tesla. In response to flagging demand, Tesla's management has instituted multiple price cuts this year, and this move is causing margin pressures. The longer Musk and Co. execute this aggressive playbook, Tesla's margins are likely to remain under pressure. While we are modeling Tesla using long-term steady-state margins, Mr. Market is a far short-sighted person, and he could sell TSLA off during lean economic times.

And Musk warned about this during the annual shareholder meeting (emphasis added):

This is going to be a challenging 12 months, I sort of want to be realistic about it that Tesla is not immune to the global economic environment. I expect things to be just at a macroeconomic level difficult for at least the next 12 months. Like, Tesla will get through it, and we'll do well and I think we'll see a lot of companies go bankrupt.

The economy moves in cycles, and we've had a very long period of upcycle, and next twelve months will be [I think] difficult for everyone. During Berkshire Hathaway's annual meeting, Warren and Charlie actually said this year Berkshire companies are going to make less money. These are very well run organizations and that is generally true for the economy. It's important to remember that there are good times, and there are dark times, which are followed by good times. So my advice would be -

Don't look at the market for the next 12 months. If there's a dip, buy the dip, and you'll not be sorry. My guess is tough times for a year and then Tesla will emerge stronger than ever. Net present value of future cash flows will be incredibly high in my opinion. (Italic added for attribution clarity)

The long-term future for Tesla remains bright; however, near-term price action is likely to be volatile, and the technical chart does look ominous.

Final Thoughts: Tesla's Ominous-Looking Tryst With Technicals

Earlier in this note, we looked at the H&S pattern on Tesla's chart, and in my view, another rejection from the neckline would be extremely bearish for the stock. From a technical perspective, a breakdown of an H&S formation could result in a downward move equivalent to the gap between the head and the neckline. In Tesla's case, that level falls in the range of $40-60 (based on how you draw the neckline [horizontal or slanted]).

Now, I am not saying Tesla, Inc. stock is headed down to the mid-double digits; however, technicals suggest that this is a possible outcome. From a valuation perspective, Tesla can trade at such levels if it loses growth in a dire economy and the stock gets priced like a traditional automaker (~5-10x earnings). Hence, it is not unrealistic.

WeBull Desktop

While I don't think Tesla should be valued like a traditional automaker, I wouldn't rule it out, as Mr. Market can do crazy things. That said, I would view such a sharp selloff as a massive buying opportunity. Now, such a move is very unlikely to materialize until and unless we end up in a deep recession, which is certainly not my base case right now.

In the short term, I think a move down to $145 is very much on the table, given we still haven't filled the gap there. And if Tesla fails to hold that level, I can even see a re-test of recent lows, i.e., the low $100s.

WeBull Desktop

In a nutshell, Tesla's technical chart is looking ominous. A breakout of the neckline at $215 would make me change my view here. However, for the time being, I think investors can afford to remain patient with Tesla, Inc. stock and wait for a better entry point. If Tesla gets down to the mid-$100s, I will resume accumulation via a DCA plan.

Key Takeaway: I continue to rate Tesla, Inc. stock "Neutral" at ~$188 per share.

Thank you for reading, and happy investing! Please share any questions, thoughts, and/or concerns in the comments section below or DM me.

This article was written by

Ahan Vashi

5.24K Followers

Leader of The Quantamental Investor

We make investing in equity markets simple, fun, and profitable

I am the Author and Chief Financial Engineer at "The Quantamental Investor" - a community pursuing bold, active investing with proactive risk management. At TQI, our mission is to help retail investors build generational wealth in equity markets. To do so, we share robust model portfolios that cater to investor needs across different stages of the investor lifecycle. All of our investment ideas are thoroughly vetted through TQI's Quantamental Analysis process, which uses a mix of fundamental, quantitative, technical, and valuation analysis. If you're interested in learning more about our marketplace service, visit: The Quantamental Investor

Prior to joining The Quantamental Investment Group LLC, I served as the Head of Equity Research at LASI's SA Marketplace service - Beating The Market, for two years. In the past, I have worked as an Associate Fellow with Jacmel Growth Partners, a middle-market private equity firm in New York. My resume also includes a stint at Capgemini as a software engineer. With regards to academia, I hold a Master of Quantitative Finance degree from Rutgers Business School and a Bachelor of Technology degree in Electronics and Communication Engineering, whilst I am also pursuing the CFA certification (Level 2 candidate).

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Last edited:

Reuters had two Ford EV articles yesterday:-

Ford strikes deal with Tesla to gain access to rival charging stations starting 2024

By Hyunjoo Jin

, David Shepardson

and Abhirup Roy

May 25, 20236:49 PM EDTUpdated 13 hours ago

[1/2] A Tesla logo is seen at Tesla Shanghai Gigafactory in Shanghai, China January 7, 2019. REUTERS/Aly Song

May 25 (Reuters) - Ford Motor Co (F.N) said on Thursday it has agreed with Tesla Inc (TSLA.O) to allow its electric vehicle owners to gain access to more than 12,000 Tesla Superchargers in North America in early 2024.

The tie-up between the rivals makes Ford the first major automaker to embrace Tesla's proprietary charging standard, giving the automaker access to the biggest network of high-speed Superchargers in the United States.

Access to charging stations is considered one of the main hurdles so far to broader acceptance of electric vehicles, analysts have said.

Tesla said last November it would open its proprietary charging design to other automakers and charging network operators.

A Tesla-developed adapter will provide Ford EVs fitted with the Combined Charging System (CCS) port access to Tesla’s V3 Superchargers. Ford will equip future EVs with Tesla's own charging standard, removing the need for an adapter for direct access to Tesla Superchargers, starting in 2025.

"The idea is that we don't want the Tesla supercharger network to be like a walled garden. We want it to be something that is supportive of electrification and sustainable transport in general," Tesla CEO Elon Musk said during an online Twitter Spaces conversation with Ford CEO Jim Farley.

"We love the locations, we love the reliability, your routing software, the ease of use of the connector, the reliability of it," Farley said.

"Tesla storms through the train station like 300 kilometers per hour Shinkansen," Farley said, referring to Japanese bullet trains. "We're learning a lot."

Tesla had 17,711 Superchargers, accounting for about 60% of total U.S. fast chargers, which can add hundreds of miles of driving range in an hour or less.

Farley on Thursday announced the partnership during the Twitter Spaces conversation. Twitter is owned by Musk.

The event comes just a day after Twitter crashed repeatedly during a highly anticipated live audio chat between Musk and Florida Governor Ron DeSantis, setting back Musk's efforts to promote the social media firm he bought for $44 billion last year.

The Musk-Farley Twitter Spaces conversation lasted about a half hour and came off without technical glitches.

Farley said earlier on Thursday at a Morgan Stanley forum that "on the infrastructure side, I think it's room for some collaboration between the auto companies, which is totally unnatural for us."

Farley added, "I think we need to start – I mean, I think the first step is to work together in a way we haven't, probably with the new EV brands and the traditional old companies."

For example, he called it "totally ridiculous" that the industry has multiple plugs for its charging networks and "we can't even agree on what plug to use."

Musk earlier this month tweeted: "I think Ford’s overall strategy with EVs is smart. The electric F-150 (Lightning) has high demand."

He also defended Ford over its losses on its electric vehicle business. "Always tough with margins for new vehicle lines, especially when there are major technology shifts."

Farley said on Thursday that Ford should take the lead to reach out to a new company like a Tesla or a Nio Inc (9866.HK) or BYD (002594.SZ) "to kind of work together in a non-natural way as competitors. I think you'll see Ford do that just because that's what kind of company we are."

This year, Tesla has started to expand beyond its proprietary connectors and incorporate the rival CCS standard at some of its charging stations in the United States, as the Biden administration seeks to provide billions in subsidies to expand charging networks.

+ + +

Ford CEO says China main EV rival, not GM, Toyota

By David Shepardson

May 25, 20237:31 PM EDTUpdated 12 hours ago

Ford Motor Company CEO Jim Farley announces Ford will partner with Chinese-based, Amperex Technology, to build an all-electric vehicle battery plant in Marshall, Michigan, during a press conference in Romulus, Michigan U.S., February 13, 2023. REUTERS/Rebecca Cook

May 25 (Reuters) - Ford Motor Co (F.N) CEO Jim Farley said on Thursday Chinese electric vehicle makers are its main rivals in the sector, but the company has hurdles competing on cost at a smaller scale.

"I think we see the Chinese as the main competitor, not GM (GM.N) or Toyota (7203.T),{not mentioned Tesla, didn't want to upset Elon on same day as charger deal}" Farley said at the Morgan Stanley Sustainable Finance Summit. "The Chinese are going to be the powerhouse."

China, the world's largest auto market, has some of the best battery technology and dominates EV production, Farley said. He cited BYD (002594.SZ), Geely (0175.HK), Great Wall, Changan (000625.SZ) SAIC as among the "winners" among Chinese automakers.

To beat Chinese automakers, Farley said Ford needs distinctive branding, which he believes it has, or lower costs. "But how do you beat on them on cost if their scale is five times yours?" Farley said. "The Europeans let (Chinese automakers) in - so now they are selling in high volume in Europe."

Ford said in February it would invest $3.5 billion to build an electric vehicle battery plant in Michigan using technology from Chinese partner CATL (300750.SZ) to produce lower-cost batteries.

The U.S. Treasury must still issue rules later this year that will determine whether the Ford SAIC arrangement violates a prohibition on "Foreign Entities of Concern" that is part of a $7,500 EV tax credit. Ford has faced criticism from Senator Marco Rubio for the plan.

Ford strikes deal with Tesla to gain access to rival charging stations starting 2024

By Hyunjoo Jin

, David Shepardson

and Abhirup Roy

May 25, 20236:49 PM EDTUpdated 13 hours ago

[1/2] A Tesla logo is seen at Tesla Shanghai Gigafactory in Shanghai, China January 7, 2019. REUTERS/Aly Song

May 25 (Reuters) - Ford Motor Co (F.N) said on Thursday it has agreed with Tesla Inc (TSLA.O) to allow its electric vehicle owners to gain access to more than 12,000 Tesla Superchargers in North America in early 2024.

The tie-up between the rivals makes Ford the first major automaker to embrace Tesla's proprietary charging standard, giving the automaker access to the biggest network of high-speed Superchargers in the United States.

Access to charging stations is considered one of the main hurdles so far to broader acceptance of electric vehicles, analysts have said.

Tesla said last November it would open its proprietary charging design to other automakers and charging network operators.

A Tesla-developed adapter will provide Ford EVs fitted with the Combined Charging System (CCS) port access to Tesla’s V3 Superchargers. Ford will equip future EVs with Tesla's own charging standard, removing the need for an adapter for direct access to Tesla Superchargers, starting in 2025.

"The idea is that we don't want the Tesla supercharger network to be like a walled garden. We want it to be something that is supportive of electrification and sustainable transport in general," Tesla CEO Elon Musk said during an online Twitter Spaces conversation with Ford CEO Jim Farley.

"We love the locations, we love the reliability, your routing software, the ease of use of the connector, the reliability of it," Farley said.

"Tesla storms through the train station like 300 kilometers per hour Shinkansen," Farley said, referring to Japanese bullet trains. "We're learning a lot."

Tesla had 17,711 Superchargers, accounting for about 60% of total U.S. fast chargers, which can add hundreds of miles of driving range in an hour or less.

Farley on Thursday announced the partnership during the Twitter Spaces conversation. Twitter is owned by Musk.

The event comes just a day after Twitter crashed repeatedly during a highly anticipated live audio chat between Musk and Florida Governor Ron DeSantis, setting back Musk's efforts to promote the social media firm he bought for $44 billion last year.

The Musk-Farley Twitter Spaces conversation lasted about a half hour and came off without technical glitches.

Farley said earlier on Thursday at a Morgan Stanley forum that "on the infrastructure side, I think it's room for some collaboration between the auto companies, which is totally unnatural for us."

Farley added, "I think we need to start – I mean, I think the first step is to work together in a way we haven't, probably with the new EV brands and the traditional old companies."

For example, he called it "totally ridiculous" that the industry has multiple plugs for its charging networks and "we can't even agree on what plug to use."

Musk earlier this month tweeted: "I think Ford’s overall strategy with EVs is smart. The electric F-150 (Lightning) has high demand."

He also defended Ford over its losses on its electric vehicle business. "Always tough with margins for new vehicle lines, especially when there are major technology shifts."

Farley said on Thursday that Ford should take the lead to reach out to a new company like a Tesla or a Nio Inc (9866.HK) or BYD (002594.SZ) "to kind of work together in a non-natural way as competitors. I think you'll see Ford do that just because that's what kind of company we are."

This year, Tesla has started to expand beyond its proprietary connectors and incorporate the rival CCS standard at some of its charging stations in the United States, as the Biden administration seeks to provide billions in subsidies to expand charging networks.

+ + +

Ford CEO says China main EV rival, not GM, Toyota

By David Shepardson

May 25, 20237:31 PM EDTUpdated 12 hours ago

Ford Motor Company CEO Jim Farley announces Ford will partner with Chinese-based, Amperex Technology, to build an all-electric vehicle battery plant in Marshall, Michigan, during a press conference in Romulus, Michigan U.S., February 13, 2023. REUTERS/Rebecca Cook

May 25 (Reuters) - Ford Motor Co (F.N) CEO Jim Farley said on Thursday Chinese electric vehicle makers are its main rivals in the sector, but the company has hurdles competing on cost at a smaller scale.

"I think we see the Chinese as the main competitor, not GM (GM.N) or Toyota (7203.T),{not mentioned Tesla, didn't want to upset Elon on same day as charger deal}

" Farley said at the Morgan Stanley Sustainable Finance Summit. "The Chinese are going to be the powerhouse."China, the world's largest auto market, has some of the best battery technology and dominates EV production, Farley said. He cited BYD (002594.SZ), Geely (0175.HK), Great Wall, Changan (000625.SZ) SAIC as among the "winners" among Chinese automakers.

To beat Chinese automakers, Farley said Ford needs distinctive branding, which he believes it has, or lower costs. "But how do you beat on them on cost if their scale is five times yours?" Farley said. "The Europeans let (Chinese automakers) in - so now they are selling in high volume in Europe."

Ford said in February it would invest $3.5 billion to build an electric vehicle battery plant in Michigan using technology from Chinese partner CATL (300750.SZ) to produce lower-cost batteries.

The U.S. Treasury must still issue rules later this year that will determine whether the Ford SAIC arrangement violates a prohibition on "Foreign Entities of Concern" that is part of a $7,500 EV tax credit. Ford has faced criticism from Senator Marco Rubio for the plan.

That's a fact, GM is no competition in the EV space and won't be for quite some time and certainly not 2025 that Barra once promised.Reuters had two Ford EV articles yesterday:-

Ford strikes deal with Tesla to gain access to rival charging stations starting 2024

By Hyunjoo Jin

, David Shepardson

and Abhirup Roy

May 25, 20236:49 PM EDTUpdated 13 hours ago

[1/2] A Tesla logo is seen at Tesla Shanghai Gigafactory in Shanghai, China January 7, 2019. REUTERS/Aly Song

May 25 (Reuters) - Ford Motor Co (F.N) said on Thursday it has agreed with Tesla Inc (TSLA.O) to allow its electric vehicle owners to gain access to more than 12,000 Tesla Superchargers in North America in early 2024.

The tie-up between the rivals makes Ford the first major automaker to embrace Tesla's proprietary charging standard, giving the automaker access to the biggest network of high-speed Superchargers in the United States.

Access to charging stations is considered one of the main hurdles so far to broader acceptance of electric vehicles, analysts have said.

Tesla said last November it would open its proprietary charging design to other automakers and charging network operators.

A Tesla-developed adapter will provide Ford EVs fitted with the Combined Charging System (CCS) port access to Tesla’s V3 Superchargers. Ford will equip future EVs with Tesla's own charging standard, removing the need for an adapter for direct access to Tesla Superchargers, starting in 2025.

"The idea is that we don't want the Tesla supercharger network to be like a walled garden. We want it to be something that is supportive of electrification and sustainable transport in general," Tesla CEO Elon Musk said during an online Twitter Spaces conversation with Ford CEO Jim Farley.

"We love the locations, we love the reliability, your routing software, the ease of use of the connector, the reliability of it," Farley said.

"Tesla storms through the train station like 300 kilometers per hour Shinkansen," Farley said, referring to Japanese bullet trains. "We're learning a lot."

Tesla had 17,711 Superchargers, accounting for about 60% of total U.S. fast chargers, which can add hundreds of miles of driving range in an hour or less.

Farley on Thursday announced the partnership during the Twitter Spaces conversation. Twitter is owned by Musk.

The event comes just a day after Twitter crashed repeatedly during a highly anticipated live audio chat between Musk and Florida Governor Ron DeSantis, setting back Musk's efforts to promote the social media firm he bought for $44 billion last year.

The Musk-Farley Twitter Spaces conversation lasted about a half hour and came off without technical glitches.

Farley said earlier on Thursday at a Morgan Stanley forum that "on the infrastructure side, I think it's room for some collaboration between the auto companies, which is totally unnatural for us."

Farley added, "I think we need to start – I mean, I think the first step is to work together in a way we haven't, probably with the new EV brands and the traditional old companies."

For example, he called it "totally ridiculous" that the industry has multiple plugs for its charging networks and "we can't even agree on what plug to use."

Musk earlier this month tweeted: "I think Ford’s overall strategy with EVs is smart. The electric F-150 (Lightning) has high demand."

He also defended Ford over its losses on its electric vehicle business. "Always tough with margins for new vehicle lines, especially when there are major technology shifts."

Farley said on Thursday that Ford should take the lead to reach out to a new company like a Tesla or a Nio Inc (9866.HK) or BYD (002594.SZ) "to kind of work together in a non-natural way as competitors. I think you'll see Ford do that just because that's what kind of company we are."

This year, Tesla has started to expand beyond its proprietary connectors and incorporate the rival CCS standard at some of its charging stations in the United States, as the Biden administration seeks to provide billions in subsidies to expand charging networks.

+ + +

Ford CEO says China main EV rival, not GM, Toyota

By David Shepardson

May 25, 20237:31 PM EDTUpdated 12 hours ago

Ford Motor Company CEO Jim Farley announces Ford will partner with Chinese-based, Amperex Technology, to build an all-electric vehicle battery plant in Marshall, Michigan, during a press conference in Romulus, Michigan U.S., February 13, 2023. REUTERS/Rebecca Cook

May 25 (Reuters) - Ford Motor Co (F.N) CEO Jim Farley said on Thursday Chinese electric vehicle makers are its main rivals in the sector, but the company has hurdles competing on cost at a smaller scale.

"I think we see the Chinese as the main competitor, not GM (GM.N) or Toyota (7203.T),{not mentioned Tesla, didn't want to upset Elon on same day as charger deal}

China, the world's largest auto market, has some of the best battery technology and dominates EV production, Farley said. He cited BYD (002594.SZ), Geely (0175.HK), Great Wall, Changan (000625.SZ) SAIC as among the "winners" among Chinese automakers.

To beat Chinese automakers, Farley said Ford needs distinctive branding, which he believes it has, or lower costs. "But how do you beat on them on cost if their scale is five times yours?" Farley said. "The Europeans let (Chinese automakers) in - so now they are selling in high volume in Europe."

Ford said in February it would invest $3.5 billion to build an electric vehicle battery plant in Michigan using technology from Chinese partner CATL (300750.SZ) to produce lower-cost batteries.

The U.S. Treasury must still issue rules later this year that will determine whether the Ford SAIC arrangement violates a prohibition on "Foreign Entities of Concern" that is part of a $7,500 EV tax credit. Ford has faced criticism from Senator Marco Rubio for the plan.

The Chinese are definitely the real competition. They are aggressive and dynamic, always innovating with design and tech. Luckily for US auto manufacturers, I can't see many Americans buying them, if Japan's experience of US consumers in the 70s is any indication. It will change in time, but many things can happen to keep Chinese EVs far from our shores.

Spy is about to go to ath after congress pass the debt ceiling next week. Almost all the faang companies are recovering from the low last year. The stars are aligning and bears are gonna get fooked soon with tsla if they don’t cover their shorts soon.

https://www.zenger.news/2023/05/26/...rovements-promise-30-50-cuts-in-battery-cost/

Tesla’s ‘Golden Goose’: Improvements Promise 30-50% Cuts In Battery Cost

Tesla announced in January it plans to invest over $3.6 billion to grow its Giga Nevada with two new factories.

A Tesla, Inc. (NASDAQ:TSLA) bull came away impressed from a visit to the electric vehicle giant’s Giga Nevada, which manufactures lithium-ion batteries and EV components.

Wedbush analyst Daniel Ives has an Outperform rating and a $183 price target for the stock.

Aiming to reduce battery costs by 30-50% over the long term is the “golden goose” for Tesla, Ives said in a note.

The company is taking great efforts to meticulously create cost efficiencies while strategically expanding, the analyst said following his walk around the factory.

It is now aiming to produce about 100 Gigawatt-hour capacity of in-house 4680 battery cells per year, he said, adding that this along with Panasonic Holdings Corp. cells, would be sufficient to power about 2 million annually.

This, according to the analyst, will be a crucial step to ramp up battery production nearly 29 times by 2030

Giga Nevada produced 7.3 billion battery cells, or 37 GWh+ annually, and supplied a total of about 3.6 million drive units, the company said at the start of the year, Ives noted. With the $3.6 billion investment in Nevada announced in January, the company plans to nearly triple its historical GWh output, he added.

“We view this as a major step forward for Tesla which we believe could potentially be ahead of schedule while from the bird’s eye view creating large economies of scale for costs and laying out the blueprint for the future,” Ives said.

The analyst noted that the 4680 batteries focus on a 16% increase in range and six times power while cutting capex per GWh, and its next-gen drive units aim for a 75% reduction in silicon carbide, zero rare-earth metals usage and a 50% reduction in factory footprint.

“The all-important 4680 production ramps, battery cost-cutting of 30% – 50%, and margins will be the largest focal points of the year along with units/gross margins balance,” the analyst said.

Tesla’s ‘Golden Goose’: Improvements Promise 30-50% Cuts In Battery Cost

Tesla announced in January it plans to invest over $3.6 billion to grow its Giga Nevada with two new factories.

A Tesla, Inc. (NASDAQ:TSLA) bull came away impressed from a visit to the electric vehicle giant’s Giga Nevada, which manufactures lithium-ion batteries and EV components.

Wedbush analyst Daniel Ives has an Outperform rating and a $183 price target for the stock.

Aiming to reduce battery costs by 30-50% over the long term is the “golden goose” for Tesla, Ives said in a note.

The company is taking great efforts to meticulously create cost efficiencies while strategically expanding, the analyst said following his walk around the factory.

It is now aiming to produce about 100 Gigawatt-hour capacity of in-house 4680 battery cells per year, he said, adding that this along with Panasonic Holdings Corp. cells, would be sufficient to power about 2 million annually.

This, according to the analyst, will be a crucial step to ramp up battery production nearly 29 times by 2030

Giga Nevada produced 7.3 billion battery cells, or 37 GWh+ annually, and supplied a total of about 3.6 million drive units, the company said at the start of the year, Ives noted. With the $3.6 billion investment in Nevada announced in January, the company plans to nearly triple its historical GWh output, he added.

“We view this as a major step forward for Tesla which we believe could potentially be ahead of schedule while from the bird’s eye view creating large economies of scale for costs and laying out the blueprint for the future,” Ives said.

The analyst noted that the 4680 batteries focus on a 16% increase in range and six times power while cutting capex per GWh, and its next-gen drive units aim for a 75% reduction in silicon carbide, zero rare-earth metals usage and a 50% reduction in factory footprint.

“The all-important 4680 production ramps, battery cost-cutting of 30% – 50%, and margins will be the largest focal points of the year along with units/gross margins balance,” the analyst said.