Interest rates, influenced by Treasury bond yields, are crucial in determining the discount rates used in valuing stocks. When Treasury yields rise, the discount rate for future cash flows also rises, reducing the present value of these cash flows. Tech stocks, which often have high growth expectations and cash flows projected far into the future, are particularly sensitive to changes in discount rates.

With that premise, today I backtested the following idea:

Signal:

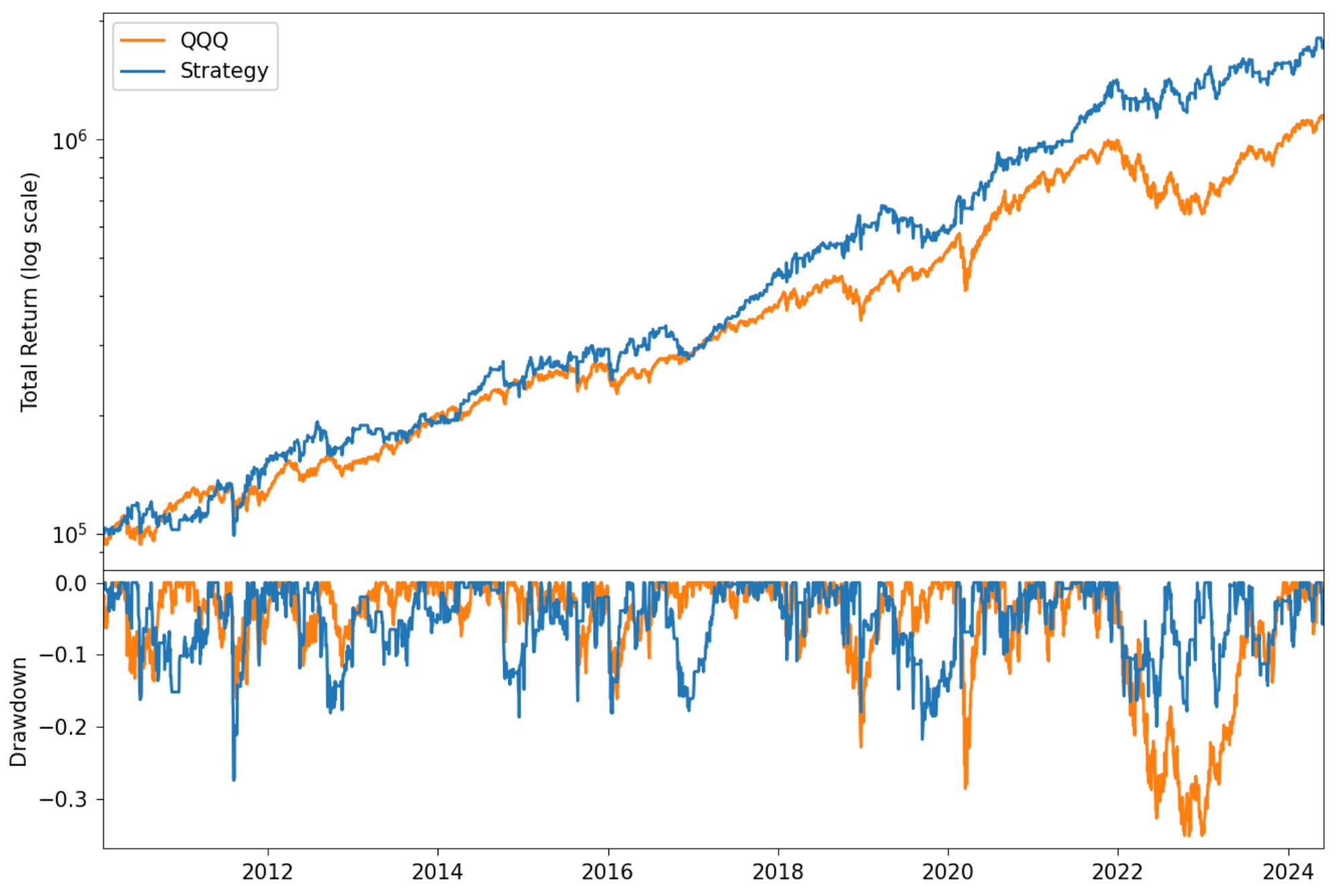

Equity curve

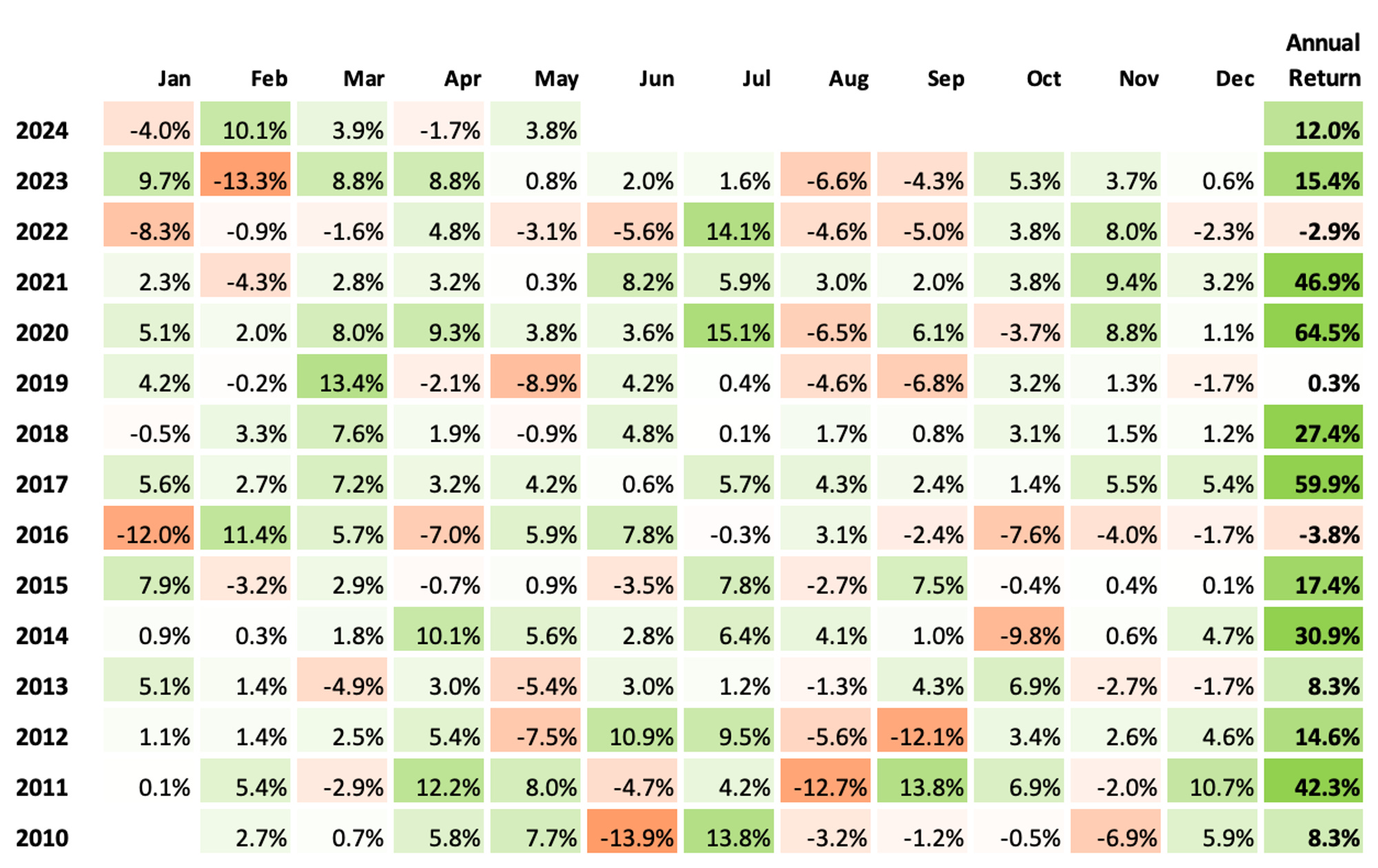

Monthly and annual returns

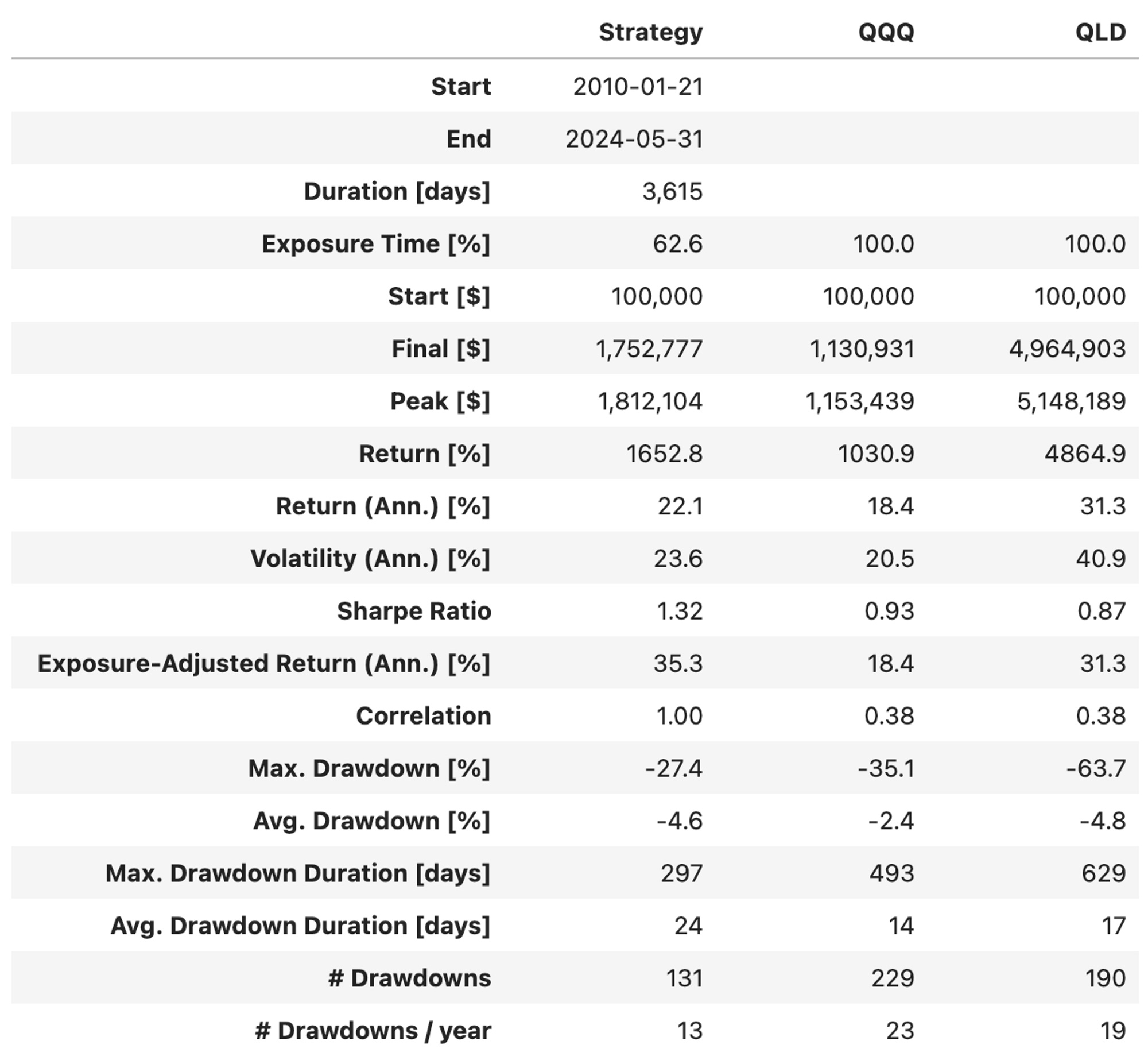

Summary of the backtest statistics

Summary of the backtest trades

Key points:

Maybe the RSI of the spread, computed as stated, is not the best instrument to trade this relationship... anyway...

I created a full write-up with all the details here.

I'd love to hear what you guys think...

Cheers!

With that premise, today I backtested the following idea:

Signal:

- We compute a spread between QQQ (QLD using 2x leverage) and TLT (UBT using 2x leverage) as the ratio between both prices;

- We then compute the 3-day RSI of the spread to track overbought and oversold signals;

- When the 3-day RSI of the spread is below 10, we go long on QQQ;

- When the 3-day RSI of the spread is above 90, we go long on TLT;

- When the 3-day RSI of the spread is above 60, we close QQQ trade;

- When the 3-day RSI of the spread is below 40, we close TLT trade.

Equity curve

Monthly and annual returns

Summary of the backtest statistics

Summary of the backtest trades

Key points:

- The annual return achieved 22.1% in comparison to 18.4% QQQ in the same period;

- This annual return was lower than the QLD's (31.3%); however, the strategy was invested only 63% of the time. If it were invested the whole period, the return would have been 35.3% (the exposure-adjusted return);

- The strategy delivered a lower maximum drawdown (27%) in comparison to both QQQ and QLD;

- Although the average drawdown was worse (4.6% vs. 2.4% QQQ) and longer (24 days vs. 14 days QQQ), the strategy had almost half of the drawdowns (13/year vs. 23/year QQQ).

Maybe the RSI of the spread, computed as stated, is not the best instrument to trade this relationship... anyway...

I created a full write-up with all the details here.

I'd love to hear what you guys think...

Cheers!