If you're going to get involved in these strategies you need to not be selling far OTM puts due to the inherent convexity of their valuation as they go from being OTM->ATM. People keep thinking that if an option goes in the money somehow the trade has gone wrong and this is false - all that matters is the price of the option when sold vs when bought back. This "never lose" mentality keeps people pursuing "no heat" type trades that become a fucking disaster when vol explodes and the market takes a big dump. You can delude yourself that this doesn't happen often enough to matter but it does and when it does it does badly. Relying on it not to happen at rock bottom VIX is just asking to be taught a lesson.

If you sell far OTM options you need to sell *more* in order to collect the same potential premium you'd make from selling a lower amount of ATM options. ATM options are at peak gamma, the rate of damage to your account is not going to be accelerating when the market goes against you whereas with OTM options it *is* going to be accelerating until they eventually become ATM (and beyond) until you either get liquidated, shit your pants, or both. You can easily destroy your entire account trying to juice up these short-dated options to make a "sure thing" return. If there's anything in trading that's to be avoided: it's a sure thing. Nine times out of ten, "sure thing" is a synonym for massive hidden risk.

Now yes, of course you're much more likely to have an ATM option end up ITM but as I said before, all that matters is what you sold it at and what you bought it back at. With an ATM option there's a decent amount of premium there but with these short dated fat out OTM options there's almost no premium at all, but a ton of embedded risk. Nobody who has the ability to survive this long term is selling these things naked, they're delta hedged either with the underlying or indirectly with VIX options or VX futures, spread against unit puts, etc. All they're looking to do is collect the difference between implied vol and realized vol and/or the bid/ask spread of the options themselves. They're not just shorting shit naked and hoping the market doesn't crash next week.

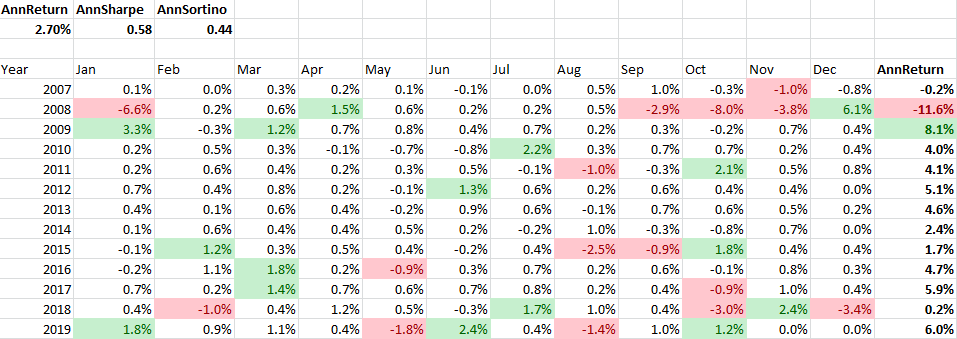

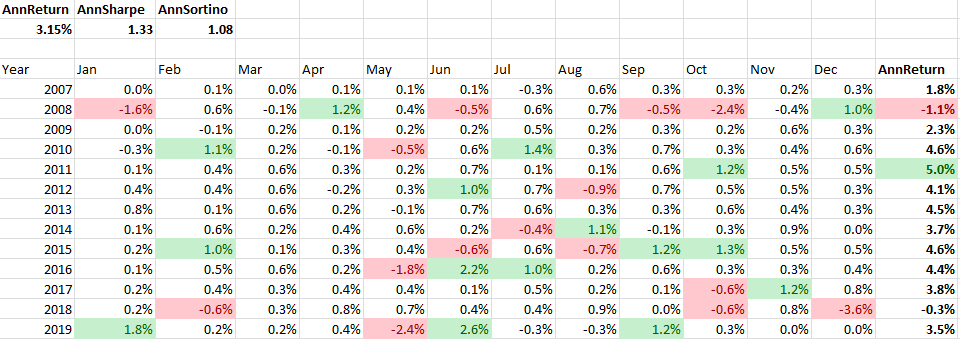

I'm once again going to post charts from the latter half of August, 2015 because some folks still aren't getting it.

View attachment 172194

View attachment 172195

View attachment 172192

On 8/18/2015:

- EW U2015 2100 (ATM) put was 14-19.75 in price.

- EW U2015 2000 (OTM) put was 1.25-1.85 in price.

If you sold 10 OTM puts at 1.5 a piece you'd be on track to collect 750$ in premium (1.5 * 50 * 10) by expiration. If you sold 1 ATM put at 16, you'd be on track to collect 800$ in premium (16 * 50 * 1) by expiration. Both around 0.75% return on a 100k account.

On 8/24/2015:

- EW U2015 2100 (ATM) put was 230 in price (14x loss).

- EW U2015 2000 (OTM) put was 130 in price (87x loss).

The guy who sold 1 ATM put is now 11,500$ (230 * 50 * 1) in the hole worst case.

The guy who sold 10 OTM puts is now 65,000$ (130 * 50 * 10) in the hole worst case.

Do you want to be the guy selling ATM or OTM here? Stop thinking that options expiring OTM and "high probability premium collecting" or worse "income collecting" is the end goal, you'll eventually get smoked. Also, selling a smaller amount of these things across a whole bunch of different stocks is not diversification one bit. When shit hits the fan they're all getting killed.

If you want a decent overview of things, I'd recommend these from Surlytrader for starters:

http://www.surlytrader.com/volatility-selling-strategies/

http://www.surlytrader.com/picking-up-nickels-in-front-of-a-steamroller/

http://www.surlytrader.com/mitigating-gamma-losses/

http://www.surlytrader.com/gamma-hemorrhage/

Plus search ET for the multitudes of threads out there that have already covered this topic over and over.

And for god sakes stop selling this crap with VIX at 11.