Hello MarkBrown,@ES - Converting indicators which often seem useless into a trading model.

a.) it's the logic used to build the model not the indicators that make it successful.

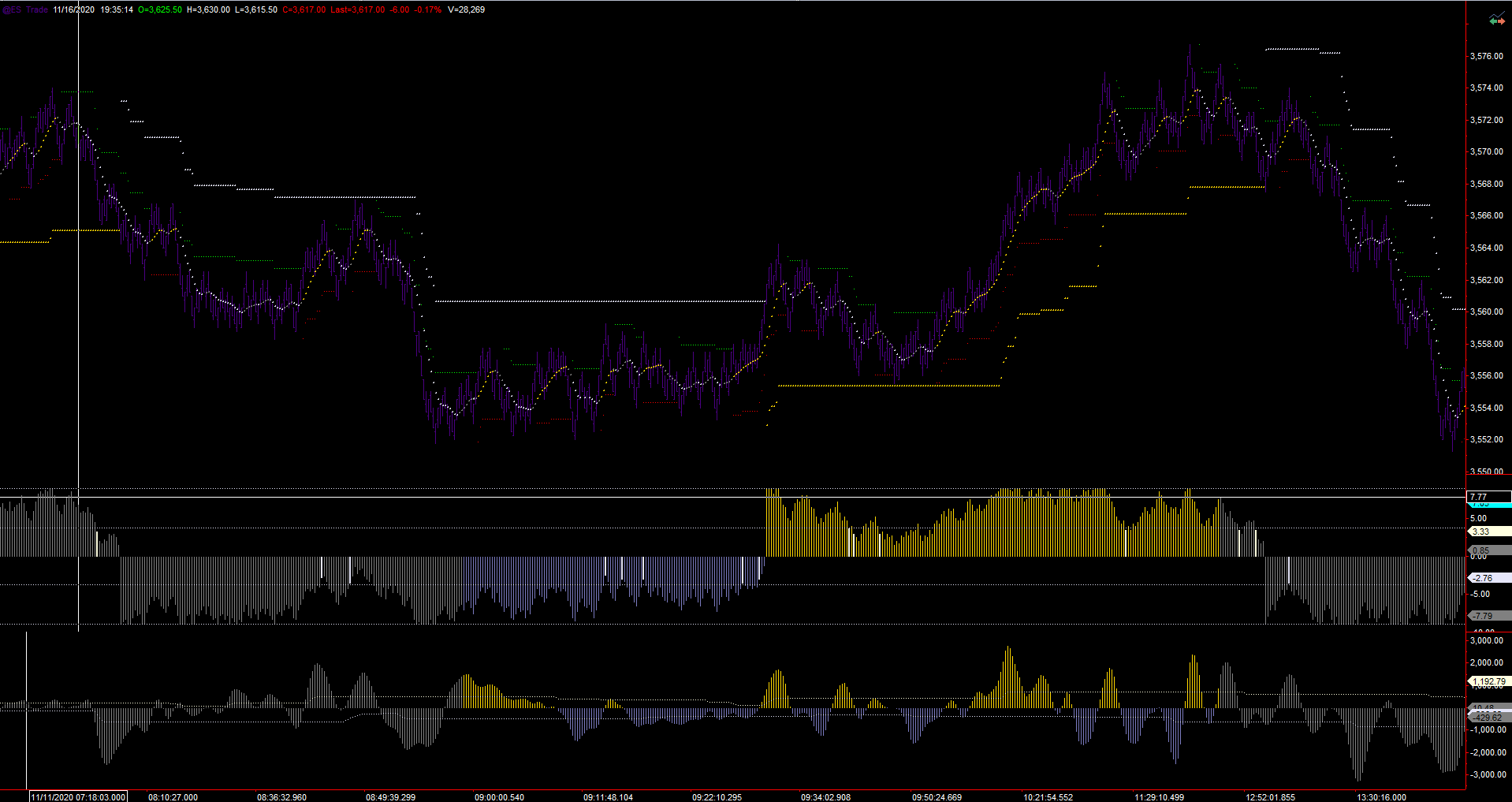

So it looks good but looks can be deceiving why not automated it?

a.) the human eye will mislead you to look for big moves, but chipping is more profitable.

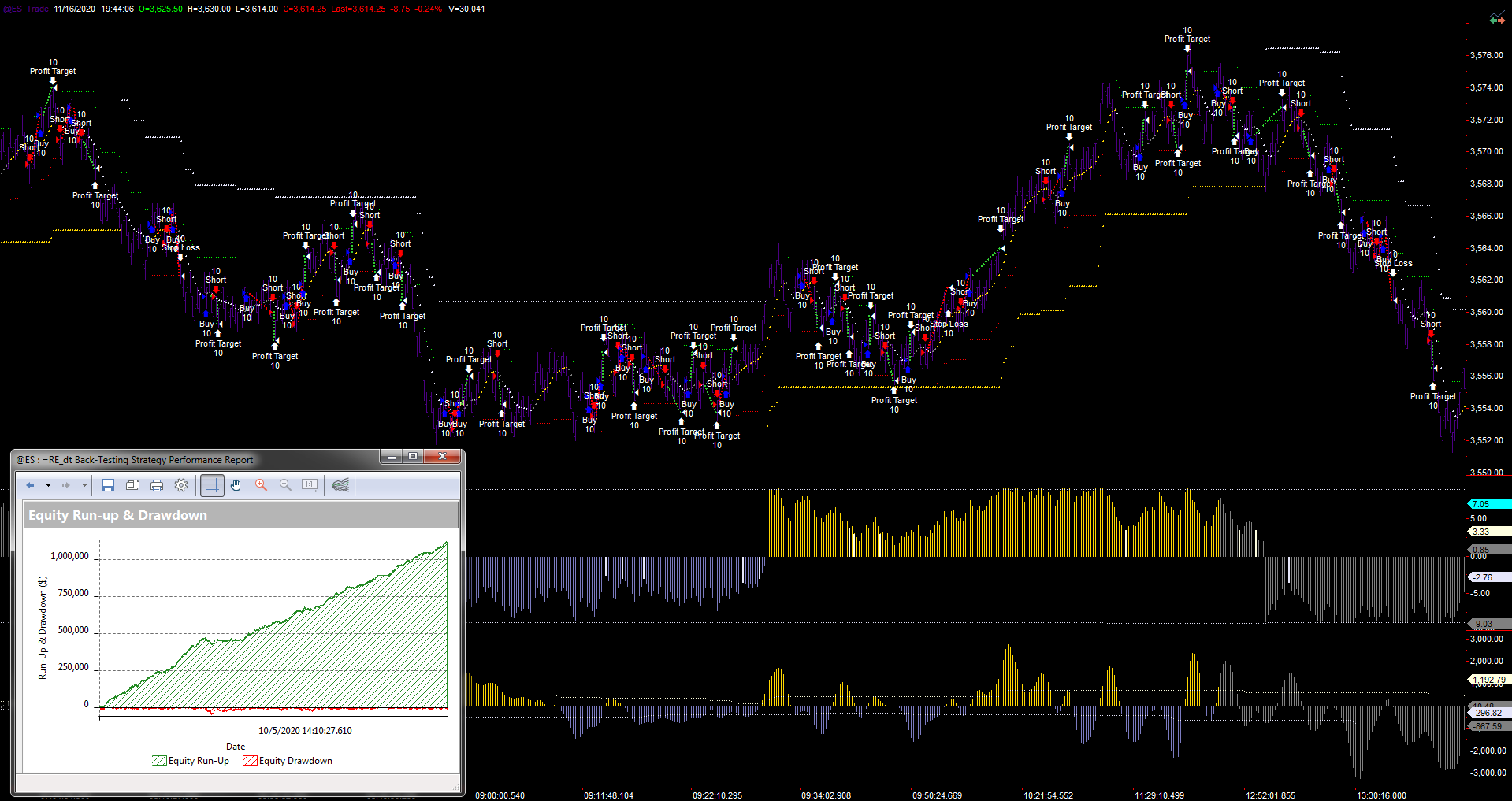

Based on fixed ratio starting with 1 ES and levering with no additional risk up to 10 contracts.

Only wins 57% of the time, run 24hrs a day non stop, 50k to 1,000,000. in 100 days.

1 to 2 risk reward - yes 200 risked for 100 made "embrace the risk" opposite of the norm.

Draw-down was less than 12%, so obviously I was disappointed with that. For years I tried incorporating reversion to the mean with trend trading and found it's better just to park when it's trending and capture the majority of the market action which is choppy action.

Happy to answer questions and give insights to building your own model. Mark

PS I have been running this system for over 15 years so it's not over over optimized, I just added the fixed ratio component to it otherwise it would have just made under 100k over the same 100 days.

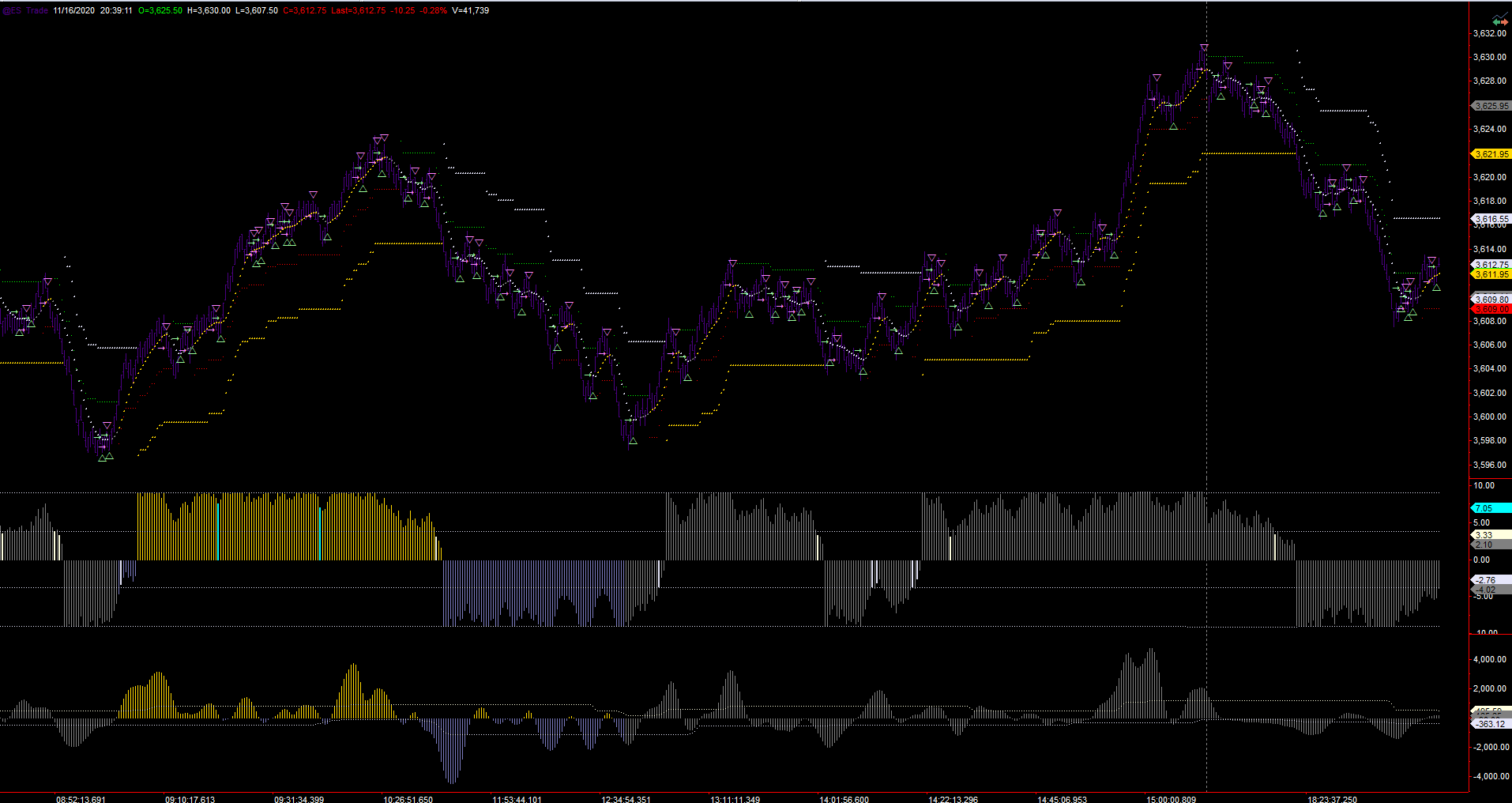

By contrast an always in model which incorporates both reversion to the mean and trending modes. Seems at first glance to make more money and it does but when you figure in the slippage and commissions of bidirectional trading you wind up with less. But it looks impressive to the eye.

Some of my wording may seem ignorant regarding algo development, so forgive me. Algo development and testing is something I have not done in about 2 years.

I have some questions for you please:

1. Did you back test the algo for historical years results? For example, did you run the algo from 2010-2019 to see the performance? I ask this because when I back test the algo I wrote and programmed, they all showed bad results.

2. Regarding algo development: From your experience, is it common to for alot of algo trading ideas to fail when programmed and then back test?

3. Regarding algo curve fitting and optimization: I read/heard that "over" optimization is a bad thing and will fail in the future trading of the algo. How much of the algo is optimized? Or was optimization even needed?

4. Regarding alo back and walk forward testing: Did you perform all your backtesting, optimization, walk forward testing, experimenting on a certain data set (like from 2010-2015)? And then tested that experimented/tuned algo from 2015-2020? I believe they call his in sample and out of sample data.

5. Is finding a profitable aglo challenging? What can share about the most difficult part of algo development?

6. Why do most algo developers fail at creating a consistent intraday algo?

Thank you sir.