Link

I refer to the combination of QE and ZIRP as QIRP. Both happened concurrently for the most part. It is hard to dis-aggregate the effect of one from the other. ZIRP has its impact from a mechanical perspective. QE has its impact from a psychological perspective – investors believe it drives asset prices up (primarily stocks), so investors then drive up asset prices.

Regardless, at this point the data is in. Asset prices have inflated (and systematic risk as well), but the economy has not. The economy has also missed every forecast the Fed had for it along the way when these policies were implemented. Further, QIRP is not working in Japan, even with the government buying equities. IF QIRP was going to increase inflation, Japan should be the place where it should at least create some inflation as they are huge net importers of commodities.

Consider the following statement from a prominent economist: “Japanese companies held Y236t or $2.0t of cash in 4Q — the same as the US corporate cash. Given continued increases in inflation expectations, it’s somewhat surprising that cash holdings by companies are still increasing.”

This is a very outdated notion that increased inflation expectations drive investment, especially if inflation is going from 0% to 2%. Frankly from any level a few % point change in inflation expectations is NOT enough to scare a business into an investment they wouldn’t otherwise make. Further as it pertains to the U.S., companies are holding cash as a matter of strategy — tax avoidance (loopholes re foreign tax dodges and other still not fixed), buybacks, and acquisitions, especially defensive acquisitions.

Keynes himself would not advocate what a lot of “Keynesians” view as proper policy today. His views (whether right or wrong) have been greatly distorted and they have morphed into something else in practice in today’s economy.

The focus on increasing inflation is overdone, outdated, myopic, and an excuse to take experimental policy action and stretch the Fed mandate (locally and globally).

Further now that it appears QIRP has been much less effective than anticipated for the economy, while increasing systematic risk, which makes it a net failure, Bernanke has taken to the blogosphere with transparent attempts to defend his decisions and legacy. Alan Greenspan seemed to often try and defend his legacy as well after his term as Fed chair ended.

“Although the recovery has not been as fast as hoped—in part because of “headwinds” arising from fiscal policy, the after-effects of the financial crisis, and other factors…”

Bernanke is saying he was right about everything, but everyone and everything else screwed it up. Hmmm. People that never admit they were wrong, blame others and other factors they didn’t consider but should have, never learn from their mistakes, and don’t evolve into being better at what they do. Janet Yellen fits this mold as well.

“The bottom line is that large increases in the short-term rate based on financial stability considerations alone would involve costs that well exceed the benefits……Initially, detractors focused on the supposed inflation risks of such policies. As time has passed with no sign of inflation, that critique now looks rather threadbare”

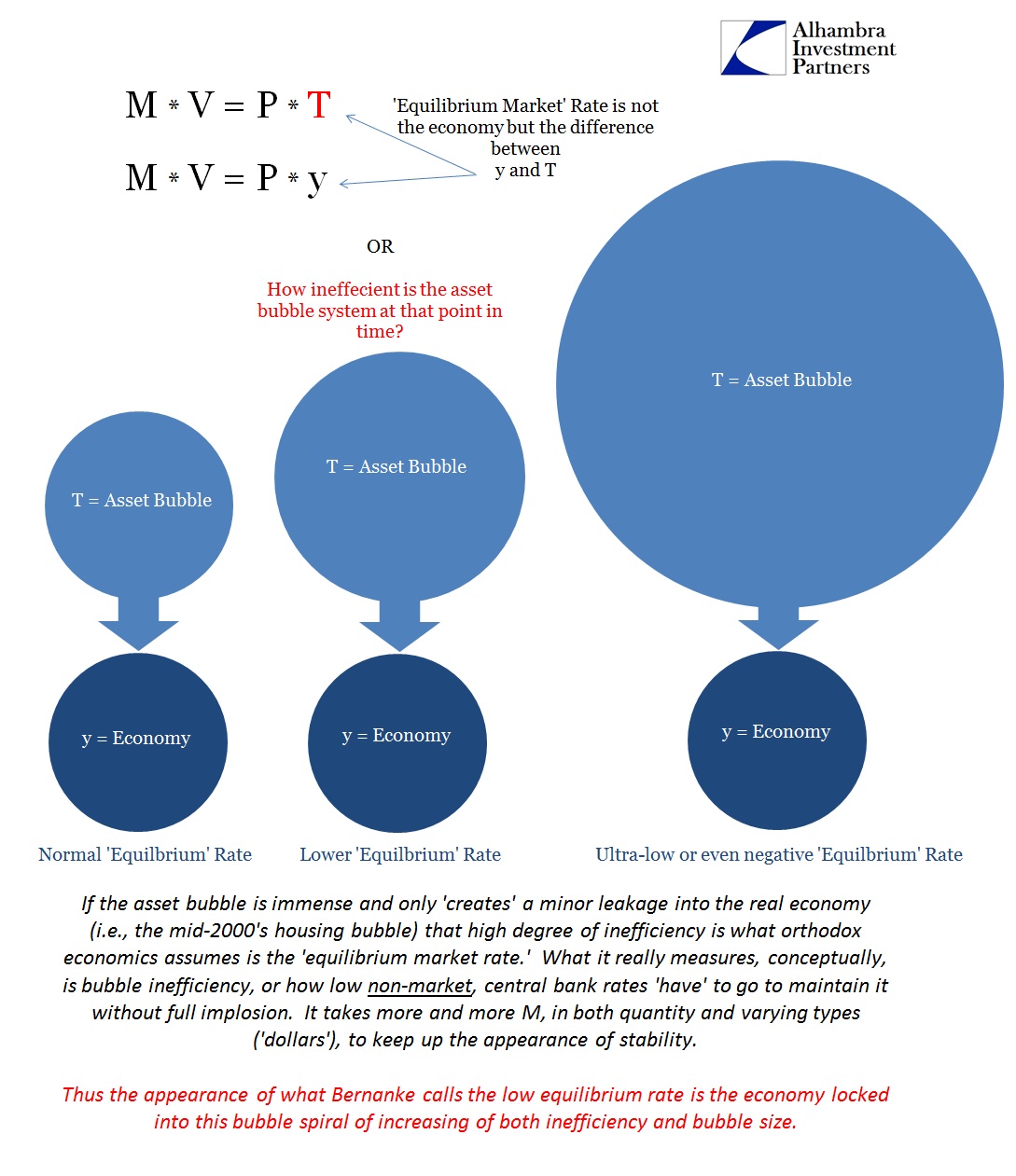

Makes sense, provided you assume, as the model he references does, that rate reductions have big effects on credit growth and economic growth. What if the effects on credit and economic growth were smaller than in the model? QE at least did not cause the credit growth that it was intended to. The increased money supply just ended up as excess reserves and the velocity of money slowed. That is why it wasn’t inflationary. Bernanke is now taking a victory lap because QE didn’t cause inflation. But that is only because QE didn’t do what he intended it to do. Then what if the costs (systemic risk) are greater than the model assumes? The costs of the last 2 bubbles blowing up was incalculably large. These models are all garbage in, garbage out. In my experience the Fed’s models recently appear to be good at one thing – being wrong!!!!

“If you asked the person in the street, “Why are interest rates so low?”, he or she would likely answer that the Fed is keeping them low. That’s true only in a very narrow sense. The Fed does, of course, set the benchmark nominal short-term interest rate. The Fed’s policies are also the primary determinant of inflation and inflation expectations over the longer term, and inflation trends affect interest rates, as the figure above shows. But what matters most for the economy is the real, or inflation-adjusted, interest rate (the market, or nominal, interest rate minus the inflation rate). The real interest rate is most relevant for capital investment decisions, for example. The Fed’s ability to affect real rates of return, especially longer-term real rates, is transitory and limited. Except in the short run, real interest rates are determined by a wide range of economic factors, including prospects for economic growth—not by the Fed…The Fed’s actions determine the money supply and thus short-term interest rates.”

BUT this is what he said on August 31, 2012 at that year’s Jackson Hole conference:

Then Bernanke also stated:

“This sounds very textbook-y, but failure to understand this point has led to some confused critiques of Fed policy. When I was chairman, more than one legislator accused me and my colleagues on the Fed’s policy-setting Federal Open Market Committee of “throwing seniors under the bus” (to use the words of one senator) by keeping interest rates low. The legislators were concerned about retirees living off their savings and able to obtain only very low rates of return on those savings.I was concerned about those seniors as well. But if the goal was for retirees to enjoy sustainably higher real returns, then the Fed’s raising interest rates prematurely would have been exactly the wrong thing to do. In the weak (but recovering) economy of the past few years, all indications are that the equilibrium real interest rate has been exceptionally low, probably negative.”

(cont'd below)

I refer to the combination of QE and ZIRP as QIRP. Both happened concurrently for the most part. It is hard to dis-aggregate the effect of one from the other. ZIRP has its impact from a mechanical perspective. QE has its impact from a psychological perspective – investors believe it drives asset prices up (primarily stocks), so investors then drive up asset prices.

Regardless, at this point the data is in. Asset prices have inflated (and systematic risk as well), but the economy has not. The economy has also missed every forecast the Fed had for it along the way when these policies were implemented. Further, QIRP is not working in Japan, even with the government buying equities. IF QIRP was going to increase inflation, Japan should be the place where it should at least create some inflation as they are huge net importers of commodities.

Consider the following statement from a prominent economist: “Japanese companies held Y236t or $2.0t of cash in 4Q — the same as the US corporate cash. Given continued increases in inflation expectations, it’s somewhat surprising that cash holdings by companies are still increasing.”

This is a very outdated notion that increased inflation expectations drive investment, especially if inflation is going from 0% to 2%. Frankly from any level a few % point change in inflation expectations is NOT enough to scare a business into an investment they wouldn’t otherwise make. Further as it pertains to the U.S., companies are holding cash as a matter of strategy — tax avoidance (loopholes re foreign tax dodges and other still not fixed), buybacks, and acquisitions, especially defensive acquisitions.

A little inflation is not the panacea for our economic problems and the Fed and others are over-focused on this notion and use it as an excuse for extreme policy flexibility.

Keynes himself would not advocate what a lot of “Keynesians” view as proper policy today. His views (whether right or wrong) have been greatly distorted and they have morphed into something else in practice in today’s economy.

The focus on increasing inflation is overdone, outdated, myopic, and an excuse to take experimental policy action and stretch the Fed mandate (locally and globally).

Further now that it appears QIRP has been much less effective than anticipated for the economy, while increasing systematic risk, which makes it a net failure, Bernanke has taken to the blogosphere with transparent attempts to defend his decisions and legacy. Alan Greenspan seemed to often try and defend his legacy as well after his term as Fed chair ended.

People only need to try and defend their legacy when they are insecure about it. I never noticed Paul Volcker trying to defend his legacy – the results of his decisions were pretty clear.

“Although the recovery has not been as fast as hoped—in part because of “headwinds” arising from fiscal policy, the after-effects of the financial crisis, and other factors…”

Bernanke is saying he was right about everything, but everyone and everything else screwed it up. Hmmm. People that never admit they were wrong, blame others and other factors they didn’t consider but should have, never learn from their mistakes, and don’t evolve into being better at what they do. Janet Yellen fits this mold as well.

“The bottom line is that large increases in the short-term rate based on financial stability considerations alone would involve costs that well exceed the benefits……Initially, detractors focused on the supposed inflation risks of such policies. As time has passed with no sign of inflation, that critique now looks rather threadbare”

Makes sense, provided you assume, as the model he references does, that rate reductions have big effects on credit growth and economic growth. What if the effects on credit and economic growth were smaller than in the model? QE at least did not cause the credit growth that it was intended to. The increased money supply just ended up as excess reserves and the velocity of money slowed. That is why it wasn’t inflationary. Bernanke is now taking a victory lap because QE didn’t cause inflation. But that is only because QE didn’t do what he intended it to do. Then what if the costs (systemic risk) are greater than the model assumes? The costs of the last 2 bubbles blowing up was incalculably large. These models are all garbage in, garbage out. In my experience the Fed’s models recently appear to be good at one thing – being wrong!!!!

“If you asked the person in the street, “Why are interest rates so low?”, he or she would likely answer that the Fed is keeping them low. That’s true only in a very narrow sense. The Fed does, of course, set the benchmark nominal short-term interest rate. The Fed’s policies are also the primary determinant of inflation and inflation expectations over the longer term, and inflation trends affect interest rates, as the figure above shows. But what matters most for the economy is the real, or inflation-adjusted, interest rate (the market, or nominal, interest rate minus the inflation rate). The real interest rate is most relevant for capital investment decisions, for example. The Fed’s ability to affect real rates of return, especially longer-term real rates, is transitory and limited. Except in the short run, real interest rates are determined by a wide range of economic factors, including prospects for economic growth—not by the Fed…The Fed’s actions determine the money supply and thus short-term interest rates.”

BUT this is what he said on August 31, 2012 at that year’s Jackson Hole conference:

“Generally, this research finds that the Federal Reserve’s large-scale purchases have significantly lowered long-term Treasury yields…

Then Bernanke also stated:

“This sounds very textbook-y, but failure to understand this point has led to some confused critiques of Fed policy. When I was chairman, more than one legislator accused me and my colleagues on the Fed’s policy-setting Federal Open Market Committee of “throwing seniors under the bus” (to use the words of one senator) by keeping interest rates low. The legislators were concerned about retirees living off their savings and able to obtain only very low rates of return on those savings.I was concerned about those seniors as well. But if the goal was for retirees to enjoy sustainably higher real returns, then the Fed’s raising interest rates prematurely would have been exactly the wrong thing to do. In the weak (but recovering) economy of the past few years, all indications are that the equilibrium real interest rate has been exceptionally low, probably negative.”

(cont'd below)

)

)