You mean in the same way that Penn Jillette said that the best way to become an atheist is to actually read the Bible?i wish more people read Von Mises.. and Hayak... Thomas Sowell is a great one to

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Public debt is not the issue — that's just a neo-con scare campaign

- Thread starter OddTrader

- Start date

We borrowed tons of money to support the same war.

Yes... and the only reason the U.S. economy boomed after the war is because we were the only country left with a manufacturing capability that was not bombed to shreds.

Right. (Also, inflation.) So high debt incurred by war does not necessarily mean you lose your empire. But at the time no one could know the high US debt load would be relieved.Yes... and the only reason the U.S. economy boomed after the war is because we were the only country left with a manufacturing capability that was not bombed to shreds.

Right. (Also, inflation.) So high debt incurred by war does not necessarily mean you lose your empire. But at the time no one could know the high US debt load would be relieved.

The British faced two wars where the high debt incurred in the war led to a financial crisis that impacted their capability to support their empire. The first was the Napoleonic Wars - the British managed to weather this storm and keep their empire. The second was WW2 - after which the British government was so broke they could no longer support colonies.

Of course there are a number of other factors in play including that the mercantile trade of the 1820s supported tea, opium, spices, sugar, etc. which meant the British colonies generated money, and the trade of the 1950s needed raw materials for modern manufacturing such as oil, metals, and rubber which the notable British colonies generally lacked.

so where did it come from?

It was already explained to you.

The British faced two wars where the high debt incurred in the war led to a financial crisis that impacted their capability to support their empire. The first was the Napoleonic Wars - the British managed to weather this storm and keep their empire. The second was WW2 - after which the British government was so broke they could no longer support colonies.

Of course there are a number of other factors in play including that the mercantile trade of the 1820s supported tea, opium, spices, sugar, etc. which meant the British colonies generated money, and the trade of the 1950s needed raw materials for modern manufacturing such as oil, metals, and rubber which the notable British colonies generally lacked.

The US had the benefit of fighting the war on other people's turf and they did not have to worry about rebuilding cities. In addition, the debt was made up of war bonds that were most held by US citizens so the money that was used to repay the debt was directly paid to Americans and funneled into the US economy.

People act like interest paid on debt is a total net loss to the government. As long as the interest is earned by the citizens of the country, its really not. Now if you are selling the debt the Chinese, thats a different story.

jem, are you listening?In addition, the debt was made up of war bonds that were most held by US citizens so the money that was used to repay the debt was directly paid to Americans and funneled into the US economy.

People act like interest paid on debt is a total net loss to the government. As long as the interest is earned by the citizens of the country, its really not. Now if you are selling the debt the Chinese, thats a different story.

yes... I was.. I gave it a thumbs up.

I have not harped on the Federal debt and borrowing since, I the I spent analyzing the govt shutdown and debt ceiling arguments and realized the Fed gives the orders for money printing not the govt.

When you realize that we have had 700 percent inflation the last 50 years while there was massive demand for the dollar (it should have gone up in value) you realize that massive inflation in the fact of strong demand, could have been caused by govt borrowing (which really should not cause general inflation... that is why a sovereign borrows instead of printing) ... the massive inflation has been caused by the Federal Reserve spreading trillions and trillions of dollars all over the world. Can you imagine the influence and the assets the private owners of the federal reserve must have purchased with those trillions.

So while I prefer no debt. its the progressive taxation and unlimited printing of the Federal Reserve which was the cancer on our standard of living.

In our economy focusing on Govt debt or Govt spending is like worrying about the pimple on top of basal cell carcinoma. Until we control of the cancer of unlimited private money creation ... worrying about the debt just plays into the the crony directed Kabuki.

I have not harped on the Federal debt and borrowing since, I the I spent analyzing the govt shutdown and debt ceiling arguments and realized the Fed gives the orders for money printing not the govt.

When you realize that we have had 700 percent inflation the last 50 years while there was massive demand for the dollar (it should have gone up in value) you realize that massive inflation in the fact of strong demand, could have been caused by govt borrowing (which really should not cause general inflation... that is why a sovereign borrows instead of printing) ... the massive inflation has been caused by the Federal Reserve spreading trillions and trillions of dollars all over the world. Can you imagine the influence and the assets the private owners of the federal reserve must have purchased with those trillions.

So while I prefer no debt. its the progressive taxation and unlimited printing of the Federal Reserve which was the cancer on our standard of living.

In our economy focusing on Govt debt or Govt spending is like worrying about the pimple on top of basal cell carcinoma. Until we control of the cancer of unlimited private money creation ... worrying about the debt just plays into the the crony directed Kabuki.

Last edited:

whatever, you could almost say the 1930's were a time when nobody wanted to borrow or lend. Then the only thing that changed in 1940 (besides Pearl Harbor and WWII) was people decided we need to borrow borrow borrow and spend spend spend. Other than that there was nothing fundamentally different from 1930 to 1940.It was already explained to you.

1950:

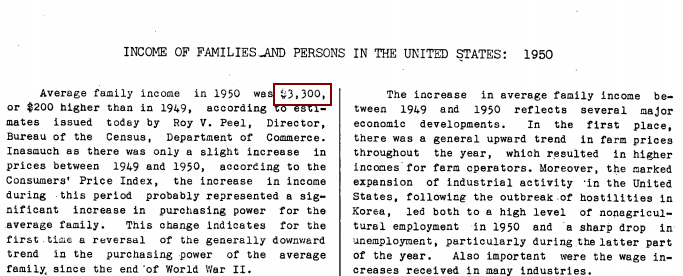

The average family income: $3,300

The average car cost: $1,510

The median home price: $7,354

2014: (Better quality car and much improved building in 2014)

The average family income: $51,017

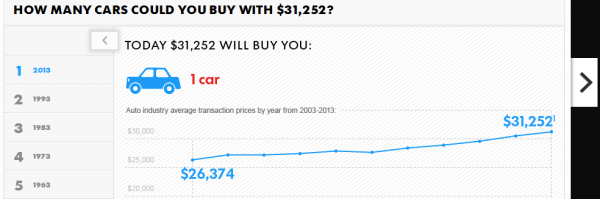

The average car cost: $31,252

The median home price: $188,900

The average family income: $3,300

The average car cost: $1,510

The median home price: $7,354

2014: (Better quality car and much improved building in 2014)

The average family income: $51,017

The average car cost: $31,252

The median home price: $188,900

http://www.mybudget360.com/cost-of-living-2014-inflation-1950-vs-2014-data-housing-cars-college/

Comparing the inflated cost of living today from 1950 to 2014: How declining purchasing power has hurt the middle class since 1950.

Inflation has a subtle eroding effect that impacts entire economies. In the United States, we have been fortunate to have relatively stable rates of inflation for two generations. Even in times of high inflation like the 1970s, people were able to adjust unlike places that experience uncontrolled inflation like Argentina is currently facing. Also, wages rose in tandem which helped buffer the pain of higher costs. Today however, inflation has eroded the purchasing power of the middle class. Only when we look at longer periods of time do we see the large impact inflation has on our ability to buy real goods and services. People found a piece comparing 1938 and 2013 prices on various goods and items to be enlightening. Since our middle class did not fully emerge until the end of World War II, it might be useful to compare the price of items back from 1950 to where things stand today. Has inflation had a big impact on our purchasing power since 1950?

1950 living versus that of 2014

It might be useful to first look at a few common items from 1950:

The average family income: $3,300

The average car cost: $1,510

The median home price: $7,354

These are three very important metrics when it comes to measuring purchasing power in the United States. Since we consider having a car and a home as cornerstones to a middle class lifestyle, it is useful to look at these figures since we can easily grab these figures from reliable sources.

See below for source data:

average family income

Source: US Department of Commerce

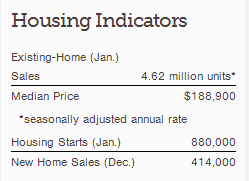

Then we can see the median home price:

1950 price of homes

Source: US Census

A Ford car could be had with a price range of $1,339 to $2,262 depending on the model. Income is an important measure because it gives us an insight into how well families are doing and how much money is being spent on certain items. So let us derive ratios for each of the items for the 1950s:

Home price / income = 2.2

Car cost / income = .45

This is important here. The typical home cost 2.2 times annual income while a car cost .45 times annual income. Let us now fast forward to 2014 and see where these things stand:

The average family income: $51,017

The average car cost: $31,252

The median home price: $188,900

Let us show the data here:

Source: National Association of Realtors

Household income was pulled from Census data based on what the typical household earns. Inflation has a subtle way of eroding purchasing power. Let us pull some ratios here:

Home price / income = 3.7

Car cost / income = .61

Housing has gotten dramatically more expensive. The cost of a new car has gone up but not so noticeably when looking at inflation data. Inflation has largely eaten away at income on other fronts like college tuition and healthcare. These were much more affordable back in the 1950s relative to overall income.

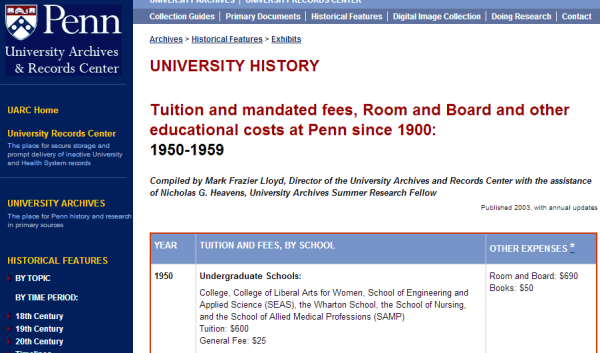

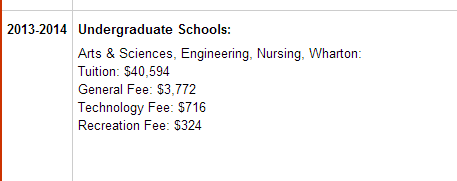

For example, in 1950 at the University of Pennsylvania annual tuition was $600:

We should run a ratio here as well:

Tuition / income = .18

Let us look at current tuition costs:

Current tuition is over $40,000 per year.

Tuition / income = .79

This is a massive change. In 1950, a family sending their child to the University of Pennsylvania would only spend 18 percent of their annual income (if they paid in cash) to send their kid to study. Today it would consume 79 percent of gross annual income. Even if we look at net take home pay a regular family in no way could send their child to school without going into massive student debt.

A good portion of inflation over this time has been masked by massive amounts of debt and financing. Car purchases, mortgages, and college are now financed long-term. Low rates have masked this erosion but with rates reaching the lower bound of the range, the pain of inflation is now being felt by many households.

Last edited: