Hello,

Some time ago I wrote the article “Pair trading died - hello massive trading”

From then, I changed the trading model, collected good quality data, that can be used as a proof of concept for the algorithm (Nasdaq Basic Feed ticks). Data collector used C API and developed on C++. It is required that we host a server next to where we are trading, and a rack cross connected to the market data provider as well as the exchange to give us an optimal edge in entries / exits (NYSE). This is a continuing project and a little more work from another Quant / Support and Development Funding is required to release this algorithm to the live environment, but the base of algo made already.

The algorithm calculates best possible basket from all USA stocks and the base idea is to be a market maker holding a major basket. We use 100 top USA stocks from SP500 index by capitalization. We than create a market neutral composite and then trade it with a lower risk intraday without holding the positions after the market close.

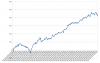

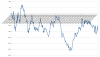

I enclosed pictures with PnL. In this example we use $250,000 USD as trading capital and 0.003 per share fee. I know that it’s possible to get a better fee if we work with exchanges directly as market maker, and this will be our target once we start live trading. As you can see, in the first hour we calculate the model’s variable and then apply it for trading. This is not “in sample holy grail”. Pure mathematics are put to operation without the use of ML/AI etc. My opinion and experience show that ML/AI can’t pass cross validation.

About running this algorithm live: I’m not sure that it’s possible to execute this live via IB or another retail trading platform that supports API. The algorithm will need extensive work with limit orders and exchange report info. We have tested a 101-stock basket and it generated 65-70 million in volume daily for $250,000 trading capital. It’s even possible to use 250-300 stocks and 10-25M trading capital volume of market data, report info and limit order management will crash any retails platform.

Now we are looking possibility continue research and development work with a private or small hedge fund team. Head office place is in Australia and another team Europe. Our team has over 10 years algorithmic trading experience specializing in high frequency trading and quantitative ideas.

As this is one of the highest forms of intelligent black box algorithms expenses must be considered. Expenses to consider: Development Expenses, Management Expenses, Support Expenses, Server Expenses, Market data Expenses. A rough estimate of expenses may vary from $25,000 on-ward.

Regards,

Eugene.

PS. Enclosed 3 screens for 100 stock basket and sample with 5 stocks basket - as you can see algo unstable for 5 stocks model.

Some time ago I wrote the article “Pair trading died - hello massive trading”

From then, I changed the trading model, collected good quality data, that can be used as a proof of concept for the algorithm (Nasdaq Basic Feed ticks). Data collector used C API and developed on C++. It is required that we host a server next to where we are trading, and a rack cross connected to the market data provider as well as the exchange to give us an optimal edge in entries / exits (NYSE). This is a continuing project and a little more work from another Quant / Support and Development Funding is required to release this algorithm to the live environment, but the base of algo made already.

The algorithm calculates best possible basket from all USA stocks and the base idea is to be a market maker holding a major basket. We use 100 top USA stocks from SP500 index by capitalization. We than create a market neutral composite and then trade it with a lower risk intraday without holding the positions after the market close.

I enclosed pictures with PnL. In this example we use $250,000 USD as trading capital and 0.003 per share fee. I know that it’s possible to get a better fee if we work with exchanges directly as market maker, and this will be our target once we start live trading. As you can see, in the first hour we calculate the model’s variable and then apply it for trading. This is not “in sample holy grail”. Pure mathematics are put to operation without the use of ML/AI etc. My opinion and experience show that ML/AI can’t pass cross validation.

About running this algorithm live: I’m not sure that it’s possible to execute this live via IB or another retail trading platform that supports API. The algorithm will need extensive work with limit orders and exchange report info. We have tested a 101-stock basket and it generated 65-70 million in volume daily for $250,000 trading capital. It’s even possible to use 250-300 stocks and 10-25M trading capital volume of market data, report info and limit order management will crash any retails platform.

Now we are looking possibility continue research and development work with a private or small hedge fund team. Head office place is in Australia and another team Europe. Our team has over 10 years algorithmic trading experience specializing in high frequency trading and quantitative ideas.

As this is one of the highest forms of intelligent black box algorithms expenses must be considered. Expenses to consider: Development Expenses, Management Expenses, Support Expenses, Server Expenses, Market data Expenses. A rough estimate of expenses may vary from $25,000 on-ward.

Regards,

Eugene.

PS. Enclosed 3 screens for 100 stock basket and sample with 5 stocks basket - as you can see algo unstable for 5 stocks model.

")