You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Options portfolio risk management resources

- Thread starter tonyf

- Start date

Risk management comes from managing your greeks.

Your greeks are additive for each underlying, except theta, which (as dollars/day) is additive across the entire portfolio.

So, add 'greeks' management, and 'portfolio' management, to your search.

And memorize those greeks' graphs, for OTM, ATM, and ITM...

Your greeks are additive for each underlying, except theta, which (as dollars/day) is additive across the entire portfolio.

So, add 'greeks' management, and 'portfolio' management, to your search.

And memorize those greeks' graphs, for OTM, ATM, and ITM...

Risk management comes from managing your greeks.

Your greeks are additive for each underlying, except theta, which (as dollars/day) is additive across the entire portfolio.

So, add 'greeks' management, and 'portfolio' management, to your search.

And memorize those greeks' graphs, for OTM, ATM, and ITM...

Thanks for that. To frame my question, it is assignment risk I am concerned about.

Matt_ORATS

Sponsor

Do you have ideas on how to show assignment risk? We are adding a Risk section to our Wheel.orats.com trading site.Thanks for that. To frame my question, it is assignment risk I am concerned about.

Do you have ideas on how to show assignment risk? We are adding a Risk section to our Wheel.orats.com trading site.

At the asset level I use a bunch of metrics to assess probability.

A different story at portfolio level where cross-correlation plays an important role.

Can you tell me more of what you do?

Matt_ORATS

Sponsor

My firm, ORATS, has a trading application. We currently have backtesting, scanning, and charting. We are adding risk and the ability to send trades to brokerages via APIs, starting with Tradier.

I was a Cboe independent market maker and backed many traders so I have experience in risk.

ORATS has metrics that can help in risk management including:

We will bring these metrics and more to bear in our risk section.

I was curious about assignment risk metrics. Assignment/early exercise usually happens to capture a dividend and ORATS has a popular dividend feed in the industry, so that can be used.

I was a Cboe independent market maker and backed many traders so I have experience in risk.

ORATS has metrics that can help in risk management including:

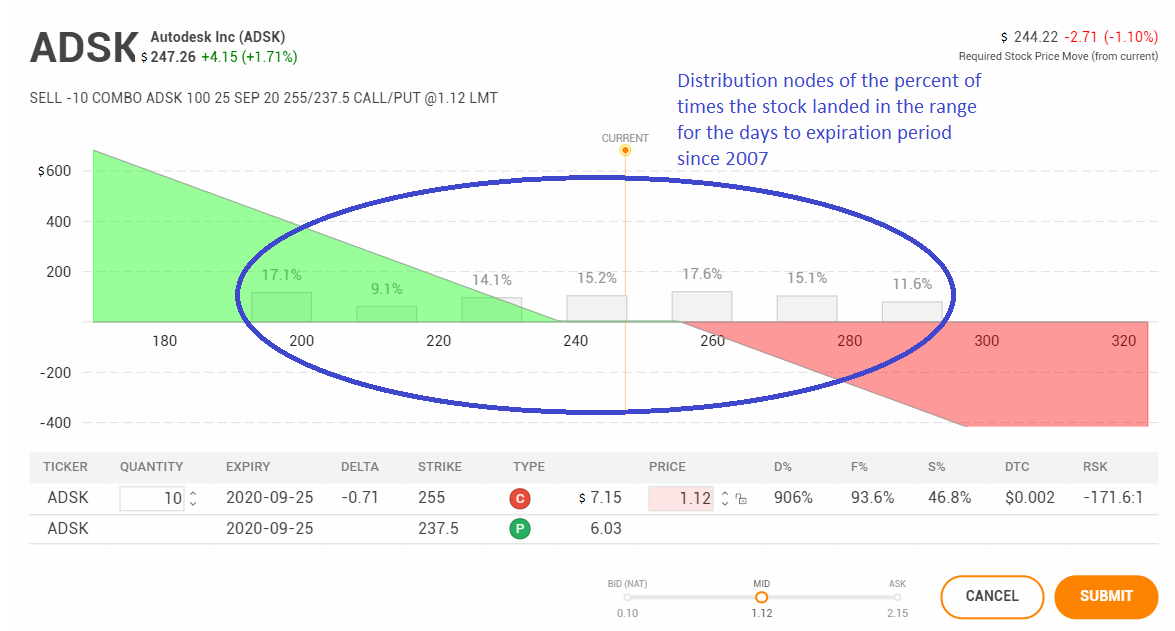

- Distribution analysis of historical stock returns as in this payoff picture overlay:

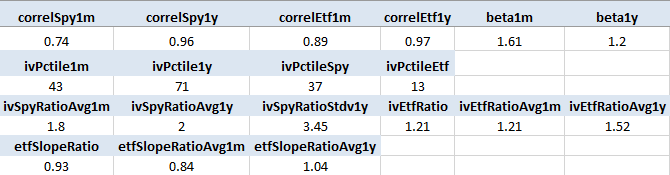

- Correlation and Beta, IV percentile and Slope (skewness) and how they relate to SPY and the best ETF for the ticker. Here ADSK best ETF is XLK.

We will bring these metrics and more to bear in our risk section.

I was curious about assignment risk metrics. Assignment/early exercise usually happens to capture a dividend and ORATS has a popular dividend feed in the industry, so that can be used.

My firm, ORATS, has a trading application. We currently have backtesting, scanning, and charting. We are adding risk and the ability to send trades to brokerages via APIs, starting with Tradier.

I was a Cboe independent market maker and backed many traders so I have experience in risk.

ORATS has metrics that can help in risk management including:

- Distribution analysis of historical stock returns as in this payoff picture overlay:

- Correlation and Beta, IV percentile and Slope (skewness) and how they relate to SPY and the best ETF for the ticker. Here ADSK best ETF is XLK.

We will bring these metrics and more to bear in our risk section.

I was curious about assignment risk metrics. Assignment/early exercise usually happens to capture a dividend and ORATS has a popular dividend feed in the industry, so that can be used.

Interesting - good stuff.

Blackswaning (crash testing) a portfolio is equaly interesting in my view if you have $s to spend on further development i.e. phased assignment v.s. bulk assignment.

Matt_ORATS

Sponsor

Yes, showing large moves like 40% or +- 3 standard deviation moves at the option, ticker, best ETF, and the entire portfolio together is interesting to me. You can look at that simply adding all the returns at the nodes in standard deviation moves of all the tickers modelling correlation going to 1. You can also model using betas or correlations.Interesting - good stuff.

Blackswaning (crash testing) a portfolio is equaly interesting in my view if you have $s to spend on further development i.e. phased assignment v.s. bulk assignment.

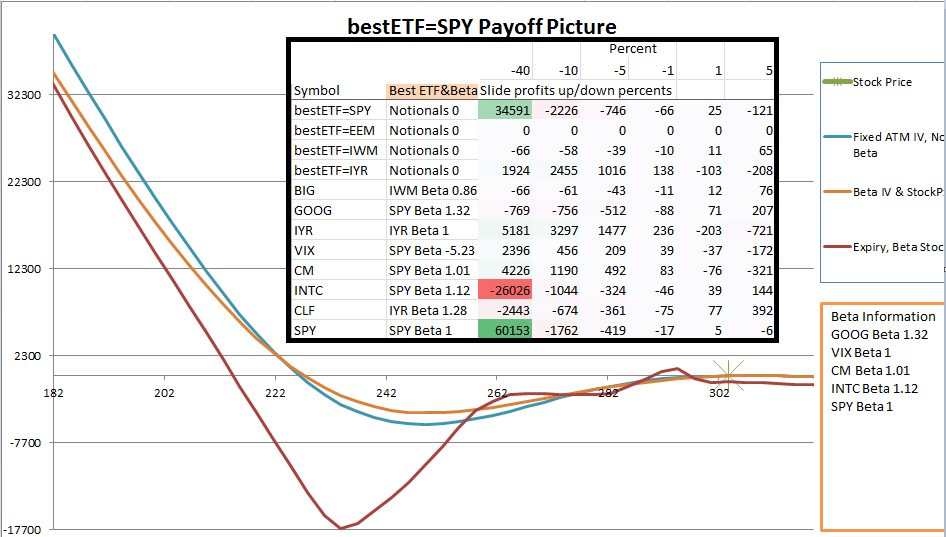

For example, here is a position break down by best ETF and simply adding all positions into SPY. VIX is in the list and has a large negative beta so that picture would be best with a beta weighting selected rather than simple summing.

You can check some assignment risk on individual positions by looking at arbitrage opportunities around exercise. Bid less than intrinsic value -> holders can’t sell for a fair value -> holders may exercise to exit the position. Put price less than call extrinsic value -> holders will exercise to capture dividends.