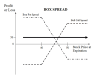

Today I was thinking, If I bought a delta 1.0 Call, sold an OTM call.(bull debit vertical) At at the same buy a 1.0 delta Put, sold an OTM put, (put debit vertical), I end up with a risk free trade and collect the premium for both short contracts... I did the risk analysis in TOS and I'm seeing a horizontal line above zero, with a profit of 4.29.... or 10% in 10 days with this particular spread, "risk free"....

After doing some digging, I learned this is called a box spread. I also saw some info on reversals. Can any knowledgable traders share their insight with these strategies, and maybe what I am missing? This obviously sounds too good to be true. Really appreciate the responses.

After doing some digging, I learned this is called a box spread. I also saw some info on reversals. Can any knowledgable traders share their insight with these strategies, and maybe what I am missing? This obviously sounds too good to be true. Really appreciate the responses.

Last edited:

")