When Domenico Colombo saw that his monthly mortgage payment was about to balloon by 30 percent, he had a clear picture of how bad it could get.

His payment was scheduled to surge by an extra $1,500 in December. With his daughter headed to college next fall and tuition to be paid, he feared ending up like so many neighbors in Fort Lauderdale, Fla., who defaulted on their mortgages and whose homes are now in foreclosure and sporting "For Sale" signs.

Colombo did manage to renegotiate a new fixed interest rate loan with his bank, and now believes he'll be OK -- but the future is less certain for the rest of us.

In the months ahead, millions of other adjustable-rate mortgages like Colombo's will reset, giving them a higher interest rate as required by the loan agreements and leaving many homeowners unable to make their payments. Soaring mortgage default rates this year already have shaken major financial institutions and the fallout from more of them, some experts say, could spread from those already battered banks into the general economy.

The worst-case scenario is anyone's guess, but some believe it could become very bad.

"We haven't faced a downturn like this since the Depression," said Bill Gross, chief investment officer of PIMCO, the world's biggest bond fund. He's not suggesting anything like those terrible times -- but, as an expert on the global credit crisis, he speaks with authority.

"Its effect on consumption, its effect on future lending attitudes, could bring us close to the zero line in terms of economic growth," he said. "It does keep me up at night."

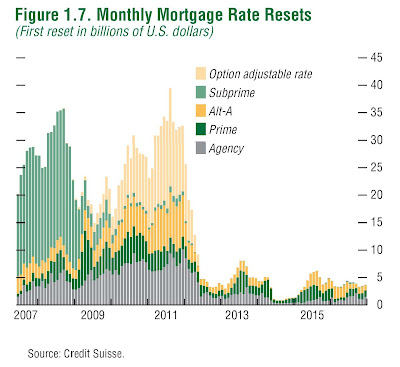

Some 2 million homeowners hold $600 billion of subprime adjustable-rate mortgage loans, known as ARMs, that are due to reset at higher amounts during the next eight months. Subprime loans are those made to people with poor credit. Not all these mortgages are in trouble, but homeowners who default or fall behind on payments could cause an economic shock of a type never seen before.

Some of the nation's leading economic minds lay out a scenario that is frightening. Not only would the next wave of the mortgage crisis force people out of their homes, it might also spiral throughout the economy.

http://biz.yahoo.com/ap/071124/doomsday_scenario.html

His payment was scheduled to surge by an extra $1,500 in December. With his daughter headed to college next fall and tuition to be paid, he feared ending up like so many neighbors in Fort Lauderdale, Fla., who defaulted on their mortgages and whose homes are now in foreclosure and sporting "For Sale" signs.

Colombo did manage to renegotiate a new fixed interest rate loan with his bank, and now believes he'll be OK -- but the future is less certain for the rest of us.

In the months ahead, millions of other adjustable-rate mortgages like Colombo's will reset, giving them a higher interest rate as required by the loan agreements and leaving many homeowners unable to make their payments. Soaring mortgage default rates this year already have shaken major financial institutions and the fallout from more of them, some experts say, could spread from those already battered banks into the general economy.

The worst-case scenario is anyone's guess, but some believe it could become very bad.

"We haven't faced a downturn like this since the Depression," said Bill Gross, chief investment officer of PIMCO, the world's biggest bond fund. He's not suggesting anything like those terrible times -- but, as an expert on the global credit crisis, he speaks with authority.

"Its effect on consumption, its effect on future lending attitudes, could bring us close to the zero line in terms of economic growth," he said. "It does keep me up at night."

Some 2 million homeowners hold $600 billion of subprime adjustable-rate mortgage loans, known as ARMs, that are due to reset at higher amounts during the next eight months. Subprime loans are those made to people with poor credit. Not all these mortgages are in trouble, but homeowners who default or fall behind on payments could cause an economic shock of a type never seen before.

Some of the nation's leading economic minds lay out a scenario that is frightening. Not only would the next wave of the mortgage crisis force people out of their homes, it might also spiral throughout the economy.

http://biz.yahoo.com/ap/071124/doomsday_scenario.html

")