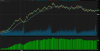

The question becomes, using 400K from 2012 - 2016 resulted in 420K, what would happen if you deployed the 400K in one day on a simple EMA system with a extreme discretionary bias. One contract per 10K, 40 contracts. Trading only 1 week out of the possible 260 weeks.

60K in one week on 400K....

What if you could identify other weeks with similar discretion out of those 260 weeks. The most amount of money can be made in the shortest period of time if you have the ability to identify market catalyzing events/periods using leverage. The EMA system is constantly on after entry to exit.