You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Micro Structure

- Thread starter dartmus

- Start date

Last edited:

The new micro structure is the trading between exchanges. Chicago and New York. Futures in Illinois and stocks in NYC. The exchanges are linked via microwave radio towers that transmit data at 99% the speed of light. Retail is clueless that this has become the entire basis for the market.

Net chat about this topic

https://news.ycombinator.com/item?id=19354341

Net chat about this topic

https://news.ycombinator.com/item?id=19354341

Last edited:

From an economics perspective, micro-structure is the straw man you raise in order to violate the Efficient Markets Hypothesis with relative impunity.

With a perfect market (infinite numbers of voluntary buyers and sellers, none of whom are large enough to affect price; instantaneous and costless transmission of complete information to all; costless trades...), there can be no effect like having the market bid down a selling price because of one individual's desire to sell. As soon as you allow for "size" to matter (whether the trade or the total transacted in some given time), you can have 'market effects' manifest. "Great!" Yeah -- this is the type of stuff that we have to deal with every day, but you need that little imperfection ("Size matters!"

Yeah -- this is the type of stuff that we have to deal with every day, but you need that little imperfection ("Size matters!"  ) to better approach the real world.

) to better approach the real world.

So when an academic approaches financial markets, things are pretty boring with ol' EMH at work. To study the interesting stuff -- to *start* asking interesting questions, you have to start disfiguring the EMH into "strong-form" or "semi-strong-form" or....

To study the interesting stuff -- to *start* asking interesting questions, you have to start disfiguring the EMH into "strong-form" or "semi-strong-form" or....  That fun MICRO-STRUCTURE is what allows/allowed Behavioral Finance (back) into the Business School. (That, and a Nobel for Kahneman & Tversky no doubt...

That fun MICRO-STRUCTURE is what allows/allowed Behavioral Finance (back) into the Business School. (That, and a Nobel for Kahneman & Tversky no doubt... )

)

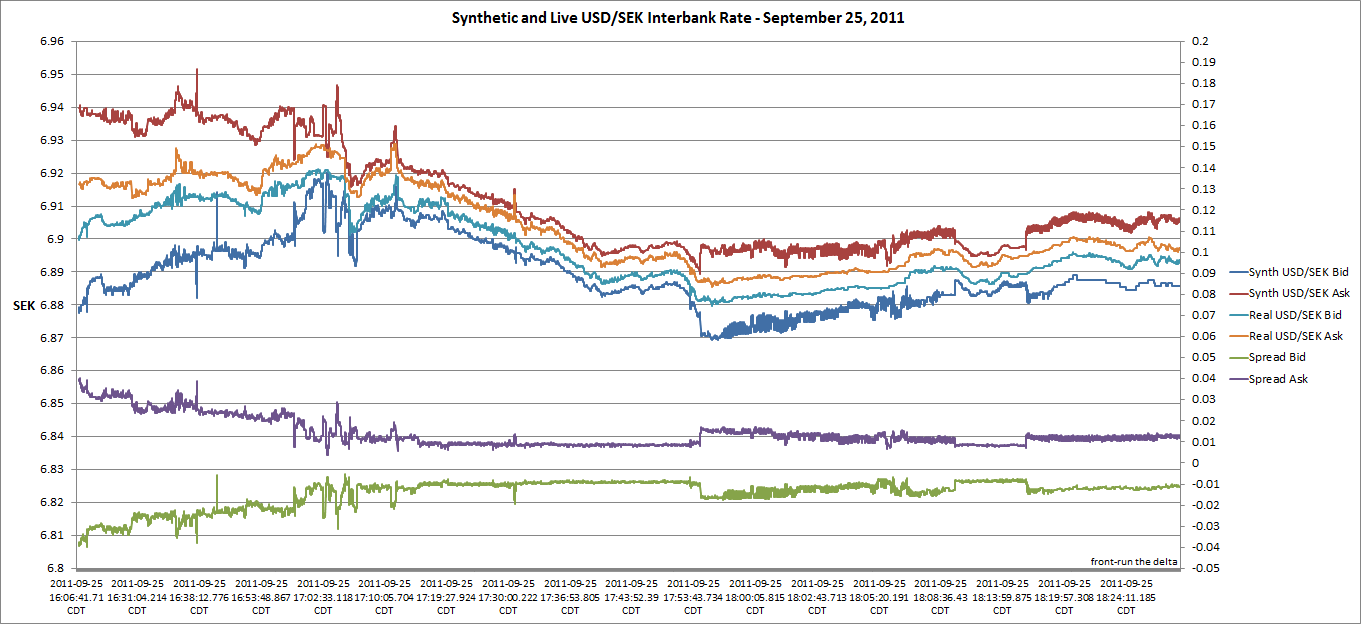

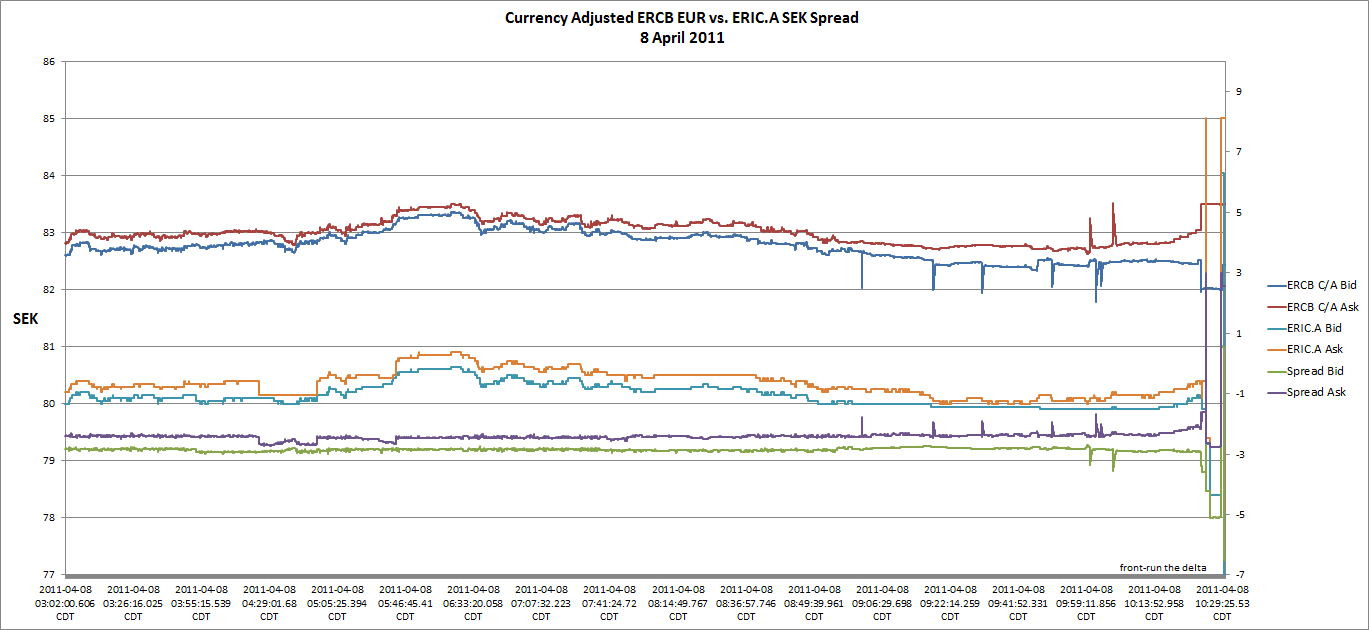

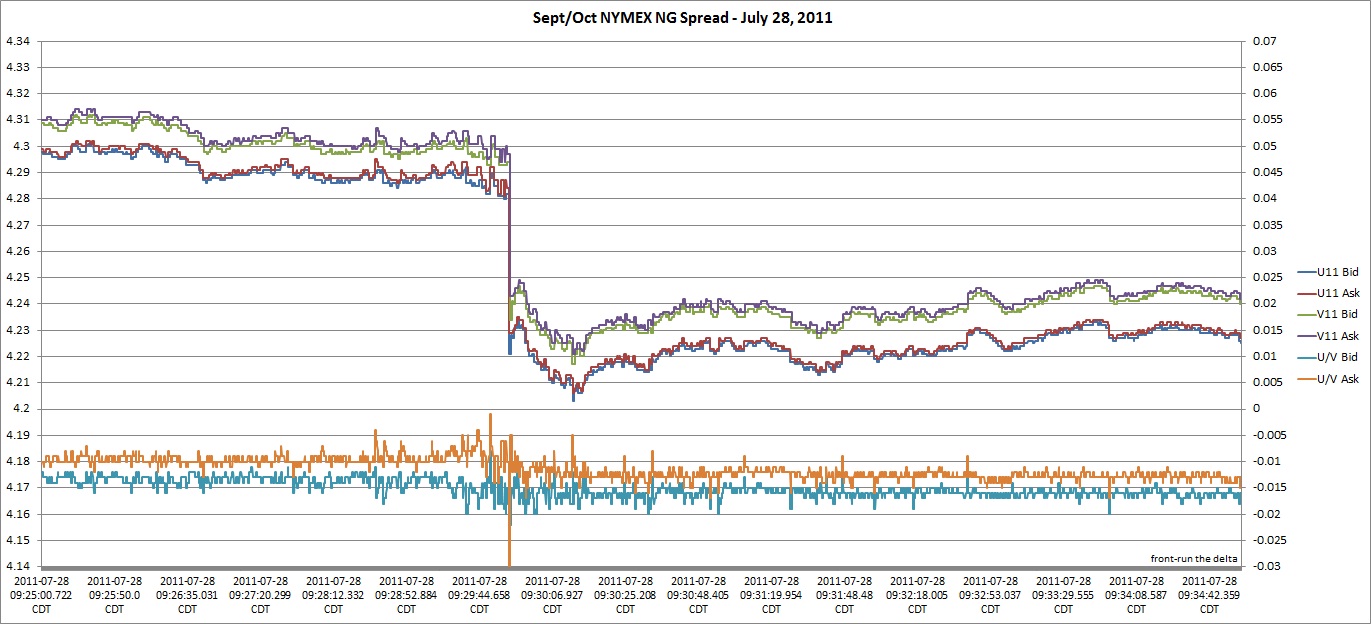

So if you're going through a faculty listing and see "Micro-Structure" as an area of interest, think "Size matters" and remember the little graphs in the ET posts above this one, where time, speed, total volume, trade volume -- all of that stuff that makes a market -- it all steps away from costlessness and infinitely supplied/purchased.

If Kris Kristofferson was a trader, he would've written...

"Liquidity's jus' another word for... effi-ci-ent mar-kets

Markets don't mean nuthin' baby if they ain't free-eeee

and

Trading be-tween Bid & Ask was... all we need to do-oooo-ooo

Vigs were good -- yeah good enough for me-eee-eeee

Good enough for me and my Bobby McGee-eeeee-eeee-eee"

With a perfect market (infinite numbers of voluntary buyers and sellers, none of whom are large enough to affect price; instantaneous and costless transmission of complete information to all; costless trades...), there can be no effect like having the market bid down a selling price because of one individual's desire to sell. As soon as you allow for "size" to matter (whether the trade or the total transacted in some given time), you can have 'market effects' manifest. "Great!"

Yeah -- this is the type of stuff that we have to deal with every day, but you need that little imperfection ("Size matters!" ) to better approach the real world.So when an academic approaches financial markets, things are pretty boring with ol' EMH at work.

To study the interesting stuff -- to *start* asking interesting questions, you have to start disfiguring the EMH into "strong-form" or "semi-strong-form" or.... That fun MICRO-STRUCTURE is what allows/allowed Behavioral Finance (back) into the Business School. (That, and a Nobel for Kahneman & Tversky no doubt...)So if you're going through a faculty listing and see "Micro-Structure" as an area of interest, think "Size matters" and remember the little graphs in the ET posts above this one, where time, speed, total volume, trade volume -- all of that stuff that makes a market -- it all steps away from costlessness and infinitely supplied/purchased.

If Kris Kristofferson was a trader, he would've written...

"Liquidity's jus' another word for... effi-ci-ent mar-kets

Markets don't mean nuthin' baby if they ain't free-eeee

and

Trading be-tween Bid & Ask was... all we need to do-oooo-ooo

Vigs were good -- yeah good enough for me-eee-eeee

Good enough for me and my Bobby McGee-eeeee-eeee-eee"

Last edited: