Hi Matt,You can recreate this spread in FEZ in our Wheel online product.

If the strikes were about -1 call at 95.7% of euro stoxx and + 2 calls x 101.8% of the stock price that translates to about the 45/48 FEZ call backspread diagonal.

The $45 strike IV is 21.3% and has a 84 delta

$48 IV is 14.8% and 39 delta

The spread is short 6 delta.

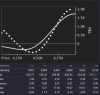

In our Chain you can simulate the trade and get a payoff diagram. Since this has a calendar aspect, we value the terminal value as the Aug 20 date. At that point, the Sep 17 residual value of the calls are valued at their volatility and added to the terminal value of the expired Aug call giving the payoff below.

Detailing the value at the current stock price and the worst case for the spread at $48:

So the trade gets a credit of $110 and the trade break evens are $46.70 -1% and $49.1 +4.1% and max loss is stock at $48 or -$32.

We analyze the valuation from a few perspectives:

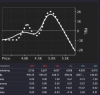

- Distribution % based on historical stock price movements times the terminal value at the shorter expiration give a valuation about equal to the price.

- Forecast % based on historical volatility and skew give a value of -12.3% against.

The trade benefits from a steep put-call skew, now in the 95th percentile.

The data API Monies endpoint shows the IV surface by delta and expiration.

The trade looks good from a payoff perspective, but the euro stoxx tends to stay within the range of stock price where the trade does not work, at least looking at the historical distribution.

Interesting analysis. Can you do the same for the last strategy of the article, i.e. the one they consider as bullish play? It would be interesting to see the conclusions.