Prominent market scholars have delved into the cyclical behavior of stock markets, emphasizing the significance of grasping asset seasonality. In this article, we will explore how to identify seasonal patterns using Python.

What is a seasonal pattern? According to José Martínez, a seasonal pattern pertains to the market behavior of specific assets within a particular time frame. For instance, commodities like soy, wheat, and oil are influenced by climatic conditions.

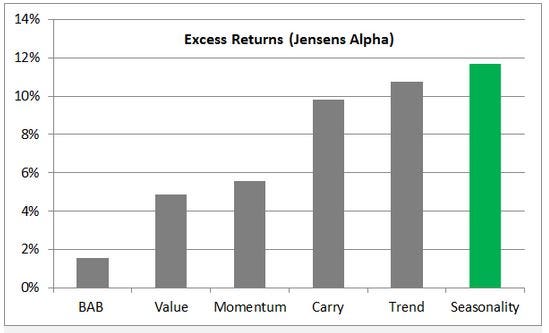

Do other financial assets respond to seasonal patterns? Yes, seasonal patterns can correlate with regular events such as employment data, stock levels, or consumption. Dimitri Speck has demonstrated that seasonality outperforms other investment strategies.

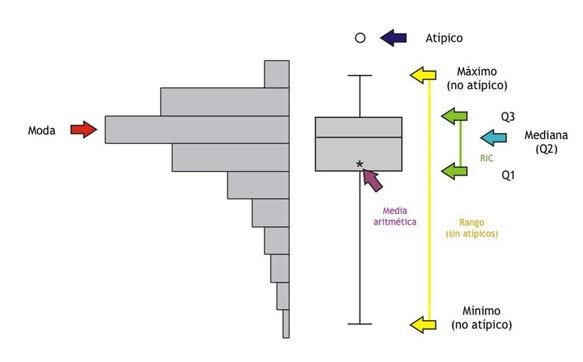

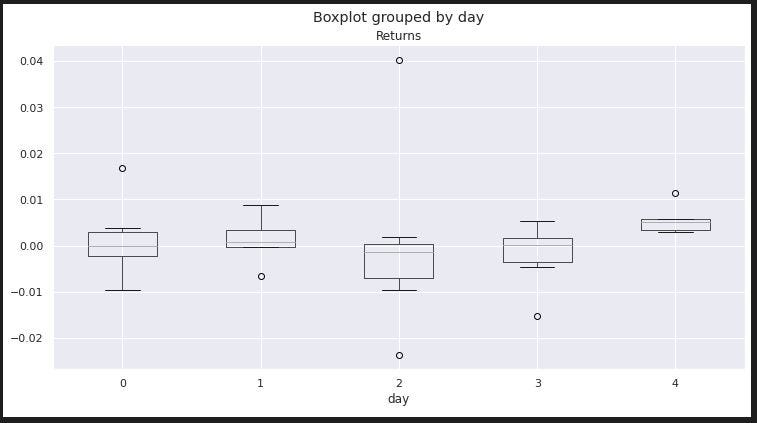

To analyze this, we employ quartiles and a box and whisker plot, statistical tools. Quartiles divide data into four parts, while the box and whisker plot visually displays the median and quartiles.

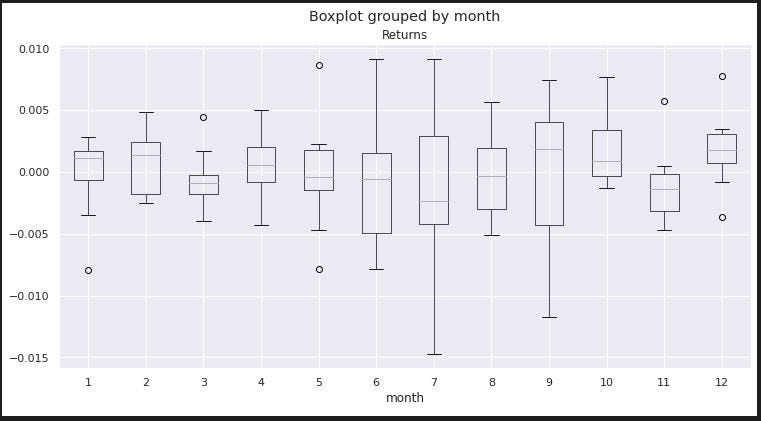

We apply these tools to Corn contract data, uncovering seasonal patterns in returns. For instance, the months of June, July, and September exhibit significant variations. Certain periods, like from July to September and from November to December, yielded positive returns.

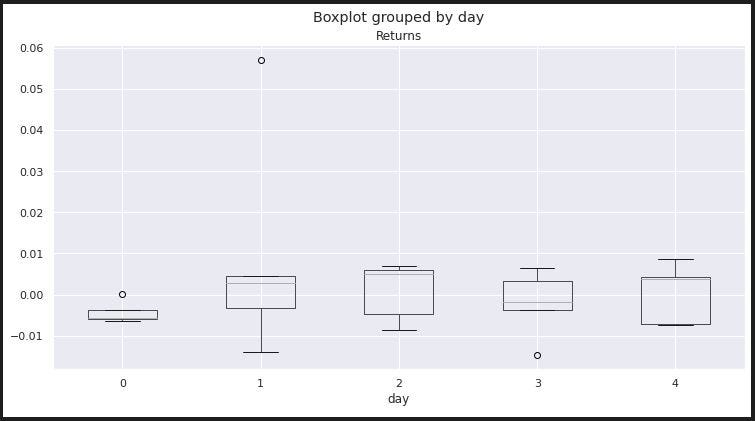

We also scrutinize the daily variation of Corn in previous years, noting returns tending to stay close to zero.

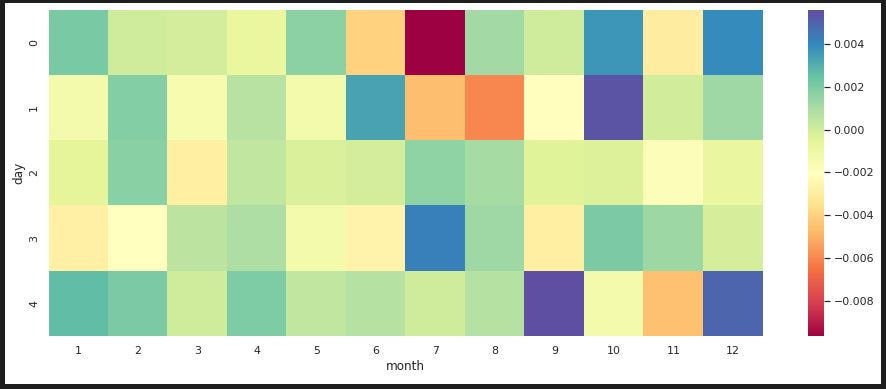

When observing return variation in a specific month, such as June, we discover that investing on Mondays and closing positions on Tuesdays or Wednesdays could generate positive returns. Similarly, for December, trading from Wednesday to Friday might be advantageous.

We proceed to explore studies based on heatmaps, which visualize the magnitude of a phenomenon using colors. We observe that buying on Mondays and selling on Thursdays in July could be an effective strategy.

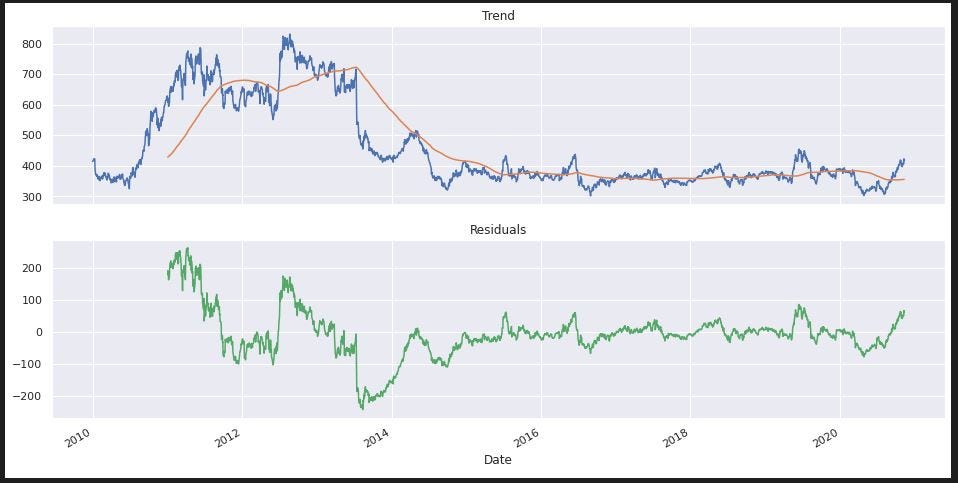

Next, we remove data trends to avoid biases and update our study. Although previous patterns become less clear, the potential for increases from November to December still remains.

For visual confirmation, we use the statsmodels library to decompose data into trend, seasonal, and residual components. This reveals how closing price, trend, and seasonal components relate.

In summary, studies on seasonal patterns in markets offer valuable insights. Understanding these trends can enrich your investment strategies and enable informed decision-making.

What is a seasonal pattern? According to José Martínez, a seasonal pattern pertains to the market behavior of specific assets within a particular time frame. For instance, commodities like soy, wheat, and oil are influenced by climatic conditions.

Do other financial assets respond to seasonal patterns? Yes, seasonal patterns can correlate with regular events such as employment data, stock levels, or consumption. Dimitri Speck has demonstrated that seasonality outperforms other investment strategies.

To analyze this, we employ quartiles and a box and whisker plot, statistical tools. Quartiles divide data into four parts, while the box and whisker plot visually displays the median and quartiles.

We apply these tools to Corn contract data, uncovering seasonal patterns in returns. For instance, the months of June, July, and September exhibit significant variations. Certain periods, like from July to September and from November to December, yielded positive returns.

We also scrutinize the daily variation of Corn in previous years, noting returns tending to stay close to zero.

When observing return variation in a specific month, such as June, we discover that investing on Mondays and closing positions on Tuesdays or Wednesdays could generate positive returns. Similarly, for December, trading from Wednesday to Friday might be advantageous.

We proceed to explore studies based on heatmaps, which visualize the magnitude of a phenomenon using colors. We observe that buying on Mondays and selling on Thursdays in July could be an effective strategy.

Next, we remove data trends to avoid biases and update our study. Although previous patterns become less clear, the potential for increases from November to December still remains.

For visual confirmation, we use the statsmodels library to decompose data into trend, seasonal, and residual components. This reveals how closing price, trend, and seasonal components relate.

In summary, studies on seasonal patterns in markets offer valuable insights. Understanding these trends can enrich your investment strategies and enable informed decision-making.