You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Let's talk about eliminating noise in the charts

- Thread starter nooby_mcnoob

- Start date

For what it's worth, a couple things.

In the treasury market, traders will spread the CBOT contracts like ZB/ZN or ZN/ZF in order to cut down on noise in the action. You can get better reads on the market this way. You can even spread those to cut down further on noise -- eg. UB/ZB against ZB/ZN, i.e. a treasury butterfly.

In this market (rate futures), the primary dealers/broker-dealers use the ICS market to manipulate the outright books all the time. And it's the same thing with the investment banks and their index/stock market manipulation.

Index markets are the same with traders watching Nikkei/SP or FDAX/Eurostoxx spreads and so forth. If you watch the S&P 500 / Dow Jones spread, you will be charting implied Nasdaq 100 pricing (this is like a beta ratio spread). The DJX/RUT spread is nice and smooth. The front month NQ/ES differential is one of the heaviest traded besides the S&P 500 vs Dow 30. A chart of MSFT against QQQ will trade much more smoothly than NQ outright.

XLK vs XLF is another spread that will have much lower noise than single names, outright index instruments, or even outright sector ETFs.

(try and ask yourself why)

If you have never done it, you should watch something like ES/YM while having the globex ES book on-screen. It's a big eye opener and will show you just how much noise and other games are being played in these markets.

The order book/ladder/stop-limit/limit order manipulations are unrelenting and absolutely ruthless.

The moral of the story is that prices are manipulated to drive up volumes, control execution costs, maintain liquidity provider profit margins, and line the pockets of trading firms/broker dealers. But some things are much harder to manipulate than others.

It really helps to think about the total size of the market you are charting and how liquid it really is.

If you want to cut down on noise, it makes a lot of sense to price one asset in terms of another.

In crypto land, this would be like watching ETH/BTC instead of ETH outright.

In the treasury market, traders will spread the CBOT contracts like ZB/ZN or ZN/ZF in order to cut down on noise in the action. You can get better reads on the market this way. You can even spread those to cut down further on noise -- eg. UB/ZB against ZB/ZN, i.e. a treasury butterfly.

In this market (rate futures), the primary dealers/broker-dealers use the ICS market to manipulate the outright books all the time. And it's the same thing with the investment banks and their index/stock market manipulation.

Index markets are the same with traders watching Nikkei/SP or FDAX/Eurostoxx spreads and so forth. If you watch the S&P 500 / Dow Jones spread, you will be charting implied Nasdaq 100 pricing (this is like a beta ratio spread). The DJX/RUT spread is nice and smooth. The front month NQ/ES differential is one of the heaviest traded besides the S&P 500 vs Dow 30. A chart of MSFT against QQQ will trade much more smoothly than NQ outright.

XLK vs XLF is another spread that will have much lower noise than single names, outright index instruments, or even outright sector ETFs.

(try and ask yourself why)

If you have never done it, you should watch something like ES/YM while having the globex ES book on-screen. It's a big eye opener and will show you just how much noise and other games are being played in these markets.

The order book/ladder/stop-limit/limit order manipulations are unrelenting and absolutely ruthless.

The moral of the story is that prices are manipulated to drive up volumes, control execution costs, maintain liquidity provider profit margins, and line the pockets of trading firms/broker dealers. But some things are much harder to manipulate than others.

It really helps to think about the total size of the market you are charting and how liquid it really is.

If you want to cut down on noise, it makes a lot of sense to price one asset in terms of another.

In crypto land, this would be like watching ETH/BTC instead of ETH outright.

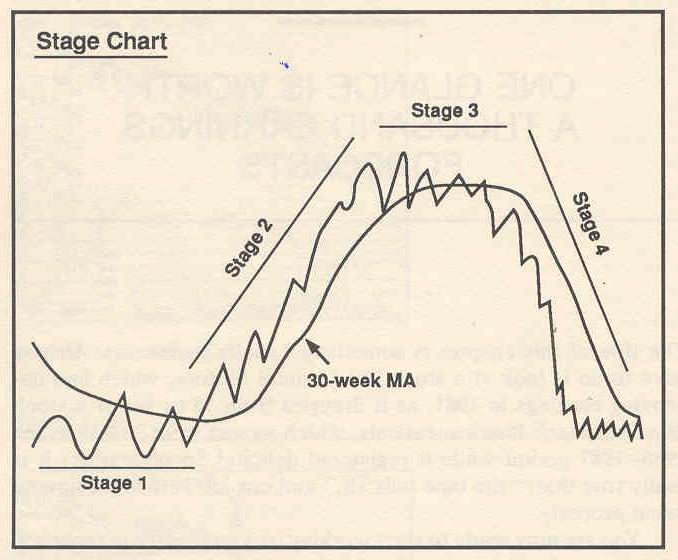

That is an oldie from years gone by.Stan Weinstein's 4 stages analysis.

Look at GE chart from 2010 to 2020. Not an exact match but one can tell all the stages. In stock charting, it's just a rough science.

%%Does not get the point across....

Profit solutions include , but limited to 50dma, longer time frames................................................................................................

One trader's noise is another trader's trend. A single 5 minute bar in the middle of barbwire may represent one or more trends on a 10 second chart.

Just like trends, define what you mean by noise on the time frame you're trading.

Just like trends, define what you mean by noise on the time frame you're trading.

Sometimes when NQ goes parabolic I think it might actually loop backwards.

If you start seeing charts as if they've been hand-drawn... it's not noise nor bad data. It's drawn by a trader smoking pot. That's when it's time to take a break from trading and close your computer...go to a rehab facility to detox.

Simply, it's not reality. Then again, next time just post a bar chart or candlestick chart...that's not hand-drawn.

wrbtrader

If you start seeing charts as if they've been hand-drawn... it's not noise nor bad data. It's drawn by a trader smoking pot. That's when it's time to take a break from trading and close your computer...go to a rehab facility to detox.

Simply, it's not reality. Then again, next time just post a bar chart or candlestick chart...that's not hand-drawn.

View attachment 272416

wrbtrader

Clearly you are a pro at spotting noise!

One trader's noise is another trader's trend. A single 5 minute bar in the middle of barbwire may represent one or more trends on a 10 second chart.

Just like trends, define what you mean by noise on the time frame you're trading.

I'm starting to really like 10 second charts...

If you start seeing charts as if they've been hand-drawn... it's not noise nor bad data. It's drawn by a trader smoking pot. That's when it's time to take a break from trading and close your computer...go to a rehab facility to detox.

Simply, it's not reality. Then again, next time just post a bar chart or candlestick chart...that's not hand-drawn.

View attachment 272416

wrbtrader

I see an instantaneous arb