Hey guys,

This week, I tested the enhanced strategy as suggested by Larry Connors in his "Short Term Trading Strategies That Work” book. It uses Cumulative RSIs instead of the vanilla RSI. They do offer a statistical edge (details are in the full article).

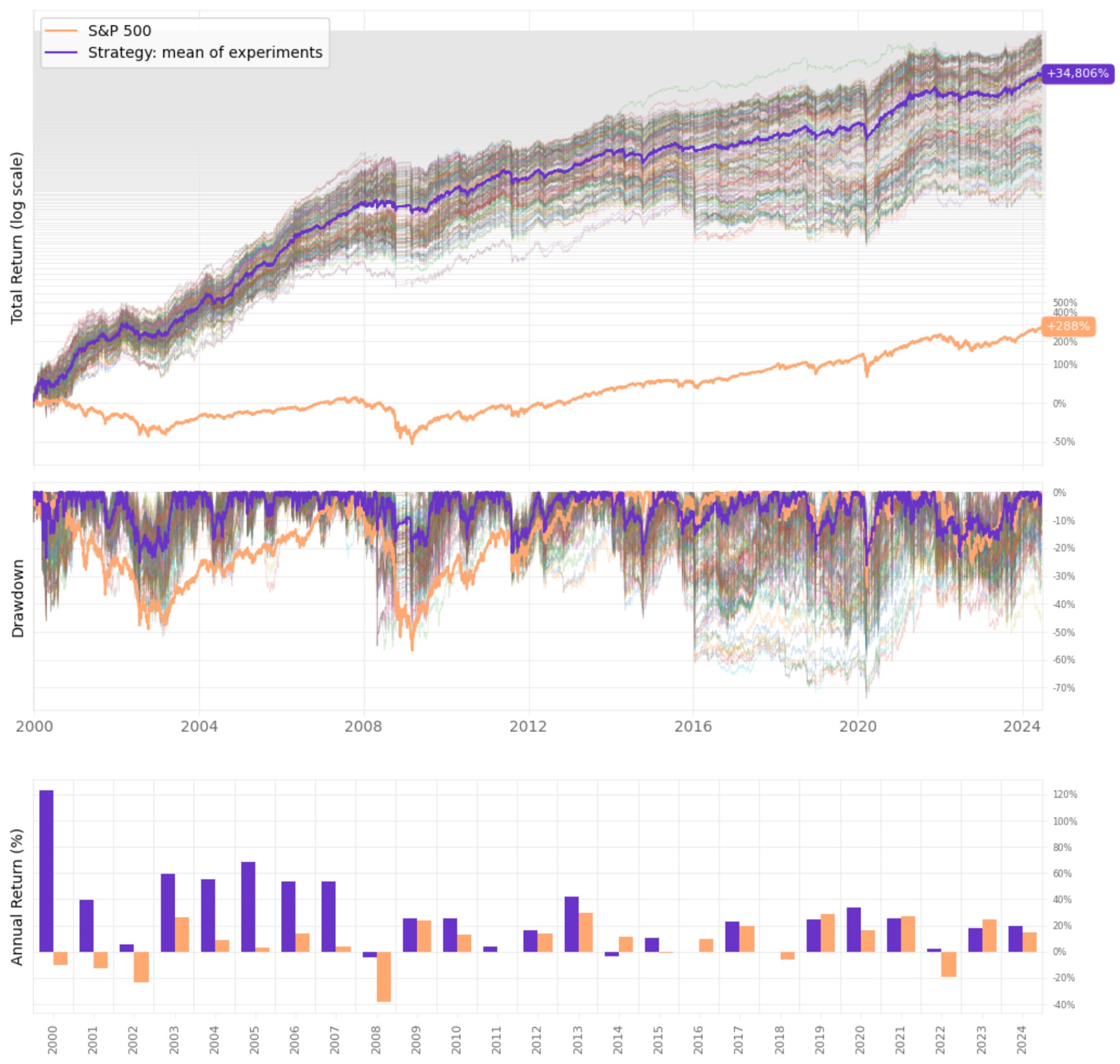

The strategy achieves a 26% annual return with 1.18 Sharpe. The maximum drawdown is 37%, much better than the S&P 500's (57%) during the 24-year period but still too high.

From now on, I decided to share a sensitivity analysis to prevent overfitting, something several people here talked about. The results below show close to 200 experiments obtained by varying the parameters in the parameter space:

Equity curve, drawdown curve, and annual returns for the enhanced strategy 198 variations

Statistics for the main indicators of the 198 experiments

Sensitivity of annual return for maximum positions of 3

The rules in detail:

I'd love to hear what you guys think. Cheers!

This week, I tested the enhanced strategy as suggested by Larry Connors in his "Short Term Trading Strategies That Work” book. It uses Cumulative RSIs instead of the vanilla RSI. They do offer a statistical edge (details are in the full article).

The strategy achieves a 26% annual return with 1.18 Sharpe. The maximum drawdown is 37%, much better than the S&P 500's (57%) during the 24-year period but still too high.

From now on, I decided to share a sensitivity analysis to prevent overfitting, something several people here talked about. The results below show close to 200 experiments obtained by varying the parameters in the parameter space:

Equity curve, drawdown curve, and annual returns for the enhanced strategy 198 variations

Statistics for the main indicators of the 198 experiments

Sensitivity of annual return for maximum positions of 3

The rules in detail:

- Whenever the 2-day cumulative RSI (2 days) is below 10, we buy on the next opening;

- Whenever the 2-day cumulative RSI (2 days) is above 65, we exit on the next opening;

- We only trade a stock if its price is above its 200-day SMA;

- We trade multiple stocks in parallel to increase exposure;

- If there are more than 3 opportunities to trade in any given day, we sort them by market cap and prioritize the lower market caps;

- We restrict ourselves to trade only large & mega caps to reduce the risk of delisting;

- We limit to holding 3 positions at any given time, maximum;

- Whenever the stock closes below its 200-day SMA, if we have a position, we exit at the next open.

- We will restrict ourselves to only trade stocks that have been traded in all sessions over the past 3 months from the day in question;

- We will only trade the stock if the allocated capital for the trade does not exceed 5% of the stock's median ADV of the past 3 months from the day in question.

I'd love to hear what you guys think. Cheers!