")

Not only has no one written that the domain between sub-segments be the same, but I have repeated referenced it being variable as a relevant factor.

,

,  ,

,  ,

,

That said, great exhibits (labeling aside).

, , ,

, , , (labeling aside).

So if you're not here to discuss and explain the reasoning for your opinions, I'm just curious what are you here for?

If we test a bunch of strategies on data segment 1 and then data segment 2 and then keep the ones that do well on both..........

Isn't that the same as testing them on segment 3 which is a combination of 1 and 2 and keeping "the good ones"?

We'll arrive to the same choice of strats in both cases, no?

When Segment 1 contains vastly different characteristics to Segment 2, then the strategies we arrived at in (B), are going to be different to the Strategies we arrived at in (A).

As a matter of fact, if"Hey! I should *build* my models on all possible data, and not leave some data out for testing/validating!"

As a matter of fact, if

- a strategy is built on a good prior hypothesis

- the effect has good statistical significance

- and the number of free parameters is low (preferably none)

it's a perfectly OK thing to do. In fact, you would be better served building a collection of simple strategies this way vs going in circles optimizing something complex.

You are missing that the x-axis values are different in segment 1 vs segment 2.

Hypothetically, the best strategy for segment 1 can also be the best strategy for segment 2.

What are you talking about? Hypothetically sure, the best streagy for segment 1 can also be the best strategy for segment 2. However, it can also not be the best strategy aswell.

I'm here for trading related entertainment.

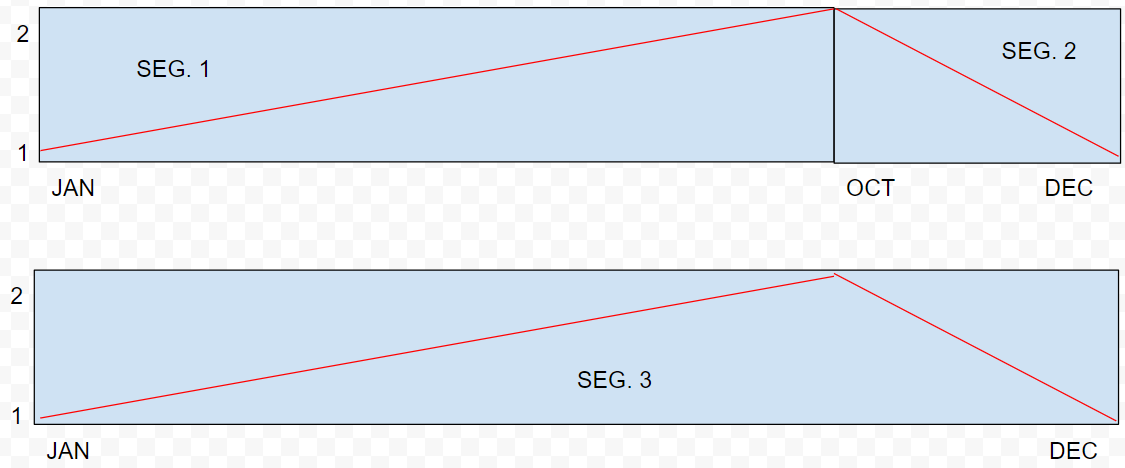

-Segment 1 (70% or data) turns out to be based on a strong bull market,

-Segment 2( 30% of data) turns out to be based on a rapid decline.

-Segment 3 (100% of data)

*we have a long only strategy

*we are blinded and have no idea what the data in segment 2 looks like

A) If we tested strategies based only on segment 1, then the equity curves could significantly under-perform on segment 2, making the strategies no longer viable. If some still performed as expected ( even after a regime change), then we know what to investigate further.

B) If we were unblinded and tested strategies across all data 1+2( Segment 3) our strategy design could have already compensated for the decline seen in segment 2( In fact we might have decided that a long only strategy was no longer a viable option). Either way, we have opened ourselves up to curve fitting, or at least increased the likelihood.

When Segment 1 contains vastly different characteristics to Segment 2, then the strategies we arrived at in (B), are going to be different to the Strategies we arrived at in (A). Even though the strategies that performed well in (A) will still perform the same in (B), they could easily get overlooked for better performing strategies derived from only (B). Therefore we will not arrive with the same choice of strategies in both cases.