Is the U.S. Banking System Safe?

August 03, 2008

by James Quinn

*James Quinn is Senior Director of Strategic Planning, The Wharton School, University of Pennsylvania.

"Treasury Secretary Henry Paulson delivered an upbeat assessment of the economy, saying growth was healthy and the housing market was nearing a turnaround. 'All the signs I look at' show 'the housing market is at or near the bottom,' Paulson said in a speech to a business group in New York. The U.S. economy is 'very healthy' and 'robust,' Paulson said. (CBS Marketwatch 4/20/07)

****************************

âAt this juncture, the impact on the broader economy and financial markets of the problems in the subprime market seems likely to be contained.â (Ben Bernanke during Congressional Testimony 3/2007)

****************************

"We will follow developments in the subprime market closely. However, fundamental factorsâincluding solid growth in incomes and relatively low mortgage ratesâshould ultimately support the demand for housing, and at this point, the troubles in the subprime sector seem unlikely to seriously spill over to the broader economy or the financial system." (Ben Bernanke 6/5/07)

****************************

"It is not the responsibility of the Federal Reserveânor would it be appropriateâto protect lenders and investors from the consequences of their financial decisions. But developments in financial markets can have broad economic effects felt by many outside the markets, and the Federal Reserve must take those effects into account when determining policy."

(Ben Bernanke 10/15/07)

****************************

âWeâve got strong financial institutionsâ¦Our markets are the envy of the world. Theyâre resilient, theyâreâ¦innovative, theyâre flexible. I think we move very quickly to address situations in this country, and, as I said, our financial institutions are strong.â (Henry Paulson 3/16/08)

Deception â Keeping the Ponzi Scheme Going

After reading the above quotes, it should be clear to you that these gentlemen do not have a clue. Our economy and banking system is so complex and intertwined that no one knows where the next shoe will drop. Politicians and government bureaucrats are lying to the public when they say that everything is alright. They do not know. Therefore, it is in our best interest to cut through all the crap and examine the facts with a skeptical eye.

Last week, bank stocks, which had been falling faster than President Bushâs approval rating, soared higher based on earnings reports that were horrific, but not catastrophic.

Again, the talking heads, like Larry Kudlow, were calling a bottom in the financial crisis. The bank with the largest increase in share price was Wells Fargo. Their earnings exceeded analyst expectations and the stock went up 22% in one day. Wells Fargo (WFC) has $84 billion of home equity loans, with half of those in California and Florida.

Coincidently, Wells Fargo decided to extend its charge-off policy in the 2nd quarter from 120 days to 180 days, in an effort to give troubled borrowers more time to reach a loan workout. A skeptical person might think that they did not change this policy out of the goodness of their hearts.

Maybe, just maybe, they changed this policy to reduce their write-offs for the 2nd quarter, to beat analyst expectations.

There are many stories of people who are still living in houses, twelve months after making their last mortgage payment. Their banks have not started foreclosure proceedings.

Is this due to incompetence by the banks, or is this a way to avoid writing off the loss? The FASB has joined the cover-up gang by delaying the implementation of new rules that would have made banks stop hiding toxic waste off-balance sheet. The new rule would have made banks put these questionable assets on their balance sheet and would have required a bigger capital cushion

What a surprise that bank regulators, the Treasury and Federal Reserve urged a delay in implementation. Manipulate the facts because the average American doesnât understand or care. Sounds like Enron accounting standards to me.

The Future FDIC Bailout

During the S&L crisis in the early 1990s, 1,500 banks failed. So far, seven banks have failed in 2008, the largest being IndyMac. The FDIC has about $53 billion in funds to handle future bank failures. The IndyMac failure is expected to use $4 to $8 billion of those funds. Average Americans will lose $500 million in uninsured deposits in this failure. The FDIC says that they have 90 banks on their âwatch listâ. They do not reveal the banks on the list, so little old ladies with their life savings in the local bank will be surprised when they go belly up. Based on the fact that IndyMac was not on their âwatch listâ, I wouldnât put too much faith in their analysis.

There are 8,500 banks in the U.S. Based on an independent analysis by Chris Whalen from Institutional Risk Analytics, they have identified 8% of all banks, or around 700 banks as troubled. This is quite a divergence from the FDIC estimate. Should you believe a governmental agency that wants the public to remain in the dark to avoid bank runs, or an independent analysis based upon balance sheet analysis? The implications of 700 institutions failing are huge. There is roughly $6.84 trillion in bank deposits.

It is almost beyond belief that $2.6 trillion of these deposits are uninsured. There is only $274 billion of the $6.84 trillion as cash on hand at banks. This means that $6.5 trillion has been loaned to consumers, businesses, developers, etc. The FDIC has $53 billion to cover $6.84 trillion of deposits. Does that give you a warm feeling?

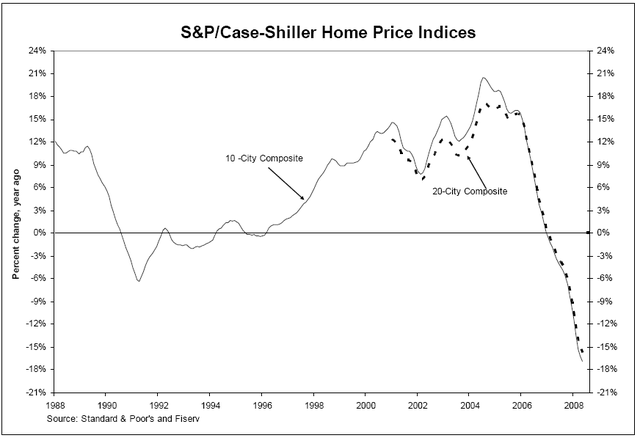

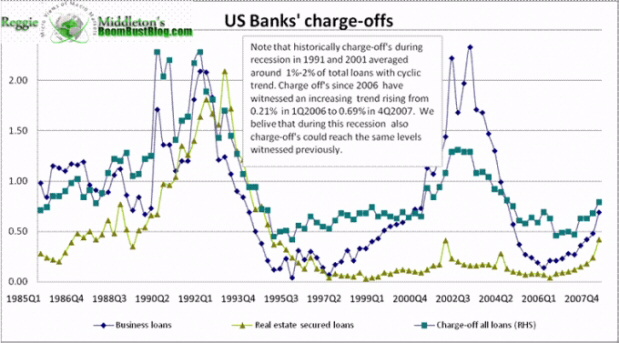

Based on the chart below, I would estimate that we are only in the early innings of bank write-offs. The write-offs will at least equal the previous peaks reached in the early 1990s.

If a large bank such as Washington Mutual (WM) or Wachovia (WB) were to fail, it would wipe out the FDIC fund.

If the FDIC fund is depleted, guess who will pay? Right again, another taxpayer bailout. Whatâs another $100 or $200 billion among friends.

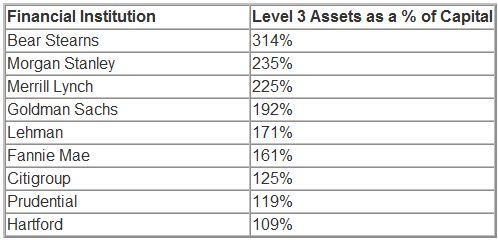

What is a Level 3 Asset?

Other banks have been moving assets to Level 2 and Level 3 in order to put off the inevitable losses. The definition of these levels according to FAS 157 are as follows:

1. Level 1 Assets that have observable market prices.

2. Level 2 Assets that donât have an observable prices, but they have inputs that are based upon them.

3. Level 3 Assets where one or more of the inputs donât have observable prices. Reliant on management estimates. Also known as mark to model.

This is Warren Buffetâs view on the financial institution practice of valuing subprime assets on the basis of a computer model rather than the free market price.

In one way, I'm sympathetic to the institutional reluctance to face the music. I'd give a lot to mark my weight to 'model' rather than to market.

So, the managements of the banks that loaned money to people who could never pay them back are now responsible for estimating what these assets are worth. According to Bill Fleckenstein,

Recently, the portfolio of Cheyne Finance, one of the more infamous structured-investment vehicles, or SIVs, was sold at 44 cents on the dollar. I suspect that similar assets are not marked anywhere near that valuation on financial institutions' balance sheets. So, the game of "everything's contained" continues, albeit in a different form.

Merrill Lynch â Poster Child for Lack of Bank Credibility

John Thain is the Chairman and CEO of Merrill Lynch. He makes in excess of $50 million per year in compensation. He previously held positions as President, COO and CFO at Goldman Sachs. He is a good buddy of Hank Paulson. Here are a few recent quotes from Mr. Thain:

"...These transactions make certain that Merrill is well-capitalized." (January 15, 2008 -- Thain in a statement after selling $6.6 billion of preferred shares to a group that included Japanese and Kuwaiti investors)

****************************

"...Today I can say that we will not need additional funds. These problems are behind us. We will not return to the market." (March 8, 2008 -- Thain in an interview with France's Le Figaro newspaper)

****************************

"We deliberately raised more capital than we lost last year ... we believe that will allow us to not have to go back to the equity market in the foreseeable future." (April 8, 2008 -- Thain to reporters in Tokyo, as reported by Reuters)

****************************

"Right now we believe that we are in a very comfortable spot in terms of our capital." (July 17, 2008 -- Thain on a conference call after posting Merrill's second-quarter results)

Merrill Lynch reported a loss of $4.7 billion for the 2nd quarter on July 17. On July 28, eleven days after this earnings report they announce a $5.7 billion write-down and the issuance of $8.5 billion of stock. Thain, the $50 million man, is either lying or completely clueless regarding the company he runs. The SEC needs to investigate him, rather than short-sellers. Their books are a fraud and anything their CEO says cannot be trusted.

-CONTINUED BELOW-

August 03, 2008

by James Quinn

*James Quinn is Senior Director of Strategic Planning, The Wharton School, University of Pennsylvania.

"Treasury Secretary Henry Paulson delivered an upbeat assessment of the economy, saying growth was healthy and the housing market was nearing a turnaround. 'All the signs I look at' show 'the housing market is at or near the bottom,' Paulson said in a speech to a business group in New York. The U.S. economy is 'very healthy' and 'robust,' Paulson said. (CBS Marketwatch 4/20/07)

****************************

âAt this juncture, the impact on the broader economy and financial markets of the problems in the subprime market seems likely to be contained.â (Ben Bernanke during Congressional Testimony 3/2007)

****************************

"We will follow developments in the subprime market closely. However, fundamental factorsâincluding solid growth in incomes and relatively low mortgage ratesâshould ultimately support the demand for housing, and at this point, the troubles in the subprime sector seem unlikely to seriously spill over to the broader economy or the financial system." (Ben Bernanke 6/5/07)

****************************

"It is not the responsibility of the Federal Reserveânor would it be appropriateâto protect lenders and investors from the consequences of their financial decisions. But developments in financial markets can have broad economic effects felt by many outside the markets, and the Federal Reserve must take those effects into account when determining policy."

(Ben Bernanke 10/15/07)

****************************

âWeâve got strong financial institutionsâ¦Our markets are the envy of the world. Theyâre resilient, theyâreâ¦innovative, theyâre flexible. I think we move very quickly to address situations in this country, and, as I said, our financial institutions are strong.â (Henry Paulson 3/16/08)

Deception â Keeping the Ponzi Scheme Going

After reading the above quotes, it should be clear to you that these gentlemen do not have a clue. Our economy and banking system is so complex and intertwined that no one knows where the next shoe will drop. Politicians and government bureaucrats are lying to the public when they say that everything is alright. They do not know. Therefore, it is in our best interest to cut through all the crap and examine the facts with a skeptical eye.

Last week, bank stocks, which had been falling faster than President Bushâs approval rating, soared higher based on earnings reports that were horrific, but not catastrophic.

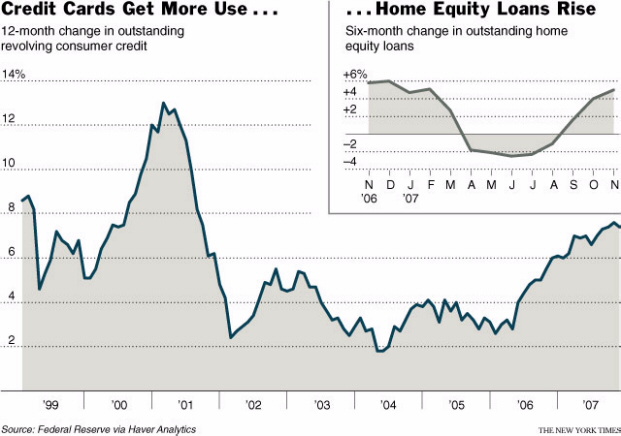

Again, the talking heads, like Larry Kudlow, were calling a bottom in the financial crisis. The bank with the largest increase in share price was Wells Fargo. Their earnings exceeded analyst expectations and the stock went up 22% in one day. Wells Fargo (WFC) has $84 billion of home equity loans, with half of those in California and Florida.

Coincidently, Wells Fargo decided to extend its charge-off policy in the 2nd quarter from 120 days to 180 days, in an effort to give troubled borrowers more time to reach a loan workout. A skeptical person might think that they did not change this policy out of the goodness of their hearts.

Maybe, just maybe, they changed this policy to reduce their write-offs for the 2nd quarter, to beat analyst expectations.

There are many stories of people who are still living in houses, twelve months after making their last mortgage payment. Their banks have not started foreclosure proceedings.

Is this due to incompetence by the banks, or is this a way to avoid writing off the loss? The FASB has joined the cover-up gang by delaying the implementation of new rules that would have made banks stop hiding toxic waste off-balance sheet. The new rule would have made banks put these questionable assets on their balance sheet and would have required a bigger capital cushion

What a surprise that bank regulators, the Treasury and Federal Reserve urged a delay in implementation. Manipulate the facts because the average American doesnât understand or care. Sounds like Enron accounting standards to me.

The Future FDIC Bailout

During the S&L crisis in the early 1990s, 1,500 banks failed. So far, seven banks have failed in 2008, the largest being IndyMac. The FDIC has about $53 billion in funds to handle future bank failures. The IndyMac failure is expected to use $4 to $8 billion of those funds. Average Americans will lose $500 million in uninsured deposits in this failure. The FDIC says that they have 90 banks on their âwatch listâ. They do not reveal the banks on the list, so little old ladies with their life savings in the local bank will be surprised when they go belly up. Based on the fact that IndyMac was not on their âwatch listâ, I wouldnât put too much faith in their analysis.

There are 8,500 banks in the U.S. Based on an independent analysis by Chris Whalen from Institutional Risk Analytics, they have identified 8% of all banks, or around 700 banks as troubled. This is quite a divergence from the FDIC estimate. Should you believe a governmental agency that wants the public to remain in the dark to avoid bank runs, or an independent analysis based upon balance sheet analysis? The implications of 700 institutions failing are huge. There is roughly $6.84 trillion in bank deposits.

It is almost beyond belief that $2.6 trillion of these deposits are uninsured. There is only $274 billion of the $6.84 trillion as cash on hand at banks. This means that $6.5 trillion has been loaned to consumers, businesses, developers, etc. The FDIC has $53 billion to cover $6.84 trillion of deposits. Does that give you a warm feeling?

Based on the chart below, I would estimate that we are only in the early innings of bank write-offs. The write-offs will at least equal the previous peaks reached in the early 1990s.

If a large bank such as Washington Mutual (WM) or Wachovia (WB) were to fail, it would wipe out the FDIC fund.

If the FDIC fund is depleted, guess who will pay? Right again, another taxpayer bailout. Whatâs another $100 or $200 billion among friends.

What is a Level 3 Asset?

Other banks have been moving assets to Level 2 and Level 3 in order to put off the inevitable losses. The definition of these levels according to FAS 157 are as follows:

1. Level 1 Assets that have observable market prices.

2. Level 2 Assets that donât have an observable prices, but they have inputs that are based upon them.

3. Level 3 Assets where one or more of the inputs donât have observable prices. Reliant on management estimates. Also known as mark to model.

This is Warren Buffetâs view on the financial institution practice of valuing subprime assets on the basis of a computer model rather than the free market price.

In one way, I'm sympathetic to the institutional reluctance to face the music. I'd give a lot to mark my weight to 'model' rather than to market.

So, the managements of the banks that loaned money to people who could never pay them back are now responsible for estimating what these assets are worth. According to Bill Fleckenstein,

Recently, the portfolio of Cheyne Finance, one of the more infamous structured-investment vehicles, or SIVs, was sold at 44 cents on the dollar. I suspect that similar assets are not marked anywhere near that valuation on financial institutions' balance sheets. So, the game of "everything's contained" continues, albeit in a different form.

Merrill Lynch â Poster Child for Lack of Bank Credibility

John Thain is the Chairman and CEO of Merrill Lynch. He makes in excess of $50 million per year in compensation. He previously held positions as President, COO and CFO at Goldman Sachs. He is a good buddy of Hank Paulson. Here are a few recent quotes from Mr. Thain:

"...These transactions make certain that Merrill is well-capitalized." (January 15, 2008 -- Thain in a statement after selling $6.6 billion of preferred shares to a group that included Japanese and Kuwaiti investors)

****************************

"...Today I can say that we will not need additional funds. These problems are behind us. We will not return to the market." (March 8, 2008 -- Thain in an interview with France's Le Figaro newspaper)

****************************

"We deliberately raised more capital than we lost last year ... we believe that will allow us to not have to go back to the equity market in the foreseeable future." (April 8, 2008 -- Thain to reporters in Tokyo, as reported by Reuters)

****************************

"Right now we believe that we are in a very comfortable spot in terms of our capital." (July 17, 2008 -- Thain on a conference call after posting Merrill's second-quarter results)

Merrill Lynch reported a loss of $4.7 billion for the 2nd quarter on July 17. On July 28, eleven days after this earnings report they announce a $5.7 billion write-down and the issuance of $8.5 billion of stock. Thain, the $50 million man, is either lying or completely clueless regarding the company he runs. The SEC needs to investigate him, rather than short-sellers. Their books are a fraud and anything their CEO says cannot be trusted.

-CONTINUED BELOW-