No, IB does this with orders you have no desire to be hidden and that you fully intend to display to the world. It's yet another hidden "feature" of their system, in market that's moved significantly "the algorithm" will decide that the current public bid/ask prices aren't marketable and refuse to send your ordinary limit order, even if it's at the current bid/ask respectively, to the market until it, in it's infinite wisdom, decides that the current market prices are marketable. It's a ham handed attempt to stop orders that might later be busted, but frustrating as hell when you get caught by it, especially when you are trying to exit a position. I've seen it most often in some of the more obscure metals futures contracts (and no, they weren't limit up or down).Well it’s doing what you asked for - not showing your order until it can be filled. Whether or not that’s a recipe for good execution is up to the individual trader. If they couldn’t send a hidden order to the exchange and it wasn’t marketable, what do you want them to do with it? Holding it is really the only choice consistent with the instructions given by the trader. I haven’t seen IB hold orders when they can send them to the exchange, but I don’t know what exchanges or markets OP is referring to so I can’t be sure.

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Is IB's Hidden orders type "real" (or simulated)? Can a hidden Buy hit a hidden Offer?

- Thread starter d0rian

- Start date

Why do you think you would bet a better execution not being represented in the NBBO and having no protection of trade throughs? At least an Iceberg order would show your price but not size. A hidden order makes no sense to me. For my orders, I want price discover and for all the players to see my order. I can understand wanting a 1000 lot to look like 10, but not zero. Especially with options. I just don't get it.

1) As to bolded part, in the case of an illiquid option listing, if NBBO is showing only market-maker's $1.00 x $2.00 spread, and I see another trader put in a Limit Bid of, say, 5 x $1.10, wouldn't submitting a Hidden Bid of 5 x $1.15 effectively allow me to sit ahead of him for a Seller, whereas if that were a visible Bid it might induce competing Bidder to go up to 5 x $1.20, etc?

2) Eh...actually, initially I wasn't quite sure what you'd meant by "no protection of trade-throughs", but...did I just effectively answer that? I.e. using my hypothetical numbers in #1 above (where I'm sitting with Hidden 10 x $1.15), what happens if a Seller:

(i) puts in a 5 x $1.10 Limit Sell order?

(ii) puts in a 5-lot Market Sell order?

In either of those cases, if this is a non-native (aka held-by-IB-until-marketable) Hidden order, wouldn't it just immediately hit the other Bidder's visible 5 x $1.10 Bid (even tho I was sitting there hidden at 5 x $1.15)? Whereas if it were a Hidden Bid natively supported by the exchange, I'd get hit at 5 x $1.15, right?

This is cool. https://www.sec.gov/marketstructure/datavis/ma_exchange_hiddenvolume.html#.XEETklxKiUk

Nasdaq calls them NON-DISPLAY orders.

https://www.nasdaqtrader.com/content/ProductsServices/Trading/OrderTypesG.pdf

Orders are hidden from the marketplace. All incoming order flow can interact with hidden orders until hidden size is exhausted at the specified price.

I do not recommend this order type.

Not sure if any of this applies to Options? (we're in Options forum)

I've been experimenting for the first time with IB's Display Size field, which allows you to display a quantity smaller than your entire order size to the market, or hide it altogether.

When I select a smaller quantity from the Display Size dropdown it works as expected (my bid/offer shows up on tape as a live quote, with my chosen size displayed), but when I choose "Hidden", IB's order status is dark blue, with note "Order is being held and monitored". IB tells me that the way their Hidden orders work is that they're held by the IB server, and not actually sent out to an exchange until the order is marketable (aka there's a live Offer at my hidden Bid, or vice versa).

1) Is this the standard way that Hidden orders are treated, or unique to IB?

2) i.e. Do exchanges even have the functionality to handle true hidden orders on the exchange side, or is it always going to have to be a broker-side process?

3) One result of this process, if I'm understanding correctly, is that there's no way for a Hidden Bid to ever hit a Hidden Offer, right? Because neither is actually ever sent out until there's a marketable counterpart, so if both are Hidden it's a stalemate(?)...or might IB match up hidden orders if they both happen to be IB clients (and so theoretically could transact without the orders ever being sent to the exchange)?

Display Size = 0 will work very differently than Non-Zero Display Size, so these are different topics. When you mix them up you may not get clear answers.

Also, orders for an option often work differently than orders for an option combo like spread, butterfly, etc. When you mix such topics than you really may not get any clear answers.

Basically your question may not be answerable (or everyone will answer it to their liking) unless you unmix these different topics and focus on one thing at a time.

Generally hidden orders in IB will change the display size to 0 and vice-versa. They are not related to orders with non-zero display size. Hidden orders with display size=0 are held by IB internally until the price calculated based on individual option prices becomes marketable. In case of option combos such orders will very rarely get filled unless you make the price very unfavorable to yourself - although once the order becomes marketable it gets sent to exchanges and may get filled at a better price than you've originally set.

Last edited:

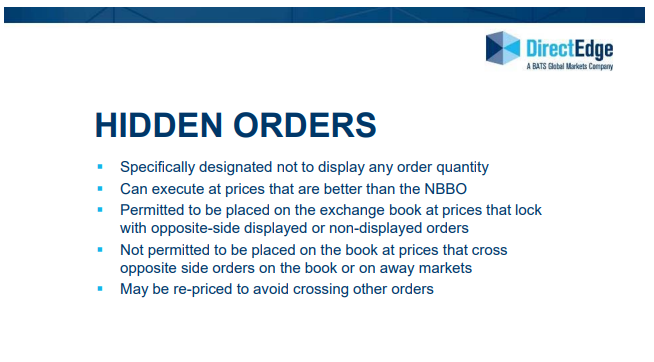

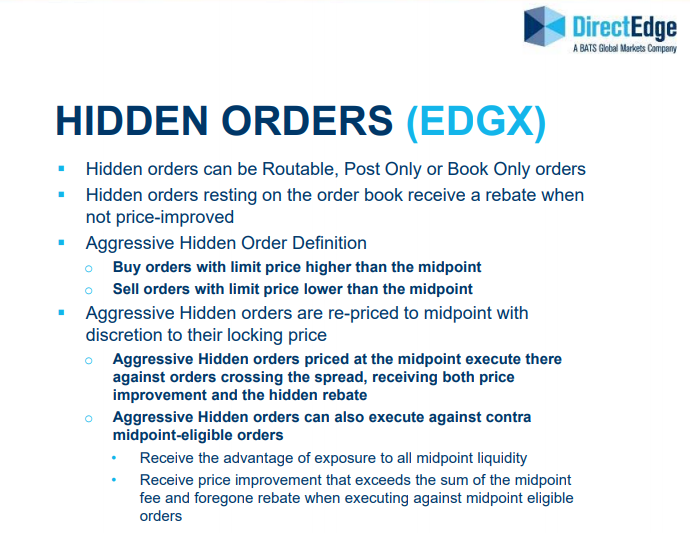

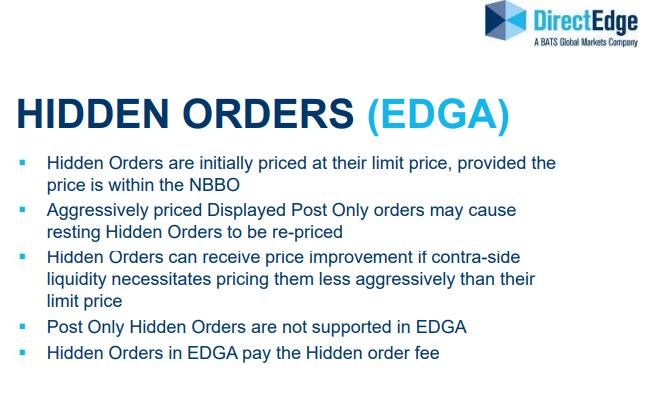

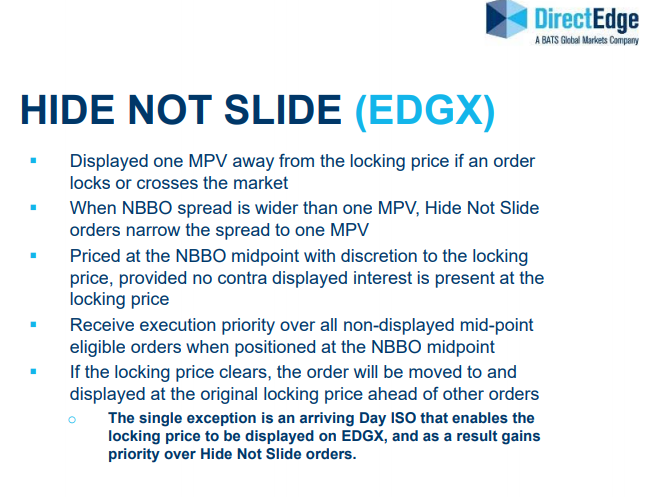

I am not sure if DirectEdge still offers the below order types. If i remember correctly, they got fined before Bats acquired them for Hide not Slide orders for not properly defining them.

http://cdn.batstrading.com/resources/membership/EDGE_Order_Type_Guide.pdf

http://cdn.batstrading.com/resources/membership/EDGE_Order_Type_Guide.pdf

When the order status goes blue its not a truly hidden order, its more like a stop limit order of sorts. It needs to be green to offer a lot of benefits to the trader(like potentially reducing adverse selection). In order to do that direct route (rather than using SMART) to places ARCA/ISLD/NDAQ/NYSE, that should do it

A true native hidden order is only active on the exchange where it is active, so other market participants can trade through your bid on other exchanges. I also believe a hidden order is assigned lower priority at the same limit price compared to a lit order....I'm not quite sure I understand this; it's trading through your Bid, so surely it's "marketable"...? Or are you talking about in the case of the "simulated" Hidden order (held by IB), where it won't ever actually get sent to the exchange, because all IB sees on its side is a $1.05 Offer (and then executions at $1.00 on the tape but never, I suppose, an Offer at or below your $1.02 Bid...?) But surely in the case where the Hidden order is fully supported and handled natively by the Exchange, this wouldn't be the case (right?)

Robert Morse

Sponsor

There are 15 option exchanges. Held at IB or on an exchange, your order has no protection. If you want to give he a call this morning I can provide more details. I'm telling you that these orders are not in your best interest. Just that simple....I'm not quite sure I understand this; it's trading through your Bid, so surely it's "marketable"...? Or are you talking about in the case of the "simulated" Hidden order (held by IB), where it won't ever actually get sent to the exchange, because all IB sees on its side is a $1.05 Offer (and then executions at $1.00 on the tape but never, I suppose, an Offer at or below your $1.02 Bid...?) But surely in the case where the Hidden order is fully supported and handled natively by the Exchange, this wouldn't be the case (right?)

Robert Morse

Sponsor

It does not. I did not know he was asking about options and in the past, posters choose the wrong forum more often than the right one. My bad.Not sure if any of this applies to Options? (we're in Options forum)

There is also an issue with "hidden liquidity" on the option exchanges. Say Schwab has a routing deal with Sig. Sig displays a market of 1.02 X 1.05 20 X 20. Sig' real market 1:00 X 1:03 450 X 600 and it sits hidden on an exchange.

Now an order comes in from Merrill to fill 20 contracts at 1.05. Sig has to fill 10 at 1.05 or better and can choose to fill anotmher 10 at 1:05 or better or ship then balance via linkage

Same market - Schwab sends in and order for 200 contracts at 1.03 they fill under the preferenced liquidity rule. Generally these preference orders will be eithehr better size so little or nothing ships

As Robert pointed out 15 venues and the are all linked. No dark pools, but there is dark liquidity. Generally the firm taking the most generous payments are participants in the "hidden liquidity" programs and not every broker has access to this hidden liquidity in options. Why would an MM offer a better market than what "they show" the industry? The assumption is that this "inside market" will bring more firms to it's Smart Router

Now an order comes in from Merrill to fill 20 contracts at 1.05. Sig has to fill 10 at 1.05 or better and can choose to fill anotmher 10 at 1:05 or better or ship then balance via linkage

Same market - Schwab sends in and order for 200 contracts at 1.03 they fill under the preferenced liquidity rule. Generally these preference orders will be eithehr better size so little or nothing ships

As Robert pointed out 15 venues and the are all linked. No dark pools, but there is dark liquidity. Generally the firm taking the most generous payments are participants in the "hidden liquidity" programs and not every broker has access to this hidden liquidity in options. Why would an MM offer a better market than what "they show" the industry? The assumption is that this "inside market" will bring more firms to it's Smart Router

Last edited: