The VIX is getting low again and I'd be looking to get long vol if the cash index got to 10 or below. Not a big fan of inventorying option premium, but what long vol position do you guys think has the highest upside/least downside risk when the VIX gets historically low? Choices:

1. Buy VIX futures

- Trades at a premium to the cash, can only replicate the cash instrument through the OTC variance swap market

- Lose money on the roll yield due to unfavorable VIX term structure

2. Buy VIX calls

- Expensive like SPX puts

3. Buy SPX/SPY OTM or winger puts

- Most crowded trade, buying the skew at its steepest point

4. Buy exceptionally cheap SPX calls and fully delta hedge them

- Vega and vol exposure disappears on a large sell-off

5. Sell 1x2 SPX/SPY put ratios, or sell 1x2 VIX call ratios

- Overpaying double on the steep skew/slope

6. Buy straddles or strangles in SPX/SPY/VIX

- Get eaten alive by theta, even if vol has bottomed out

7. Buy straddles or strangles in SPX/SPY/VIX

- Get eaten alive by theta waiting for the big move, even if vol has bottomed out

8. Buy one or more of the VIX-related ETFs: VXX, TVIX, UVXY, etc.

- Never get what you expect from leveraged ETFs

Good question VolSkewTrader

What to do now with the VIX this low.

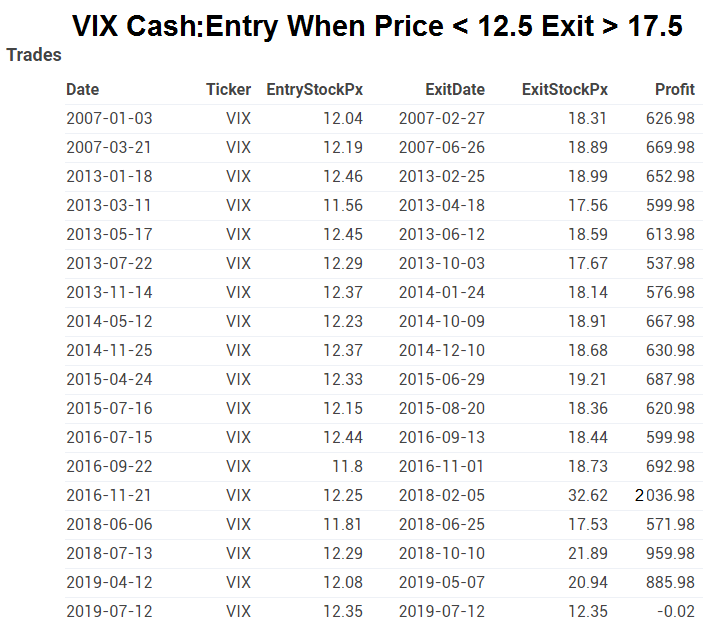

The VIX below 12.5 has only triggered our backtester 18 times.

I have backtested the strategies you mentioned as follows.

1. Buy VIX futures if VIX under 12.5 and sell if gets above 15, 17.5, 20 or 25.

For starters if you were able to buy the VIX cash when it fell under 12.5 and sell when it went above 15, 17.5, 20 or 25 you would do very well. Here are the results for the best of those selling when the cash VIX went above 17.5:

Being unable to buy the VIX cash, what is the best alternative? I can list out some alternatives if people are interested but the returns will not be nearly this good because what VolSkewTrader mentions:

- Trades at a premium to the cash, can only replicate the cash instrument through the OTC variance swap market

- Lose money on the roll yield due to unfavorable VIX term structure

2. Buy VIX calls if VIX under 12.5. 30 days to expiration (DTE) 30 delta calls held to expiration does poorly with a -13.07% Annual Return. Our annual returns are based on profit/stock price, slippage and commissions are considered as explained

here.

3. Buy SPY OTM puts if VIX under 12.5. I chose a long term 1-year put with a low delta of .05 returned a -0.04% annualized return.

4. Buy SPY cheap calls and delta hedge. I backtested buying 6-month OTM 0.05 delta calls, delta hedging every 5 days when the VIX was under 12.5 and exit the position when the VIX went above 17.5. This returned -0.03% annually.

5. Buy a SPY 1x2 put backspread. I used a short 0.40 delta put and two long 0.20 delta puts at 45 days to expiration in the backtest, and entered the spread when the VIX was under 12.5 and held the position to expiration. The strategy returned -0.6%.

6. Buy a SPY straddle 30 DTE hold to expiration when the VIX goes below 12.5 returned 0.27%.

7. See #6

8. Buy UVXY when the VIX goes below 12.5 and exit when the VIX goes above 17.5 returned -4.01%.

So my choice would be to find the best VIX future to buy in this scenario.

If you want to see these backtests and run some of your own, signup for a

free-trial and message me. I can send you links to the backtests which you can edit or run new ones.