Is there a [relatively simple] way to negate effects of implied vol changes? If I have an iron fly that expires Friday, and it settles exactly at the strike of the body, I know what my profit will be:

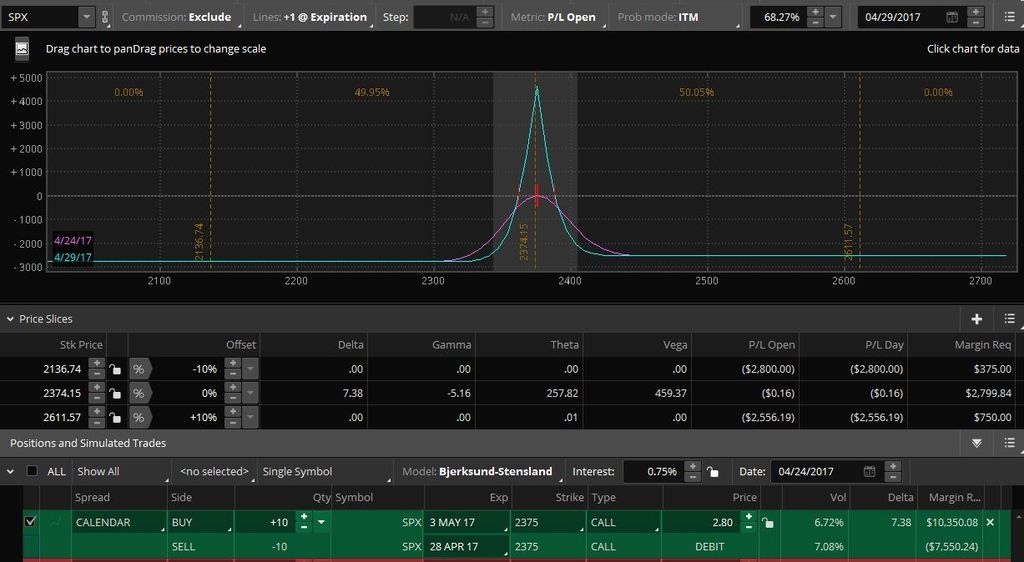

But if I have a calendar (2 wk/1 wk):

... and on Friday it closes exactly at the strike price (2375), I don't know what my profit will be because the implied vol will have changed for the longer dated option (usually lower from contango). I want the risk graph to remain close to what it is showing at the time when the short option expires - I want the implied vol to stay constant for the longer dated option. I know I'm oversimplifying, such as ignoring skew and the relationship to other greeks, but I'll ask anyway. Is there a certain amount of VXX or VX I can be short to remain approximately "implied vol neutral" for my long options? Thanks.

But if I have a calendar (2 wk/1 wk):

... and on Friday it closes exactly at the strike price (2375), I don't know what my profit will be because the implied vol will have changed for the longer dated option (usually lower from contango). I want the risk graph to remain close to what it is showing at the time when the short option expires - I want the implied vol to stay constant for the longer dated option. I know I'm oversimplifying, such as ignoring skew and the relationship to other greeks, but I'll ask anyway. Is there a certain amount of VXX or VX I can be short to remain approximately "implied vol neutral" for my long options? Thanks.