I set it up live on November 2019, these are the results so far.

It trades 3 contracts of MNQ.

It trades 3 contracts of MNQ.

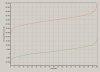

This is a backtest (green) for the last three years up to January 2020, vs the index (blue).

The last months have been in a strong uptrend, so I could've been just lucky. On the other hand the bot made more than 140 trades, each spanning from a few minutes to a few hours. The probability of having chosen bad trades was not negligible.

In other words by doing short-lived, intraday trades at random, the chances of producing a profit are very low. The same is better shown by the percentile rank of the above curves:

The median of the random entry (green) shows a profit of 2.500, but there is a significant chance of loss. The red line is the actual (backtested) system.

I'm aware that the real test is still to come, three months are just too little. If nothing else, the software infrastructure is running smoothly. The systems runs completely unattended on a dedicated computer (I light candles on it and treat it with deference). It writes a web page for remote monitoring from my cellphone and sends me Telegram messages any time it opens/closes a trade.

I will post more on how it's doing.

This is a backtest (green) for the last three years up to January 2020, vs the index (blue).

To verify that, I ran two Montecarlo simulations, the first on the above backtest, the second on a test system that opened the same number of trades, with the same distribution of duration, but at random times. The upper cloud refers to the backtested system, the lower is the random entry:In other words by doing short-lived, intraday trades at random, the chances of producing a profit are very low. The same is better shown by the percentile rank of the above curves:

I'm aware that the real test is still to come, three months are just too little. If nothing else, the software infrastructure is running smoothly. The systems runs completely unattended on a dedicated computer (I light candles on it and treat it with deference). It writes a web page for remote monitoring from my cellphone and sends me Telegram messages any time it opens/closes a trade.

I will post more on how it's doing.