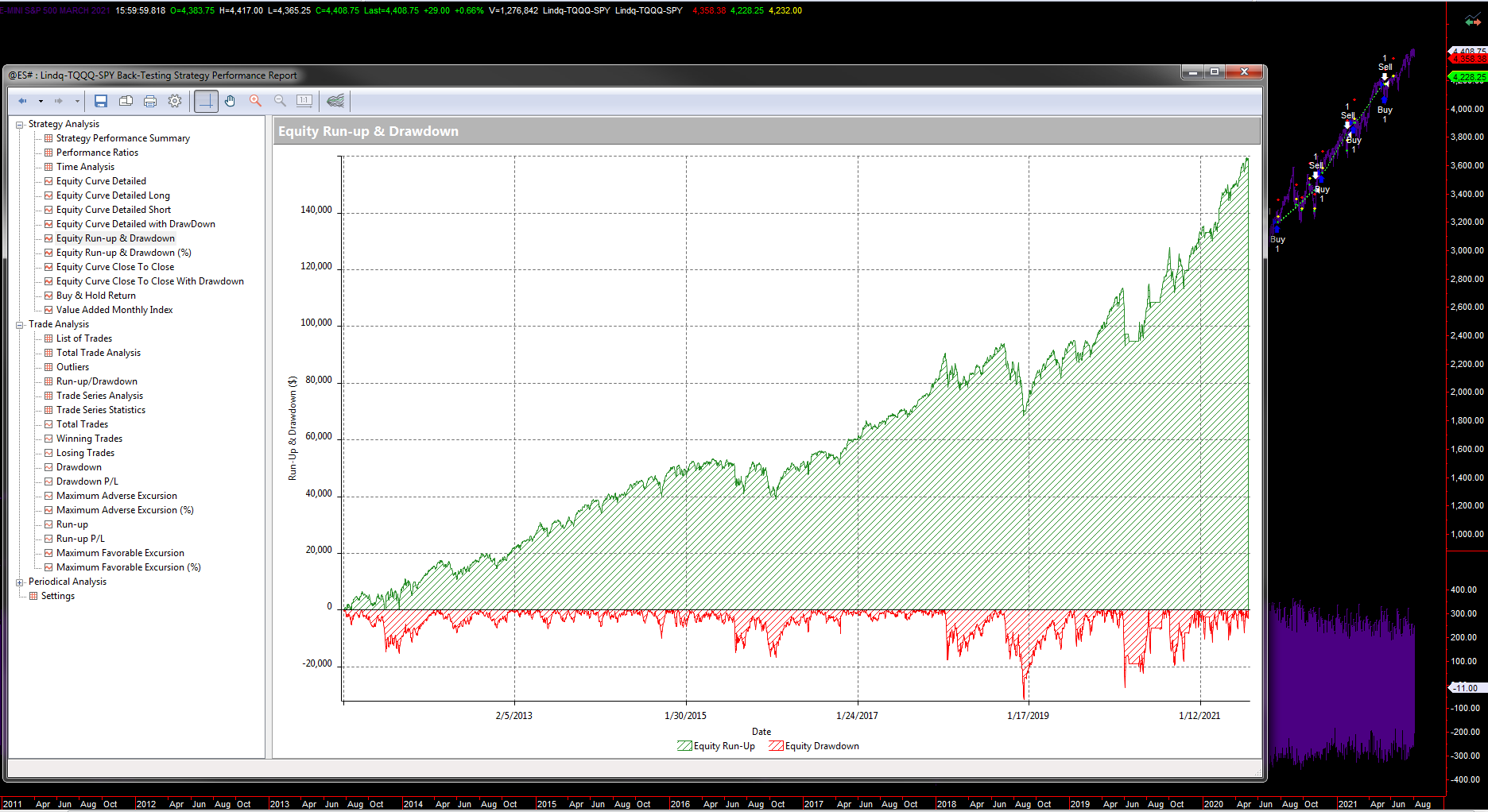

Mine is very close to yours. Formatting is boogered, but the data is there:

Net Profit % 108.79% 108.79% 0.00% 298.13%

Annualized Gain % 27.90% 27.90% 0.00% 58.69%

Exposure 0.00% 0.00% 0.00% 100.00%

Number of Trades 106 106 0 1

Avg Profit/Loss $328.42 $328.42 $0.00 $95,401.54

Avg Profit/Loss % 1.11% 1.11% 0.00% 295.76%

Avg Bars Held 1.00 1.00 0.00 752.00

Winning Trades 74 74 0 1

Winning % 69.81% 69.81% N/A 100.00%

Gross Profit $66,661.09 $66,661.09 $0.00 $95,401.54

Avg Profit $900.83 $900.83 $0.00 $95,401.54

Avg Profit % 3.03% 3.03% 0.00% 295.76%

Avg Bars Held 1.00 1.00 0.00 752.00

Max Consecutive 12 12 0 N/A

Losing Trades 32 32 0 0

Losing % 30.19% 30.19% N/A 0.00%

Gross Loss $-31,848.33 $-31,848.33 $0.00 $0.00

Avg Loss $-995.26 $-995.26 $0.00 $0.00

Avg Loss % -3.34% -3.34% 0.00% 0.00%

Avg Bars Held 1.00 1.00 0.00 0.00

Max Consecutive 4 4 0 N/A

Max Drawdown $-6,038.98 $-6,038.98 $0.00 $-39,711.36

Max Drawdown % -16.19% -16.19% 0.00% -70.25%

Max Drawdown Date 6/3/2019 6/3/2019 N/A 3/20/2020

Wealth-Lab Score 0.00 0.00 0.00 17.46

Profit Factor 2.09 2.09 0.00 INF

Recovery Factor 5.76 5.76 N/A 2.40

Payoff Ratio 0.91 0.91 0.00 INF

Sharpe Ratio 1.68 1.68 0.00 1.01

Ulcer Index 5.81 5.81 0.00 22.98

Wealth-Lab Error Term 7.14 7.14 0.00 16.56

Wealth-Lab Reward Ratio 3.90 3.90 N/A 3.54

Luck Coefficient 1.32 1.32 0.00 1.00

Pessimistic Rate of Return 1.58 1.58 0.00 0.00

Equity Drop Ratio 0.15 0.15 0.00 0.15

Thanks. It's always interesting to compare results in different platforms.

If you were an early user of Wealthlab, you may remember how excellent it was to share code and credit for system improvements. Systems were even named for the initial developer, and subsequent contributors.

")