Hi,

I'm interested in modelling the volatility skew of a stock with a bimodal outcome. I found this blogpost and want to reproduce its findings. I am struggling with the implied volatility-part.

I know that the probability density function is equal to

$f(S) = \sum^n_{i=1}p_i\frac{1}{\sqrt{2\pi}\sigma_i}exp\{-\frac{(S-\mu_i)^2}{2\sigma_i^2}\}$

I also know that the price of a call can be defined as

$C=e^{-rT}\int_0^\infty(S-K)^+p(S)dS$

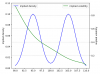

My plotted implied volatility looks different than the authors. What am I doing wrong? My methodology

- obtain the PDF

- get the price of the call using this PDF

- get IV based on price of the call

I attached my Python code for clarity:

import numpy as np

import scipy.stats as ss

import matplotlib.pyplot as plt

from black_scholes import *

from typing import Union

def f(mu: float, sigma: float, x: np.ndarray) -> np.ndarray:

return np.exp((-1 * (x - mu) ** 2) / (2 * sigma ** 2)) / (np.sqrt(2 * np.pi) * sigma)

def call(r: float, T: float, S: np.ndarray, K: Union[int, float], pdf: np.ndarray) -> float:

inner = np.zeros_like(S)

itm = S > K

inner[itm] = S[itm] - K

return np.exp(-r * T) * np.sum(inner * pdf)

def price(S, K, T, r, sigma):

# https://www.aaronschlegel.me/black-scholes-formula-python.html

d1 = (np.log(S / K) + (r + 0.5 * sigma ** 2) * T) / (sigma * np.sqrt(T))

d2 = (np.log(S / K) + (r - 0.5 * sigma ** 2) * T) / (sigma * np.sqrt(T))

return S * ss.norm.cdf(d1, 0.0, 1.0) - K * np.exp(-r * T) * ss.norm.cdf(d2, 0.0, 1.0)

def vega(S, K, T, r, sigma):

d1 = (np.log(S / K) + (r + 0.5 * sigma ** 2) * T) / (sigma * np.sqrt(T))

return S * ss.norm.pdf(d1) * np.sqrt(T)

def iv(c, S, K, T, r):

MAX_ITERATIONS = 200

PRECISION = 1.0e-5

sigma = 0.25

for _ in range(MAX_ITERATIONS):

p = price(S, K, T, r, sigma)

v = vega(S, K, T, r, sigma)

diff = c - p

if abs(diff) < PRECISION:

return sigma

sigma = sigma + diff / v

return sigma

S = 100

n = 2

p_up = 0.5

p_down = 1 - p_up

mu_up = 105

sigma_up = 2

mu_down = 95

sigma_down = 2

T = np.sqrt(7 / 255)

r = 0

if __name__ == "__main__":

dx = 0.5

xs = np.arange(90, 110 + dx, dx)

f_up = p_up * f(mu=mu_up, sigma=sigma_up, x=xs)

f_down = p_down * f(mu=mu_down, sigma=sigma_down, x=xs)

implied_density = f_up + f_down

ax1 = plt.subplot()

ax1.plot(xs, implied_density, c='blue', label='implied density')

ax1.set_ylabel('implied density')

ax1.legend(loc='upper left')

ax1.set_ylim([0, 0.12])

ax2 = ax1.twinx()

ivs = []

for x in xs:

c = call(r=r, T=T, S=xs, K=x, pdf=implied_density)

implied_vol = iv(c=c, S=S, K=x, T=T, r=r)

ivs.append(implied_vol)

ax2.plot(xs, ivs, c='green', label='implied volatility')

ax2.set_ylabel('implied volatility')

ax2.set_xlabel('S')

plt.grid(axis='both', linestyle='--')

ax2.legend(loc='upper right')

plt.tight_layout()

plt.show()

I'm interested in modelling the volatility skew of a stock with a bimodal outcome. I found this blogpost and want to reproduce its findings. I am struggling with the implied volatility-part.

I know that the probability density function is equal to

$f(S) = \sum^n_{i=1}p_i\frac{1}{\sqrt{2\pi}\sigma_i}exp\{-\frac{(S-\mu_i)^2}{2\sigma_i^2}\}$

I also know that the price of a call can be defined as

$C=e^{-rT}\int_0^\infty(S-K)^+p(S)dS$

My plotted implied volatility looks different than the authors. What am I doing wrong? My methodology

- obtain the PDF

- get the price of the call using this PDF

- get IV based on price of the call

I attached my Python code for clarity:

import numpy as np

import scipy.stats as ss

import matplotlib.pyplot as plt

from black_scholes import *

from typing import Union

def f(mu: float, sigma: float, x: np.ndarray) -> np.ndarray:

return np.exp((-1 * (x - mu) ** 2) / (2 * sigma ** 2)) / (np.sqrt(2 * np.pi) * sigma)

def call(r: float, T: float, S: np.ndarray, K: Union[int, float], pdf: np.ndarray) -> float:

inner = np.zeros_like(S)

itm = S > K

inner[itm] = S[itm] - K

return np.exp(-r * T) * np.sum(inner * pdf)

def price(S, K, T, r, sigma):

# https://www.aaronschlegel.me/black-scholes-formula-python.html

d1 = (np.log(S / K) + (r + 0.5 * sigma ** 2) * T) / (sigma * np.sqrt(T))

d2 = (np.log(S / K) + (r - 0.5 * sigma ** 2) * T) / (sigma * np.sqrt(T))

return S * ss.norm.cdf(d1, 0.0, 1.0) - K * np.exp(-r * T) * ss.norm.cdf(d2, 0.0, 1.0)

def vega(S, K, T, r, sigma):

d1 = (np.log(S / K) + (r + 0.5 * sigma ** 2) * T) / (sigma * np.sqrt(T))

return S * ss.norm.pdf(d1) * np.sqrt(T)

def iv(c, S, K, T, r):

MAX_ITERATIONS = 200

PRECISION = 1.0e-5

sigma = 0.25

for _ in range(MAX_ITERATIONS):

p = price(S, K, T, r, sigma)

v = vega(S, K, T, r, sigma)

diff = c - p

if abs(diff) < PRECISION:

return sigma

sigma = sigma + diff / v

return sigma

S = 100

n = 2

p_up = 0.5

p_down = 1 - p_up

mu_up = 105

sigma_up = 2

mu_down = 95

sigma_down = 2

T = np.sqrt(7 / 255)

r = 0

if __name__ == "__main__":

dx = 0.5

xs = np.arange(90, 110 + dx, dx)

f_up = p_up * f(mu=mu_up, sigma=sigma_up, x=xs)

f_down = p_down * f(mu=mu_down, sigma=sigma_down, x=xs)

implied_density = f_up + f_down

ax1 = plt.subplot()

ax1.plot(xs, implied_density, c='blue', label='implied density')

ax1.set_ylabel('implied density')

ax1.legend(loc='upper left')

ax1.set_ylim([0, 0.12])

ax2 = ax1.twinx()

ivs = []

for x in xs:

c = call(r=r, T=T, S=xs, K=x, pdf=implied_density)

implied_vol = iv(c=c, S=S, K=x, T=T, r=r)

ivs.append(implied_vol)

ax2.plot(xs, ivs, c='green', label='implied volatility')

ax2.set_ylabel('implied volatility')

ax2.set_xlabel('S')

plt.grid(axis='both', linestyle='--')

ax2.legend(loc='upper right')

plt.tight_layout()

plt.show()

")