Good morning.

This is a scalping trading algorithm based on footprint signals for entries and exits.

I've been testing it in demo for a month.

I also did backtests and the profit factor are 2 times more than the results with the live test

I tested it with an apex trader funding account but it failed because of the DD trailing (even though it was positive).

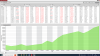

This is a scalping trading algorithm based on footprint signals for entries and exits.

I've been testing it in demo for a month.

I also did backtests and the profit factor are 2 times more than the results with the live test

I tested it with an apex trader funding account but it failed because of the DD trailing (even though it was positive).