Skew means that vols are higher for lower strikes compared to ATM and usually calls... at least, this is the case for equities and equity indices. This has to do with downward risk perception.

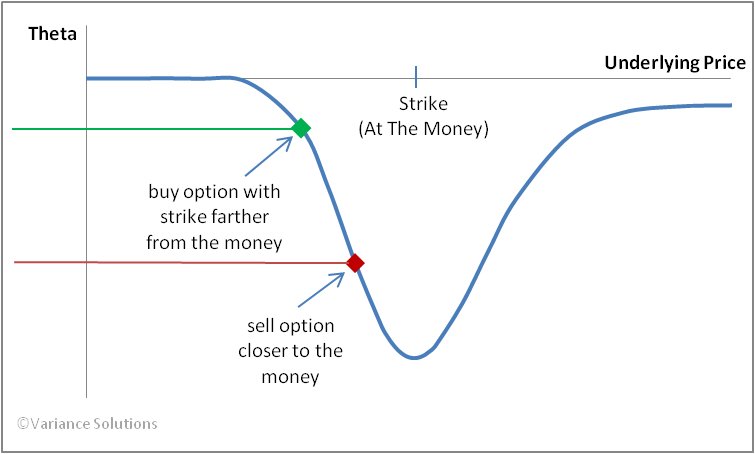

A higher vol means higher value of an option... therefore increasing theta (value loss due to 1 day time). The pic I put on actually shows the top of the curve is slightly left of the ATM... hardly visible, but it should be there.

The way theta is shown in IB and in general... is wrong IMO. I regard theta as loss in value in 24 hrs... the theta in a call and put of the same strike are exactly the same. However, you notice that in your system, IB or any really, that the theta for calls are higher than for puts. This is due to the fact that options are priced on fwd/future pricing, taking into account an interest factor. So... part of the theta is due to the decrease in interest component... for calls this is a negative number (so increasing theta) and for puts this is a positive number (decreasing theta). IMO this isn't really theta, but just interest component (not to be confused with Rho, that's something else again).

So, usually in options you will see a non-normal distribution, partly due to skew... this causes relative vols and prices in OTM puts to be higher than OTM calls... and this causes that shift in theta to be higher in OTM puts.

")